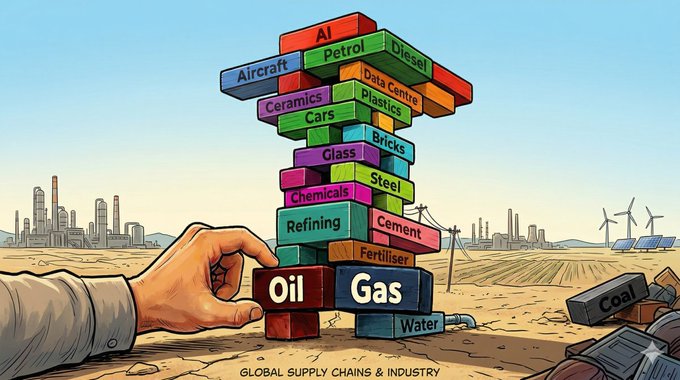

The United Kingdom once stood as an industrial powerhouse, fueled by abundant domestic oil, gas, and coal reserves that powered manufacturing, jobs, and economic growth. Today, that foundation is crumbling under the weight of Net Zero policies, sky-high energy taxes, regulatory barriers, and a deliberate shift away from reliable hydrocarbons. A powerful new report from the Great British Business Council (GBBC), released in early 2026, lays bare this self-inflicted wound. Titled Premeditated Industrial Destruction? How the UK Destroyed Its Industry and a Plan to Reverse This, the paper—co-authored by economist Catherine McBride OBE, energy analyst David Turver, and PR consultant Brian Monteith—delivers a data-driven indictment of decades of misguided policy.

As the UK plunges deeper into an energy crisis—with industrial electricity prices the highest in the G7 and factories facing shutdowns—the report demands renewed attention. It is not just a postmortem on deindustrialization; it offers a clear, actionable roadmap to reversal. At Energy News Beat, we will be reaching out to co-author David Turver for an in-depth discussion on our podcast to unpack these findings and explore real solutions.

Evaluating the GBBC Report: A Forensic Takedown of Policy Failure

Released on April 1, 2026 (with the PDF dated March 31), the report systematically dismantles the narrative that Net Zero is a benign or inevitable transition. Instead, it argues that UK governments—through the Climate Change Act 2008 (amended to 100% reduction by 2050), the Paris Agreement, high taxes like the 38% Energy Profits Levy (EPL) and 35% Oil and Gas Price Mechanism (OGPM), the Carbon Price Support (CPS), Climate Change Levy (CCL), and Emissions Trading Scheme (ETS)—have engineered industrial decline.

Key evidence of destruction includes: Energy-intensive industries gutted: Manufacturing’s share of GDP has halved since 1990. Steel output has plummeted (from millions of tonnes historically to just 4 million tonnes in 2024), with blast furnaces at Port Talbot closing.

Aluminum production collapsed from over 300,000 tonnes in the early 2000s to under 50,000 tonnes. Petrochemical sites have shuttered (25 chemical sites closed 2019–2025), refineries dropped from 18 in the 1970s to just 4 today, and fertilizer output halved since 2000, forcing 60% imports.

Oil, gas, and coal choked: North Sea production fell 40% (oil) and 21% (gas) since 2019 due to 78% effective tax rates, fracking moratoriums (reimposed despite brief lifts), and licensing bans under the North Sea Future Plan. Coal reserves (77 million tonnes recoverable) sit untapped as the last power station closed in 2024; mines like Ffos-y-fran were forced shut by activists. Result: 43.8% energy import dependency in 2024, despite vast domestic reserves.

Skyrocketing costs and lost productivity: UK industrial electricity prices remain the highest in Europe (25.33p/kWh for large users in H1 2025, 125% above EU median). Carbon taxes add 5–7% to bills. Renewables subsidies (CfDs £2.6bn in 2025, Renewables Obligation £8.4bn projected 2026/27) and intermittency costs (BSUoS, TNUoS) shift burdens to industry. Offshoring emissions has cut UK territorial CO₂ to just 0.8% of global totals—but global emissions rose, and imported goods embed 180 million tonnes of CO₂.

Jobs and GDP hemorrhage: Over 150,000–200,000 industrial jobs lost since 2019. Oil/gas supports £25bn GVA and 200,000+ jobs today—but potential £150bn more from untapped resources is blocked. Trade deficits in fuels and chemicals ballooned.

The authors label this “premeditated” because policies explicitly targeted hydrocarbons via Scope 3 emissions rules, financial regulations (PRA, BoE, Basel rules hiking borrowing costs), and activist-enabled legal blocks (e.g., Rosebank field delayed 22 years). Renewables were prioritized despite their intermittency, while Norway—exploiting similar geology—thrives with new discoveries, lower effective taxes, and full investment deductions. The report calls Net Zero “futile”: UK cuts are dwarfed by global rises and offshoring.

Strengths? It is evidence-heavy, with ONS, OBR, and government data charts on production, revenues, and GVA. It avoids ideology, focusing on economic reality: hydrocarbons still supply 78% of UK energy. Weaknesses? Some may debate the exact scope of Scope 3 accounting or timelines, but the data on decline is irrefutable.

Why Renewed Interest Now? The UK’s Deepening Energy Crisis

Fast-forward to April 2026: the crisis is accelerating. Industrial electricity prices are 70%+ above pre-2022 levels and the highest among G7 nations, with further 10–30% rises projected. Gas price shocks from global tensions (Iran conflict) compound the pain. Factories face production cuts “within weeks,” 40% of manufacturers slashed investment, and deindustrialization is “rapid.” Refineries and chemical plants close; energy-intensive sectors warn of offshoring.

The GBBC report’s timing could not be better. It exposes how Net Zero created this vulnerability—import dependency amid geopolitical risks—and provides the antidote. Ignoring it risks irreversible damage to jobs, security, and competitiveness.

Energy News Beat will reach out to David Turver—one of the report’s authors and a leading voice on energy policy via his Eigen Values Substack—for our podcast. His forensic analysis of subsidies, prices, and policy failures makes him essential listening as Britain confronts reality.

Parallels with California: A Cautionary Tale Across the Pond

The UK’s path mirrors California’s energy disaster almost exactly. Both embraced aggressive renewables mandates, EV/heat pump pushes, and anti-fossil fuel rules—resulting in the highest electricity rates, refinery closures, and industrial flight.

Prices and costs: California’s residential electricity is ~32¢/kWh (double the U.S. average), with bills hitting $1,000/month for AC in summer. Industrial users suffer similarly. Refineries dropped from 40+ in the 1980s to 13, with more closures announced—pushing gasoline toward $8/gallon.

Deindustrialization: Manufacturing flees high costs; emissions are offshored. Net Zero rhetoric ignores that 80%+ of California’s total energy remains hydrocarbons. Blackout risks, battery failures, and mandates drive businesses out.

Policy echoes: Both prioritize intermittent power over dispatchable power, impose carbon taxes/levies, and face activist/legal blocks. UK’s CfDs and ETS parallel California’s renewable portfolio standards. Result? Energy security sacrificed for ideology.

The GBBC plan’s focus on domestic hydrocarbons, tax relief, and mandate repeal offers lessons California ignored—potentially averting the same fate.

A Plan to Reverse Course: Practical and Urgent

The report’s 21-point reversal is straightforward and supply-focused:

Scrap EPL, OGPM, CPS, and CCL to slash costs immediately.

Lift fracking bans, issue North Sea/onshore licenses (copy Norway’s model: full expensing, stable taxes).

Restart coal mining for industry and exports; use domestic gas for power, chemicals, and new sectors like AI/data centers.

Ditch EV/heat pump mandates; reform EIAs to prioritize real impacts over Scope 3 imports.

Exit or downgrade Paris Agreement commitments; cut renewables subsidies and activist veto power.

Implementation could unlock £150bn+ GVA, restore jobs, narrow trade deficits, and secure energy—without fantasy tech.

Britain does not have to accept decline. The GBBC report proves the destruction was policy-driven and reversible. With an energy crisis biting harder than ever, policymakers must choose: double down on failure or embrace the plan to rebuild. Energy News Beat will keep the pressure on—and we look forward to David Turver joining us to chart the path forward.

Appendix: Links and Sources

- GBBC Report PDF (full download): https://gbbc.uk/wp-content/uploads/2026/04/Premeditated-Industrial-Destruction-Final-31-March-2026-with-a-plan.pdf

- GBBC Report Webpage: https://gbbc.uk/uk-deindustrialisation-energy-policy/

- David Turver on X/Substack (Eigen Values):

https://x.com/7Kiwi

- Related Turver IEA Report (Jan 2026, The Cost of Net Zero): https://iea.org.uk/publications/the-cost-of-net-zero/

- UK Industrial Energy Crisis Coverage: Guardian (Mar 2026), Dieter Helm analysis, CBI/Energy UK report.

- The Energy News Beat Substack: https://theenergynewsbeat.substack.com/

- Grok on X

- California Parallels: Energy News Beat analysis, Heartland Institute, Telegraph comparisons.

This article reflects independent analysis of public data and reports as of April 2026.

Check out the Energy News Beat Substack: https://theenergynewsbeat.substack.com/