The Federal Reserve Bank of Dallas released its Q1 2026 Energy Survey on March 25, 2026, and the headline is clear: after nearly a year of contraction, oil and gas activity in the Eleventh Federal Reserve District (Texas, northern Louisiana, and southern New Mexico) is expanding again. The survey’s broadest measure—the business activity index—jumped from -6.2 in Q4 2025 to +21.0 in Q1 2026, marking the first positive reading since early 2025 and the strongest expansion signal since 2022.

This rebound comes amid a backdrop of elevated geopolitical uncertainty, sharply higher oil prices (WTI averaged ~$94.65 during the March 11–19 survey window), and rising costs. While production remains largely flat for now, executives report improved outlooks, stronger capital spending plans, and—crucially for the service sector—higher equipment utilization and operating margins.

Key Survey Highlights: What the Numbers Show

The survey polled 135 firms (92 E&P, 43 oilfield services). Diffusion indexes are calculated as the percentage reporting an increase minus the percentage reporting a decrease.

All Firms (Q/Q change):

- Business Activity: +21.0 (from -6.2)

- Company Outlook: +32.2 (from -15.2)

- Outlook Uncertainty: +53.7 (from +43.4) — now at its highest level in recent quarters

- Capital Expenditures: +21.2 (from -11.6)

- Employment: +0.8 (from -10.8)

- Wages & Benefits: +23.5 (from +6.2)

E&P Firms:

- Oil production index held steady at 0.0 (unchanged output)

- Natural gas production edged higher to +2.3

- Finding & development costs: +22.3

- Lease operating expenses: +30.0

Oilfield Services Firms:

- Business activity: +30.3 (strongest reading in the survey)

- Equipment utilization: +30.2

- Input costs: +34.9

Year-over-year comparisons also turned solidly positive, with business activity indexes showing the sharpest improvement since the post-pandemic recovery period.

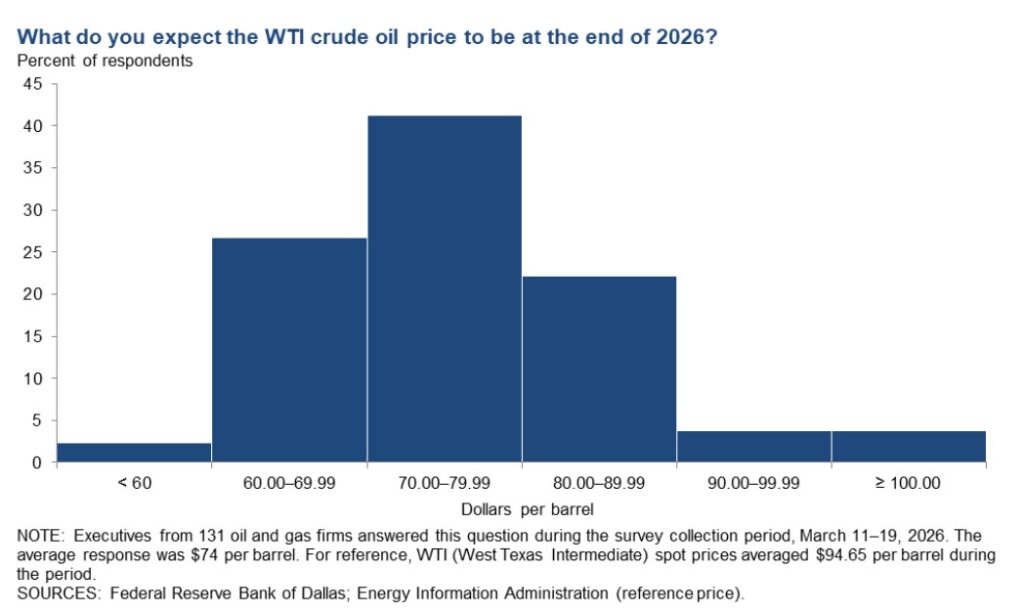

Price Forecasts and Breakevens: Caution Despite the Rally

Executives now expect West Texas Intermediate (WTI) crude to average $74 per barrel by year-end 2026 (up sharply from last quarter’s $62 forecast), with a wide range of $50–$135 reflecting geopolitical volatility. Longer-term (five years out) they see $79/bbl. Henry Hub natural gas is forecast at $3.60/MMBtu by year-end 2026.

Break-even prices rose modestly:

- Operating expenses for existing wells: $43/bbl average (up from $41)

- New wells to drill profitably: $66/bbl average (Permian Basin: $67/bbl, up from $65 last year)

Large firms (≥10,000 b/d) report lower breakevens (~$59–$59 for new wells) than smaller operators, highlighting scale advantages in a higher-cost environment.

Special Questions: Drilling Plans and Long-Term Views

Half of E&P executives said 2026 drilling plans are unchanged since the start of the year. However, smaller firms are noticeably more aggressive—nearly 60% plan to increase wells drilled—while large producers remain largely on hold, waiting for clearer signals once the current Middle East tensions (widely referenced in executive comments as the Iran conflict and Strait of Hormuz disruptions) resolve.

Comments from respondents captured the mood perfectly: “We are drilling six wells in 2026 vs. zero prior to the increase in oil prices” (small E&P) versus cautious “wait-and-see” from majors who view the price spike as temporary. Many expect consolidation opportunities for independents and slight improvements in oil/gas recovery rates over the next decade.

Higher Oil Prices: A Long-Run Win for Investors and U.S. Consumers

The near-term price surge is geopolitically driven and may moderate, but sustained higher prices (above breakevens) are a powerful catalyst for more domestic drilling. Here’s why that benefits investors and consumers over the long run:

- Investors: Higher realized prices boost free cash flow, enabling dividend hikes, share buybacks, and accelerated debt reduction for E&P and service companies. Small operators are already responding with increased activity, creating a virtuous cycle of revenue growth, higher valuations, and M&A opportunities. The Dallas Fed data show capital expenditures and equipment utilization rebounding—direct tailwinds for oilfield service stocks and midstream infrastructure.

- Consumers: More U.S. drilling expands domestic supply, enhancing energy security and reducing reliance on imports. This buffers against global shocks, supports jobs and tax revenues in producing states (Texas alone generates billions in royalties and severance taxes), and keeps long-term energy costs lower and more stable than in import-dependent regions. The economic multiplier effect—jobs in drilling, manufacturing, and logistics—strengthens household incomes in energy-producing communities.

With the exception of California (where strict permitting, environmental rules, and production bans have driven output steadily lower), the rest of the United States is far better positioned than peers like the UK or Australia. The U.S. remains the world’s top oil producer thanks to shale innovation, private mineral rights, and relatively streamlined development on federal and state lands in Texas, New Mexico, and the Gulf. In contrast:

- The UK faces a mature, declining North Sea basin hampered by high taxes, net-zero mandates limiting new projects, and policy uncertainty.

- Australia is a major LNG exporter but grapples with domestic price volatility, lengthy environmental approvals, and regulatory hurdles that slow upstream investment.

The result? U.S. shale can respond faster to price signals, delivering supply growth that benefits American consumers while competitors lag.

Bottom Line

The Dallas Fed survey confirms what many in the patch have felt: the sector is turning the corner. Activity is rising, outlooks are improving, and higher prices are prompting selective drilling increases—especially among nimble independents. Elevated uncertainty remains the biggest near-term risk, but the long-term fundamentals for U.S. oil and gas remain robust. For investors seeking exposure to domestic energy and for consumers counting on reliable, affordable supply, more drilling in America is the clearest path forward.

Appendix: Sources and Further Reading

- Official Dallas Fed Energy Survey Q1 2026 Report: https://www.dallasfed.org/

research/surveys/des/2026/2601 - Dallas Fed News Release: https://www.dallasfed.org/

news/releases/2026/nr260325des - Historical Dallas Fed Energy Survey Data (back to 2016): https://www.dallasfed.org/

research/surveys/des/data - FRED Economic Data (Business Activity Index): https://fred.stlouisfed.org/

series/DALENGINDEXQQ04 - FRED Uncertainty Index: https://fred.stlouisfed.org/

series/DALENGINDEXQQ07 - Reuters analysis of survey and drilling plans: https://www.reuters.com/

business/energy/dallas-fed- survey-finds-first-quarter- oil-gas-activity-rose-2026-03- 25/ - Novi Labs Q1 2026 Survey Takeaways: https://novilabs.com/blog/

dallas-fed-energy-survey-q1- 2026-key-takeaways-and- analysis/ - EIA International Energy Statistics (U.S. production leadership): https://www.eia.gov/tools/

faqs/faq.php?id=709&t=6

All charts in this article were generated from official Dallas Fed data. Full quarterly datasets and additional charts are available in the Dallas Fed’s downloadable Excel file linked in the report. Stay tuned to Energy News Beat for ongoing coverage as the Q2 2026 survey approaches in June.