By the time they finally wanted to sell their home, it wasn’t easy anymore because demand had plunged, and fewer of those mortgages got paid off.

By Wolf Richter for WOLF STREET.

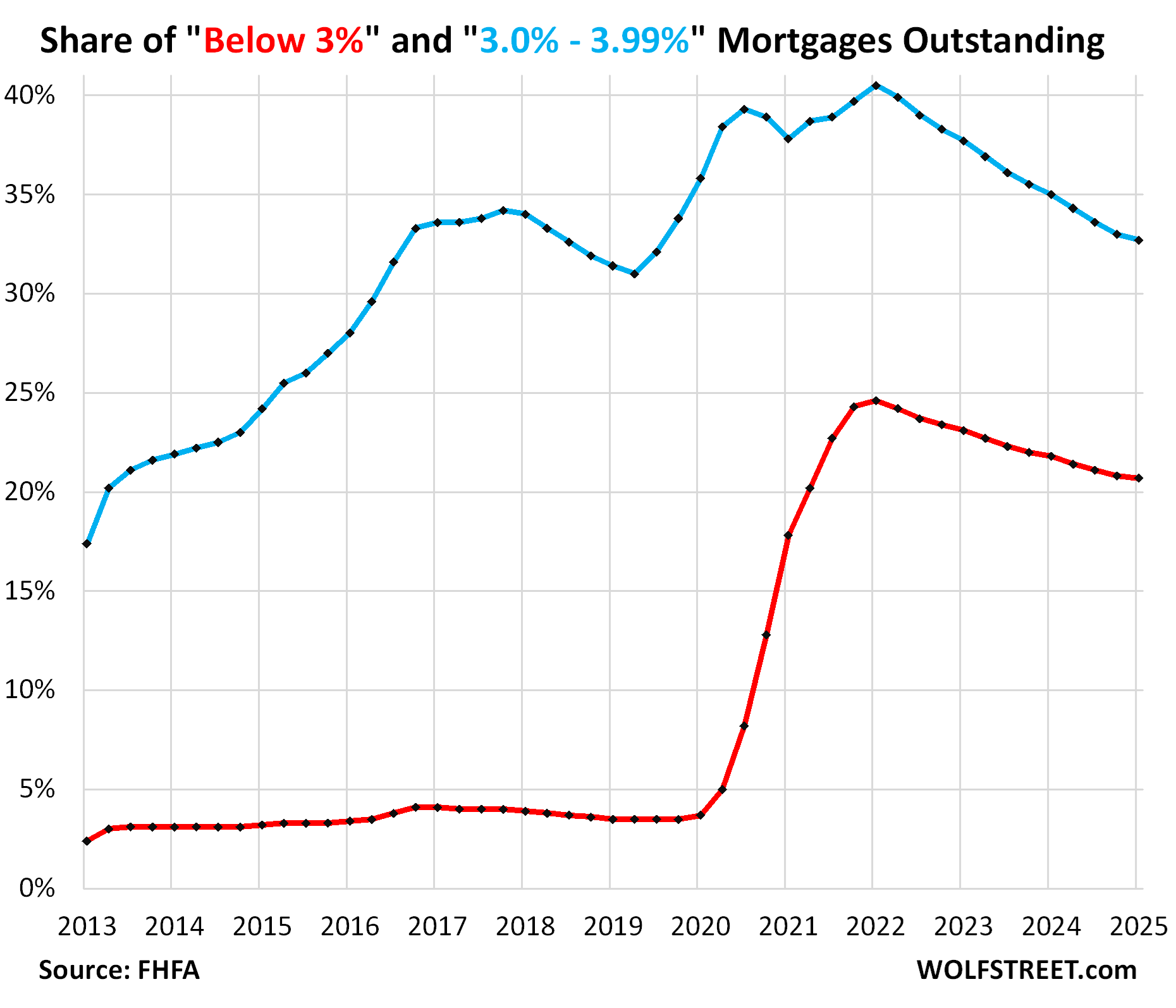

Mortgages outstanding with rates below 3% declined to a share of 20.7% of all mortgages in Q1, according to data today by the Federal Housing Finance Agency (FHFA). Their share started to decline in mid-2022. But the decline of just 10 basis points Q1 was the smallest since the declines started. Over these three years, the quarter-to-quarter declines of the share of these below-3% mortgages averaged just over 30 basis points, with a range between -20 to -50 basis points (red in the chart).

Similarly, the share of 3-4% mortgages declined by 30 basis points to a share of 32.7%. But the average quarter-to-quarter decline since mid-2022 was nearly 70 basis points, with a range from -50 to -90 basis points (blue). In the chart, the slowdown is visible in the flattening of the curves at the end.

The declining share of these ultra-low-rate mortgages represents the exit of homeowners from the “lock-in effect.” This slowdown in the rates of decline – the slowdown of this exit – is not what the real estate brokers and mortgage lenders were hoping for. But it’s not that locked-in homeowners didn’t want to sell – on the contrary, supply has ballooned as they put their homes on the market. It’s that demand has plunged further in Q1, even below the beaten-down levels from a year earlier, and a lot of them couldn’t sell, and so fewer of these mortgages got paid off.

When these low mortgage rates came along in early 2020, they triggered a tsunami of refinancing of higher-rate mortgages, and the number of these outstanding low-rate mortgages exploded through Q1 2022.

The lock-in effect is where homeowners refuse to move because they would have to sell their home and pay off the mortgage, and finance the next home at a much higher mortgage rate. This lock-in effect is in part responsible for the roughly 40% collapse in demand for mortgages compared to 2019, and for the plunge in sales of existing homes – by 23% from 2019 for single-family homes and by 38% for condos.

But even the closest thing to free money that Americans could borrow has slowly been getting paid off because homeowners moved to take a new job or accommodate a larger family, or got divorced, or died.

Or they’d already bought a new home a few years ago and moved into it, but kept the old home to ride up the home-price explosion all the way. And now the carrying costs of that vacant home are becoming a burden, and prices are no longer exploding; but instead in some markets, there are downdrafts in single-family home prices, and in more markets, there are serious downdrafts in condo prices. And so they put these vacant homes on the market, and pay off the mortgage if they sell the home.

The hope of brokers and mortgage lenders was that the lock-in effect would loosen up, and that more of these locked-in homeowners would return to the market as buyers and sellers and generate commissions, fees, and points coming and going.

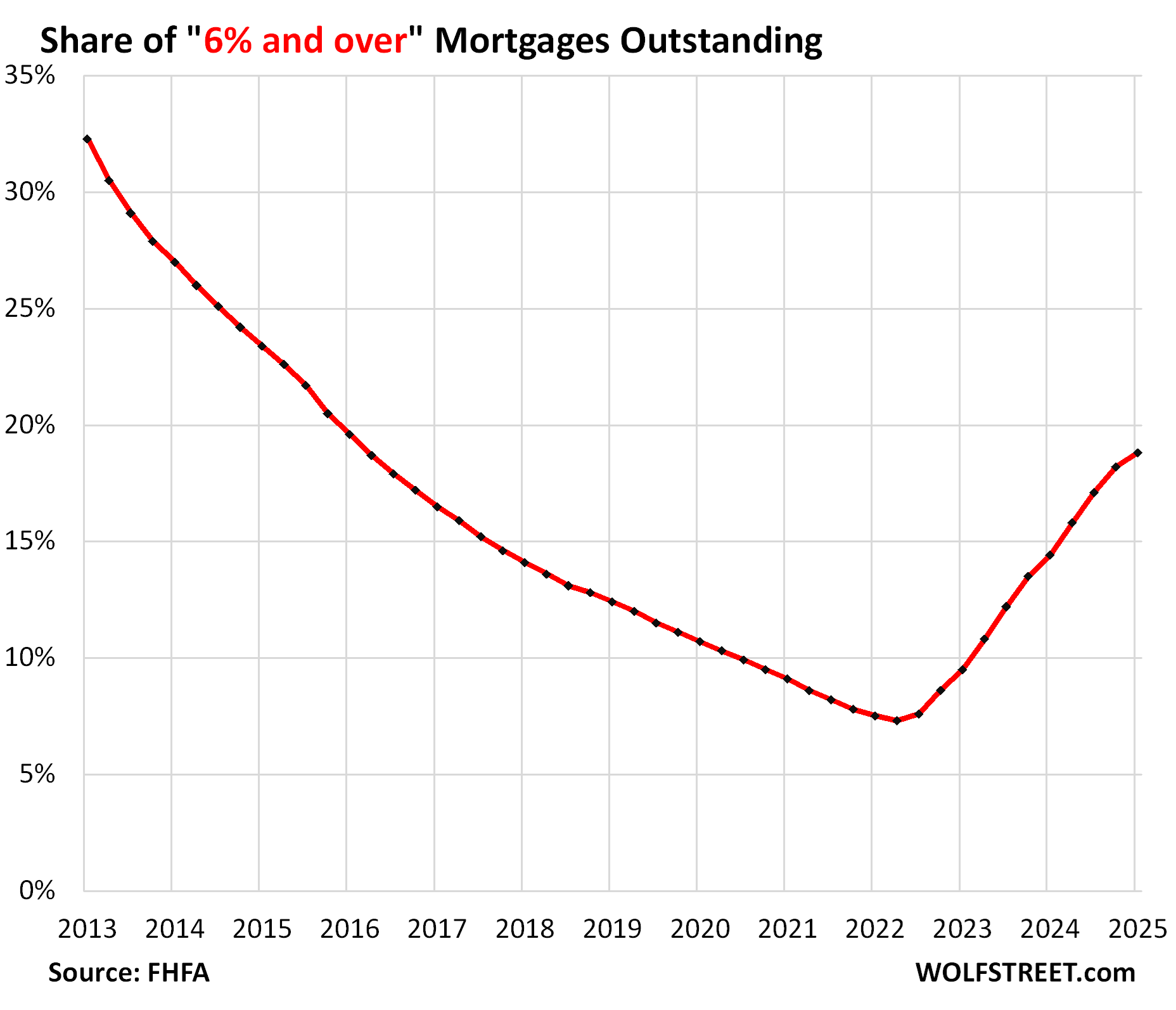

The share of 6%-plus mortgages rose by 60 basis points to a share of 18.8% in Q1, the highest since Q1 2016. Their share has multiplied by over 2.5, from 7.3% at the low point in Q2 2022.

But that 60-basis point increase in the share was the slowest increase since increases took off in mid-2022. Between Q3 2022 and Q4 2024, the increases averaged nearly 120 basis points per quarter, with a range from +90 to +140 basis points.

The ultra-low-rate mortgages were a brief phenomenon.

The below-3% mortgage rates burst on the housing scene from mid-2020 to October 2021, as a result of the Fed’s massive pandemic QE that included purchases of trillions of dollars of mortgage-backed securities.

Even the 3-4% mortgages were a relatively brief phenomenon that came and went several times since late 2011 as a result of the Fed’s Financial Crisis-era QE.

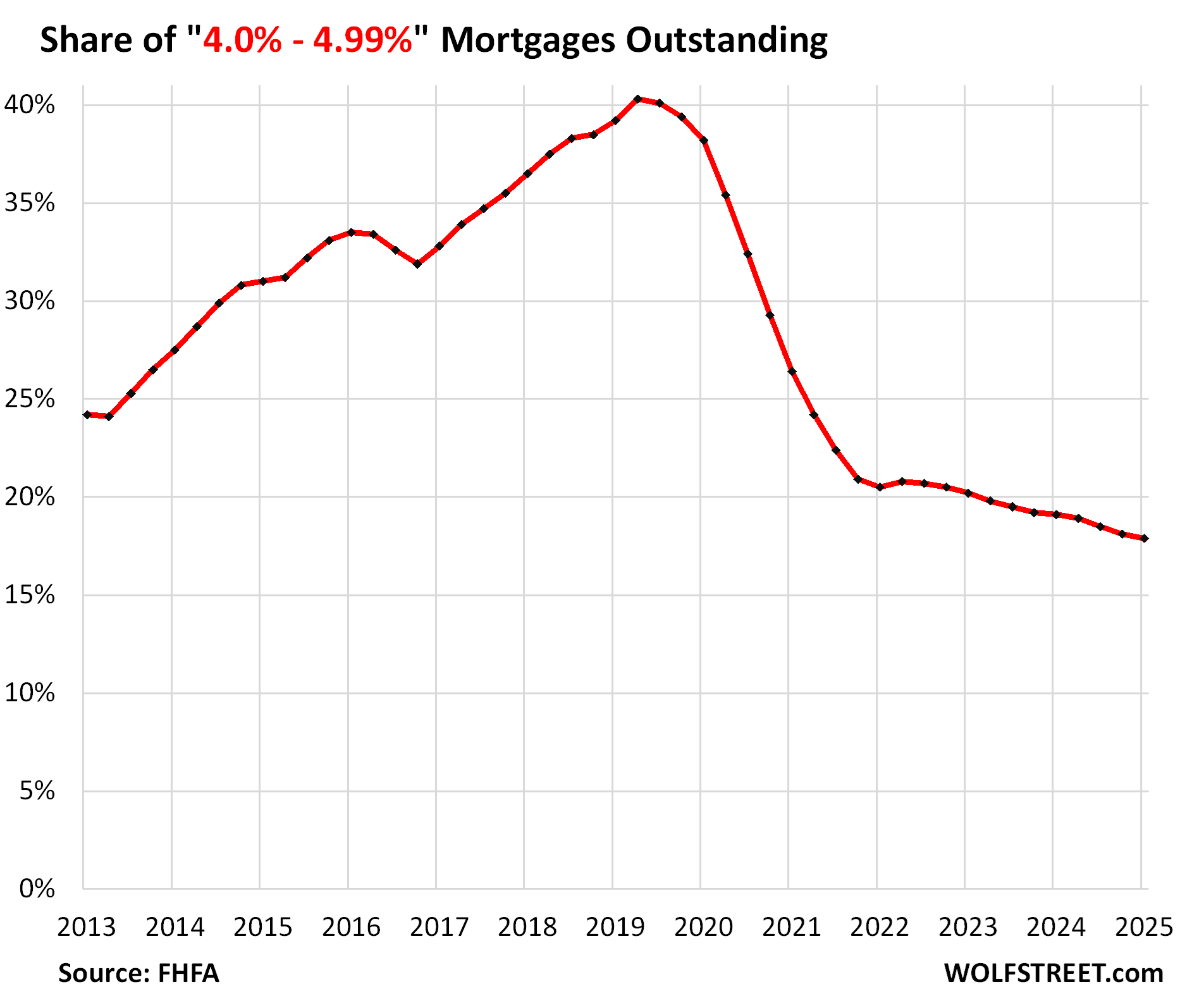

Even the 4-5% mortgages did not exist before the Fed’s Financial Crisis QE at the beginning of 2009.

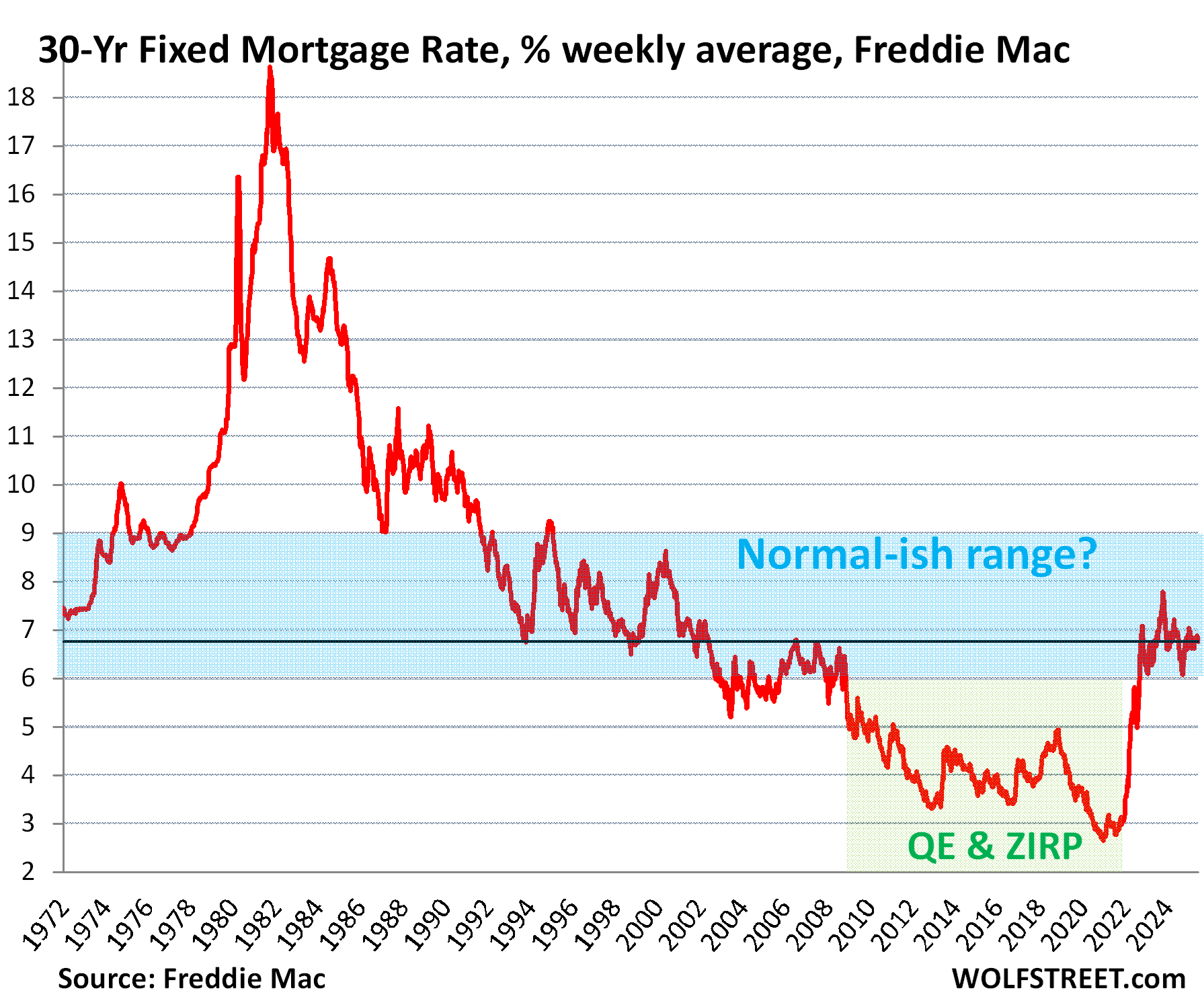

For a few years in the early 2000s, mortgage rates were in the 6% range – so low that they created the Housing Bubble that later imploded, and the resulting mortgage bust helped trigger the Financial Crisis that threatened to take down the entire US financial system.

In the decades before then, mortgage rates were at around 7% and higher, which is roughly where they’ve also been over the past three years.

Unfortunately, the data from the FHFA on the share of mortgages by mortgage rates goes back to only 2013, and therefore only reflects the era when QE had already repressed mortgage rates.

The share of 4-5% mortgages dipped by 20 basis points to 17.9% in Q1. That share is the lowest in the FHFA’s data going back to 2013.

Some of these mortgages were refinanced into lower-rate mortgages when mortgage rates began to drop in 2019. Then in Q2 2020 through Q1 2022, the tsunami of refinancing caused their share to get cut in half, and their share has since then declined further.

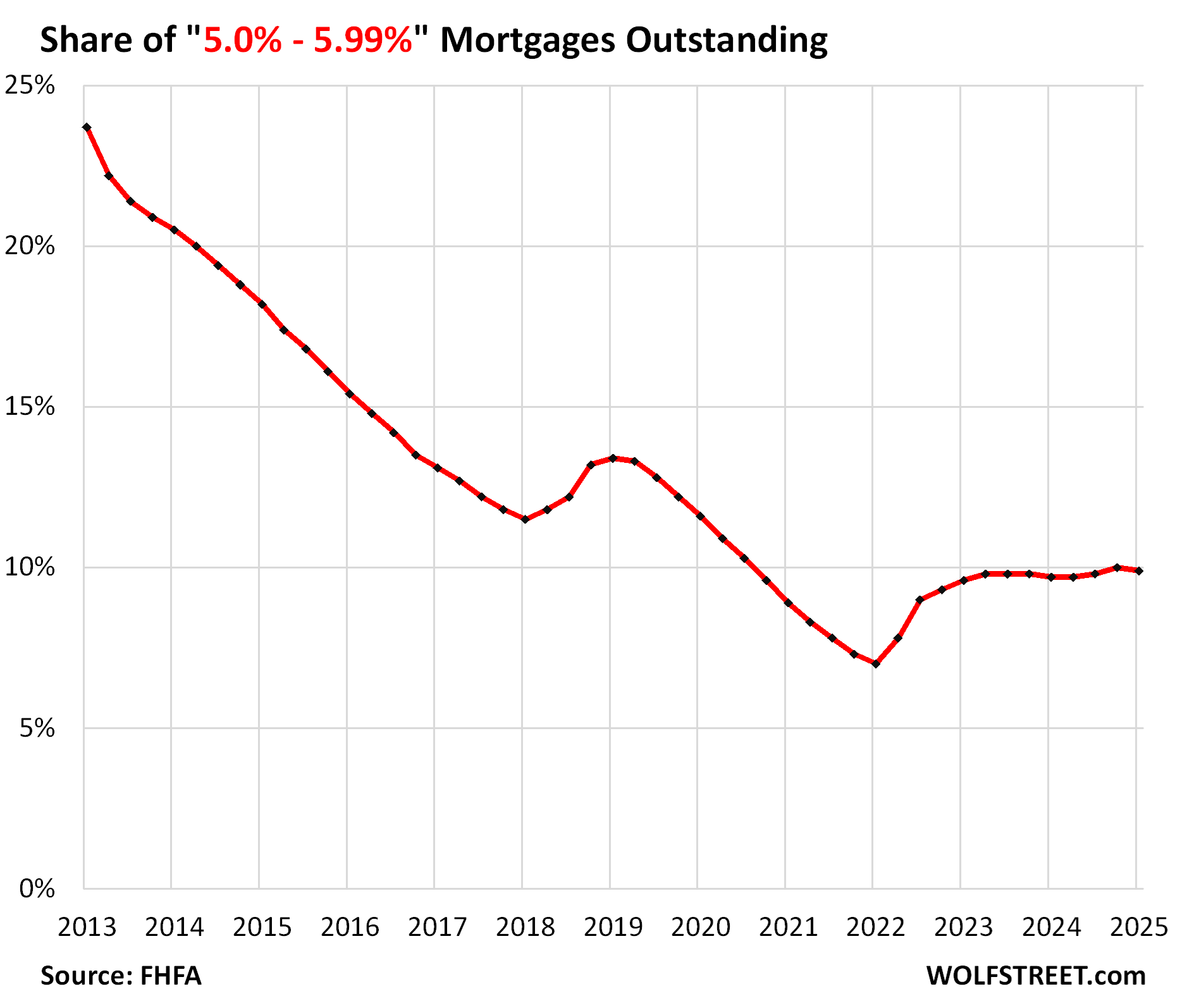

The share of 5-6% mortgages has remained roughly stable over the past two years, mostly just under the 10%-line. In Q1, the share dipped to 9.9% of mortgages outstanding.

There are fixed-rate mortgages offered in this range. For example, the interest rate of the average conforming 15-year mortgage fell below 6% in February and has largely remained below 6%.

The long decline of the share of these 5-6% mortgages during the QE era to bottom out in Q1 2022 at 7.0% was interrupted only by the Fed’s QT and rate hikes in 2018, when mortgage rates rose, and the average 30-year fixed mortgage rate briefly hit 5% in November 2018. But in 2019, mortgage rates declined again amid the Fed’s rate cuts and end of QT.

The lock-in effect has depressed demand for homes, and real estate brokers, mortgage lenders, and mortgage brokers have gotten hit hard by this plunge in demand and shed a large portion of their employment to deal with it (I discussed the effects here: Housing Bubble & Bust #1 and #2 as Seen through Employment at Mortgage Lenders: They Shed Jobs Again, 38% Gone).

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()