In the dynamic world of energy utilities, Entergy Corporation (NYSE: ETR) has been making waves with its steady performance amid broader market fluctuations. As of December 2025, investors are closely watching whether this regulated utility giant is keeping pace with—or even surpassing—high-growth indices like the Nasdaq Composite. Drawing from recent financial data and market trends, the short answer is yes: Entergy has modestly outperformed the Nasdaq both year-to-date and over the past 52 weeks.

But let’s dive deeper into the latest earnings report, key drivers behind the stock’s movement, a direct comparison with the Nasdaq, and what investors should keep an eye on moving forward.A Look at Entergy’s Latest Earnings ReportEntergy’s most recent quarterly results, released for the third quarter of 2025 on October 29, provide a solid foundation for understanding its current trajectory.

The company reported earnings per share (EPS) of $1.53 on both an as-reported and adjusted (non-GAAP) basis, surpassing Wall Street expectations of $1.46 per share by about 4.8%.

This beat came despite ongoing challenges in the utility sector, such as regulatory hurdles and fluctuating energy costs. Revenues for the quarter showed year-over-year improvement, driven primarily by the Utility segment, which contributed $810 million in earnings attributable to Entergy, or $1.79 per share.

Key highlights included stronger industrial sales and favorable weather patterns boosting demand, though these were partially offset by higher operating expenses. Overall, the results reinforced Entergy’s full-year 2025 guidance, which was initiated earlier in the year at $3.75 to $3.95 per share.

Analysts noted that this performance positions Entergy well for continued stability, with the company’s focus on regulated operations providing a buffer against economic volatility.

What’s Driving Entergy’s Stock Price?

Several factors are propelling Entergy’s stock upward in late 2025. First and foremost, the positive earnings surprise has fueled investor optimism, leading to a Zacks Rank upgrade to #2 (Buy) in October.

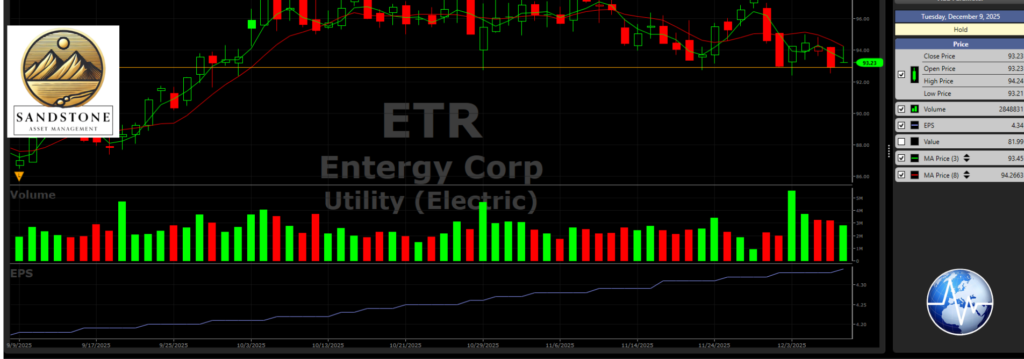

The stock has seen a 1.37% one-day gain recently, pushing shares to around $94.24, building on a robust year-to-date increase.

Broader drivers include strategic investments in infrastructure, such as new natural gas plants in Louisiana, which enhance capacity and reliability in a region prone to extreme weather.

Rising energy demand from data centers and electrification trends is another tailwind, as utilities like Entergy benefit from increased load growth. Additionally, Entergy’s attractive dividend yield—currently around 4.8%—appeals to income-focused investors in a high-interest-rate environment.On the flip side, sector-wide pressures like valuation concerns and analyst price target trims due to volatility in regulated utilities have introduced some caution.

Regulatory risks, including approvals for rate hikes and environmental compliance, also play a role. Despite these, Entergy’s financial metrics, including strong cash flow from operations, support its upward momentum.

Comparing Entergy to the Nasdaq

To assess outperformance, let’s compare key metrics. Year-to-date through December 2025, Entergy shares have risen approximately 23%, outpacing the Nasdaq Composite’s 19% gain.

Over the past 52 weeks, ETR is up 24.7%, compared to the Nasdaq’s 21% advance.

This edge highlights Entergy’s resilience as a defensive stock in a market dominated by tech-heavy growth names on the Nasdaq.While the Nasdaq has been buoyed by AI and semiconductor booms, Entergy’s gains stem from more predictable utility fundamentals. For context, Entergy’s current price hovers near $93-94, with a 52-week high around $97, reflecting steady but not explosive growth.

In contrast, the Nasdaq’s volatility—driven by mega-cap tech—has led to sharper swings, making Entergy a more stable option for diversified portfolios.

|

Metric

|

Entergy (ETR)

|

Nasdaq Composite

|

|---|---|---|

|

Year-to-Date Return

|

+23%

|

+19%

|

|

52-Week Return

|

+24.7%

|

+21%

|

|

Current Price (approx.)

|

$93.65

|

N/A

|

|

Dividend Yield

|

~4.8%

|

N/A

|

What Should Investors Look For?

For those considering Entergy as part of their portfolio, several indicators warrant attention. First, monitor upcoming Q4 2025 earnings, expected in early 2026, for updates on full-year results and 2026 guidance—analysts project EPS around $3.89 for 2025, with potential upside from infrastructure projects.

Regulatory developments, particularly in Entergy’s service territories across the South, could impact rate base growth and profitability.Investors should also watch energy demand trends, including partnerships with tech firms for data center power needs, which could drive long-term revenue. Dividend sustainability remains key; Entergy’s history of consistent payouts makes it appealing, but check payout ratios against earnings growth.

Finally, broader market factors like interest rates and commodity prices (e.g., natural gas) will influence the stock—lower rates could boost utilities by reducing borrowing costs.In summary, Entergy’s outperformance against the Nasdaq underscores its value as a reliable energy play in uncertain times. While not immune to risks, its strong fundamentals and strategic positioning make it worth considering for balanced, income-oriented investing. Stay tuned to Energy News Beat for more updates on the sector.

Sources: nasdaq.com, investtech.com, finance.yahoo.com, simplywall.st, entergy.com

Want to get your story in front of our massive audience? Get a media Kit Here. Please help us help you grow your business in Energy.