For instance, the UAE aims to hit 5 million bpd by 2027, while Guyana’s production has already surged to over 660,000 bpd and could reach 1.3 million bpd by 2030.

OPEC’s call for $18.2 trillion in oil and gas investments by 2050 underscores the long-term bet on hydrocarbons, even as renewable projects—like Saudi Arabia’s 44 GW of tenders—make headlines but fail to displace fossil fuels at scale.

Meanwhile, oil demand continues to climb, driven by economic growth in emerging markets and persistent needs in transportation and petrochemicals. This article examines the surge in oil, natural gas, and liquefied natural gas (LNG) demand over the past decade, contrasts it with the trillions poured into wind, solar, and energy storage, and evaluates whether the Net Zero push has been worth the marginal energy additions to global grids. The data paints a picture of a transition that’s not just stalled—it’s being outpaced by fossil fuel resilience.

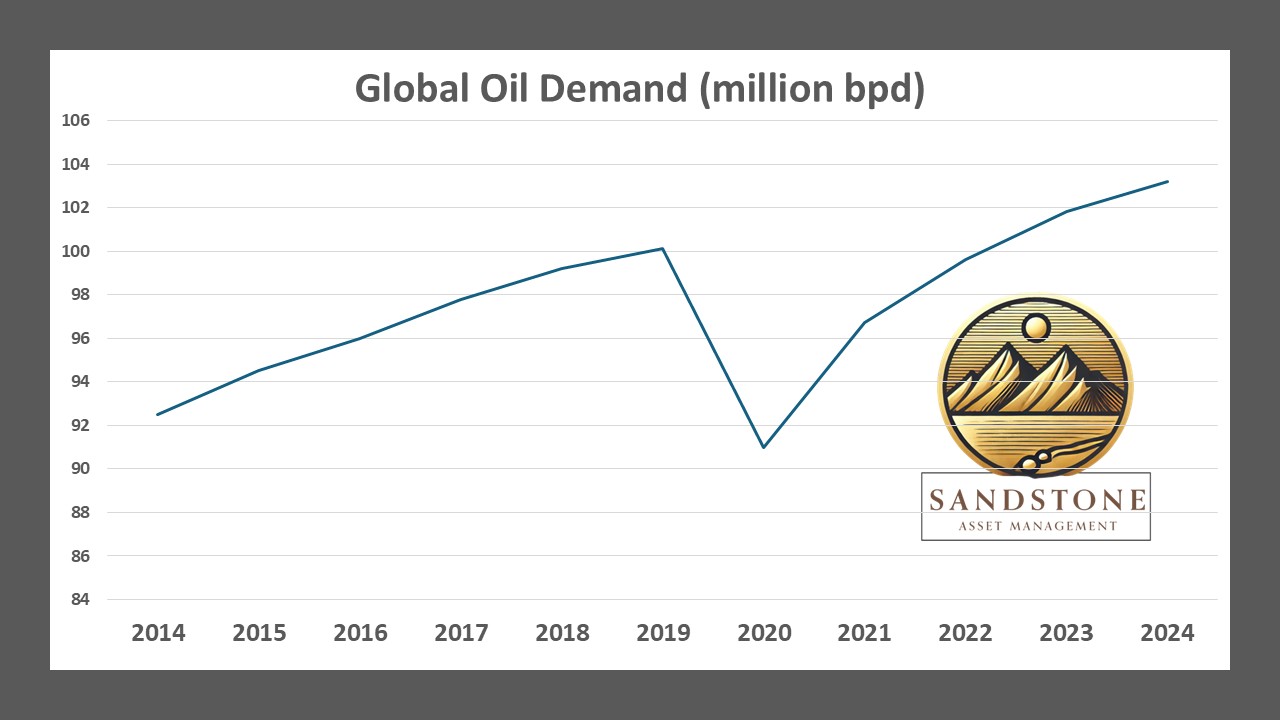

The Unstoppable Rise of Oil Demand

By 2024, it had shattered records, exceeding 103 million bpd for the first time—a roughly 11% increase despite the COVID-19 dip in 2020, when demand plummeted to around 91 million bpd.

This equates to an additional 3,650 million barrels consumed annually in 2024 compared to 2014, representing vast energy volumes primarily fueling transport, industry, and chemicals.

This growth is fueled by emerging economies, with China’s refinery runs hitting two-year highs and naphtha imports poised for records in 2025. Forecasts suggest demand will continue rising to 108 million bpd or more by the early 2030s, challenging the notion of an imminent peak. Production has kept pace, reaching 82.8 million bpd in 2024, led by the U.S. at 13.2 million bpd.

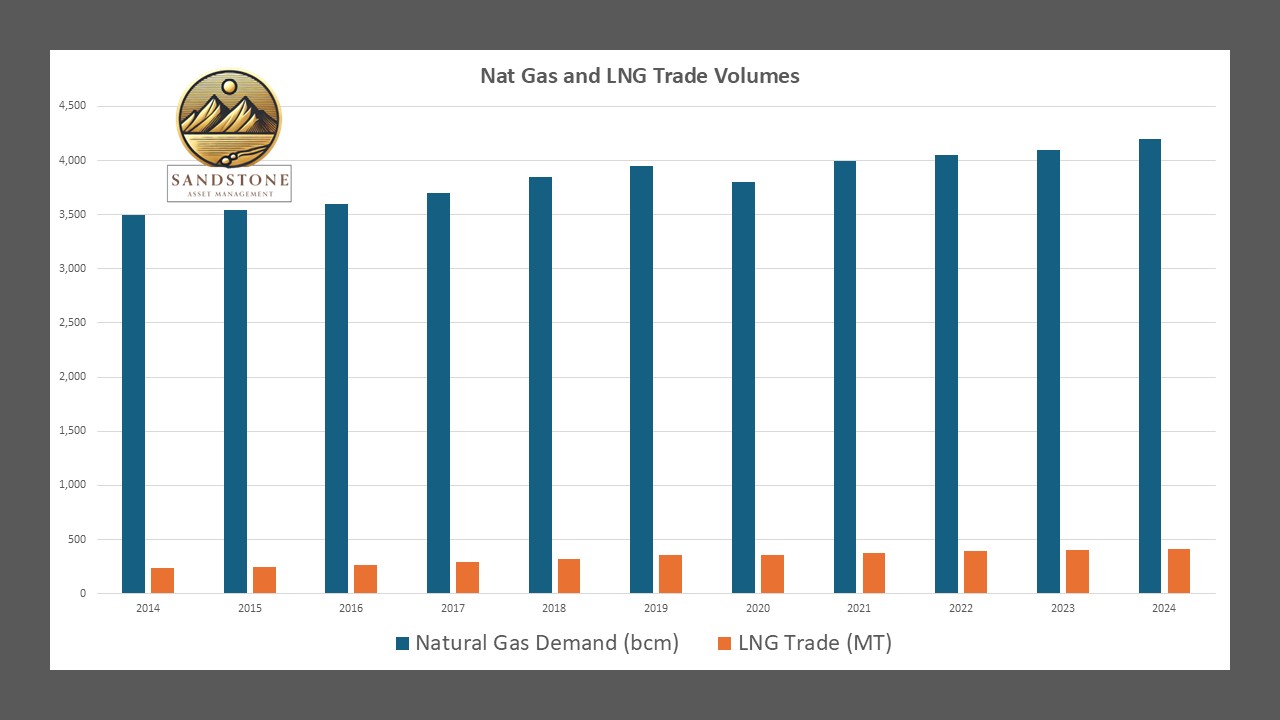

Natural Gas and LNG: A Parallel Surge

Production rebounded by 2% in 2024, with key increases in major exporters.

LNG trade, a key enabler of global gas distribution, has boomed even faster. In 2014, trade volumes were around 241 million tonnes (MT). By 2024, they reached 411.24 MT, a 70% increase, connecting 22 exporters to 48 importers.

This growth averaged 5-11% annually, with 2024 seeing a 2.4% uptick despite high prices.

Projections from the Gas Exporting Countries Forum indicate natural gas demand could rise by another 34% by 2050.

The Renewables Investment: Trillions Spent, Incremental Gains

Focusing on renewables, annual spending on solar PV and wind reached $735 billion in 2023, with cumulative investments from 2014-2024 likely surpassing $4 trillion for these sectors alone.

Battery storage investments have also surged, part of broader clean tech funding, with global spending on energy storage reaching tens of billions annually—e.g., residential storage alone grew at a 51% CAGR to 33.4 GWh installed by 2023.

Yet, the electricity added to global grids from wind and solar tells a tale of inefficiency. In 2014, wind generated about 700 TWh and solar around 200 TWh, totaling ~900 TWh (3% of global electricity).

By 2024, wind hit 2,494 TWh and solar 2,131 TWh, a combined 4,625 TWh (about 15% of ~30,000 TWh total global generation).

That’s a net addition of ~3,725 TWh over the decade.

However, storage doesn’t generate energy—it enables intermittent renewables, with cumulative additions around 350 GWh over the period.Was the Net Zero Cost Worth It?To assess value, consider the cost per unit of added electricity. With ~$4 trillion invested in wind and solar from 2014-2024, the 3,725 TWh addition implies a rough cost of over $1 billion per TWh.

This doesn’t account for grid upgrades, subsidies, or intermittency issues requiring backup (often gas). Storage adds another $500-700 billion in costs for minimal direct energy addition.

Comparatively, oil’s 10 million bpd increase provides energy equivalent to ~6,200 TWh annually (assuming 1 barrel yields ~1.7 MWh thermal energy), far outstripping renewables’ grid additions, and at lower marginal costs for established infrastructure. Natural gas and LNG growth add even more, with gas often serving as a backup for renewables.