In an era defined by the push toward clean energy, electrification, and advanced technologies, critical minerals have emerged as the backbone of modern manufacturing and national security. These essential resources—ranging from lithium for batteries to rare earth elements for magnets—are vital for everything from electric vehicles (EVs) to renewable energy infrastructure and defense systems.

However, the United States faces significant vulnerabilities in its supply chains, with heavy reliance on foreign sources, particularly China, which dominates global production and refining. As of October 2025, the U.S. Geological Survey (USGS) has released a draft list of 54 critical minerals, expanding from the 2022 list of 50 by adding commodities like copper, silicon, potash, silver, rhenium, and lead while removing arsenic and tellurium.

This article examines the top 15 critical minerals most relevant to the U.S. energy transition and manufacturing, their global sources, refining capacities, and production of usable materials. It also assesses China’s control, U.S. progress in securing supplies, and the path to independence.

Why Critical Minerals Matter

Critical minerals are defined by their economic importance and high risk of supply disruptions, as per the Energy Act of 2020, which mandates USGS updates every three years.

For the energy sector, minerals like lithium, cobalt, nickel, graphite, and rare earth elements are indispensable for batteries, wind turbines, and solar panels. The International Energy Agency (IEA) highlights that demand for these could quadruple by 2040 under net-zero scenarios, driven by the global shift to clean energy.

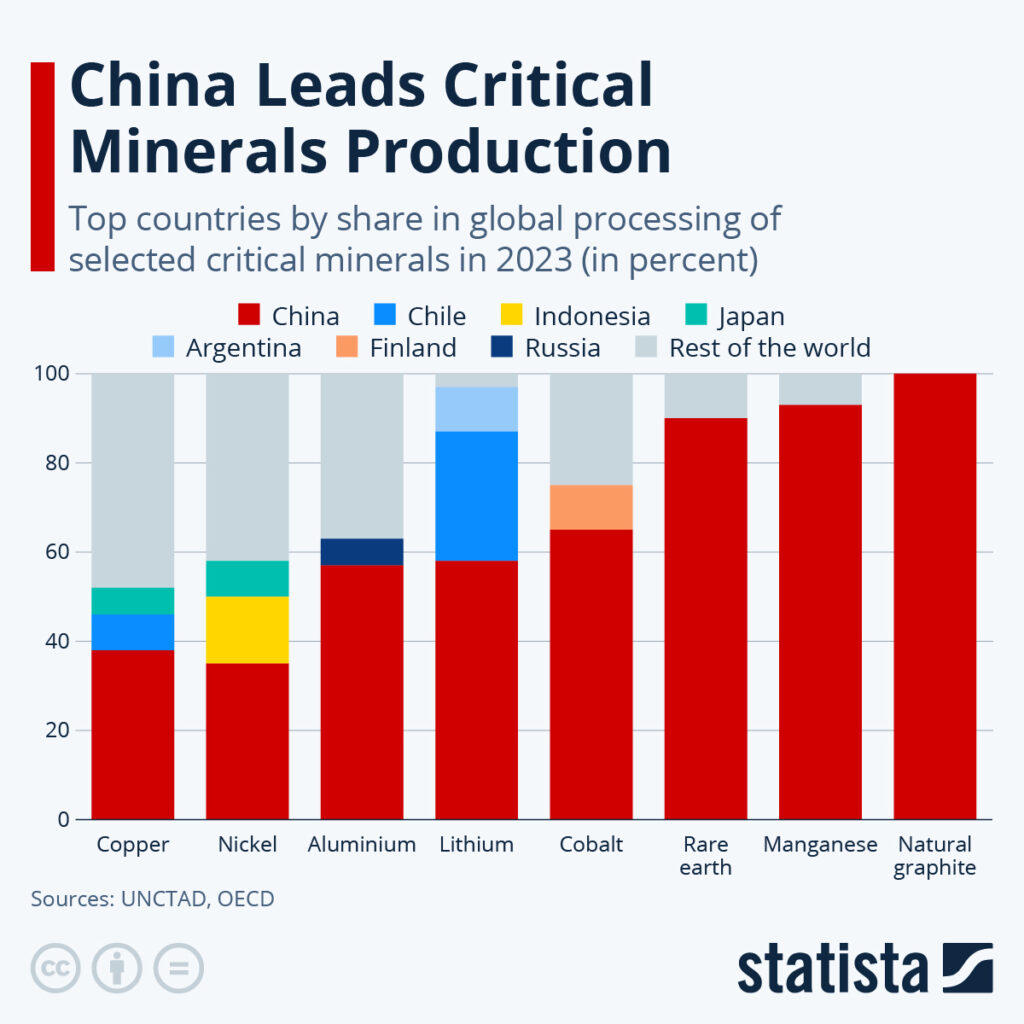

Yet, concentrated supply chains pose risks: geopolitical tensions, export restrictions, and environmental challenges can lead to price volatility and shortages. China’s dominance in processing—often exceeding 70-90% for key minerals—amplifies these concerns, especially amid recent export curbs on rare earth technologies and elements like gallium and germanium.

Top 15 Critical Minerals: Sources, Refining, and Usable MaterialsBased on USGS and Department of Energy (DOE) assessments, as well as IEA reports, the following table summarizes the top 15 critical minerals prioritized for the U.S. energy transition. Selection focuses on those with high import reliance, supply risks, and relevance to clean tech. Data includes primary global sources (mining), refining capacity shares, and processes for creating usable materials (e.g., metals, compounds, or alloys for manufacturing). China’s control is quantified where possible, alongside U.S. domestic or secured shares.

Mineral

Key Uses in Manufacturing

Primary Sources (Mining)

Refining Capacity (Global Shares)

Creation of Usable Materials

China’s Control (%)

U.S. Secured/Share (%)

Lithium

EV batteries, energy storage

Australia (50%), Chile (30%), China (10%)

China (60-70%), Australia/Chile (20-30%)

Extracted as brine/carbonate, refined to hydroxide/carbonate for cathodes

60-70% refining

~5% domestic (Nevada projects); imports 100% net reliance

Cobalt

Battery cathodes, alloys

DRC (70%), Australia (5%), Indonesia (5%)

China (70%), Finland/Belgium (15-20%)

Refined to sulfate/metal for battery precursors

70% refining

<5% domestic; ~20% via allies (e.g., Australia)

Nickel

Battery cathodes, stainless steel

Indonesia (50%), Philippines (15%), Russia (10%)

China (35-40%), Indonesia (20-25%)

Smelted to matte/sulfate for NMC batteries

35-40% refining

~10% domestic; high import from Canada/Indonesia

Graphite

Battery anodes, lubricants

China (80%), Brazil/Mozambique (10%)

China (90%), synthetic from U.S./Europe (5-10%)

Processed to spherical graphite for anodes

80-90% mining/processing

0% domestic mining; 100% import reliance

Rare Earth Elements (group)

Magnets for EVs/wind turbines, electronics

China (60%), Australia (15%), Myanmar (10%)

China (90%), Malaysia/Australia (5-10%)

Separated into oxides/metals for neodymium magnets

60% mining, 90% processing

~5% domestic (Mountain Pass); ~15% via allies

Copper

Wiring, motors, renewables

Chile (30%), Peru (10%), China (10%)

China (40%), Chile/Japan (20-25%)

Smelted to cathodes for wire/foil

40% refining

~15% domestic; net exporter of ore but importer of refined

Manganese

Battery cathodes, steel

South Africa (35%), Gabon (20%), Australia (15%)

China (80%), South Africa (10%)

Ferromanganese alloys for steel/batteries

80% processing

0% domestic; 100% import

Gallium

Semiconductors, LEDs

China (95%), Germany/Japan (minimal)

China (95%)

Refined from bauxite to arsenide for chips

95% production

0% domestic; 100% import

Germanium

Fiber optics, solar cells

China (60%), Russia (20%)

China (80%)

Refined to dioxide for optics/semiconductors

80% processing

Minimal domestic; high reliance

brookings.edu

Indium

Solar panels, screens

China (50%), South Korea (20%)

China (60%)

Refined to oxide for ITO coatings

60% processing

0% domestic

crossdockinsights.com

Tantalum

Capacitors, alloys

DRC/Rwanda (50%), Brazil (20%)

China (40%), Estonia/Germany (30%)

Refined to powder for electronics

40% processing

Minimal; recycling efforts

crossdockinsights.com

Tungsten

Alloys, electronics

China (80%), Vietnam (5%)

China (85%)

Refined to carbide for tools

85% production

~10% domestic

brookings.edu

Antimony

Flame retardants, batteries

China (55%), Russia (20%)

China (80%)

Refined to trioxide for alloys

80% processing

Minimal

atlanticcouncil.org

Bismuth

Alloys, pharmaceuticals

China (70%), Mexico (10%)

China (80%)

Refined for low-melt alloys

80% production

Low domestic

brookings.edu

Fluorspar

Steel, aluminum, chemicals

China (50%), Mexico (20%)

China (60%)

Acid-grade for HF in manufacturing

60% processing

~20% domestic

crossdockinsights.com

Sources: Compiled from USGS, IEA, and DOE data.

China’s overall dominance stems from strategic investments since the 1980s, controlling 60% of rare earth mining and up to 95% for gallium, often through state-backed firms.

The U.S. relies on imports for over 50% of 43 critical minerals, with 100% net reliance on 12, including graphite and gallium.

“This mine is one that could basically drive civilization over the next 20, 30, 50 years,” Christopher Messina, CEO of Tanbreez, told me in a recent interview. For the United States and its needs, that is probably no exaggeration given that the resource was recently ranked by Mining.com as #1 on its list of Top 10 rare earth mining projects in the world. The total estimated recoverable resource at Tanbreez of 28.2 Mt. compares to the combined resource in the #4 through #8 mines on the list.

It is an enormous potential resource, on an island nation adjacent to the North American coastline. It can be recovered with current technology with minimal environmental disturbance, and Greenland’s own government is in favor of moving ahead.

It is no accident that the Trump government moved in recent weeks to try to secure a 50% equity interest in that very mine. Indeed, the mine’s existence was the main reason why President Trump spent so much time talking about his desire to purchase the island entirely in the early weeks of his administration.

China’s Control and U.S. Security Measures

China controls an average of 60-80% of global refining for these minerals, leveraging low costs, subsidies, and vertical integration.

Recent actions, such as export restrictions on rare earth technologies (December 2023) and expansions in October 2025 to include five more elements, signal weaponization amid U.S.-China tensions.

This has prompted U.S. responses: The Inflation Reduction Act (IRA) offers tax credits for domestic sourcing, while DOE has invested $60 million in magnet manufacturing and critical materials accelerators.

Executive orders in 2025 mandate immediate increases in domestic production, and initiatives like the Minerals Security Partnership ally with Australia, Canada, and others.

Progress includes new facilities for rare earths in California and lithium in Nevada, but domestic refining remains under 10% for most minerals.

Path to Independence: What Needs to Change and How Fast It Can Happen

Achieving full independence from China is challenging due to geological limits, environmental regulations, and capital needs, but resilience through diversification is feasible. Key changes include:

Streamline Permitting: Reduce mine approval times from 10+ years via reforms like FAST-41 for copper and rare earth projects.

Boost Domestic Refining: Federal initiatives like the Critical Mineral Processing Initiative aim to expand U.S. capacity, targeting 25-50% for key minerals by 2030.

International Partnerships: Invest in allied sources (e.g., Ukraine, Central Asia) and recycling to cut reliance by 20-30%.

R&D and Recycling: Advance alternatives and urban mining to recover 10-20% of needs.

Timeline: Partial resilience (reducing China reliance to <50%) could occur by 2030 for lithium and nickel via IRA-driven projects, but full independence for rare earths and graphite may take 10-15 years, per DOE and Atlantic Council analyses.

Urgent action is needed to avoid disruptions in the energy addition and keep the overall economy moving forward. Since much of this is used in military equipment, the wartime powers act typically comes into effect, and the US invests in mining and companies. We will be watching for investment opportunities.

Industrial output in China grew 4.2% in August year over year, an improvement from the 3.8% growth in July, according to official data released on Friday. It indicates that despite the recent return to Covid […]

NewsNuclear Energy Seoul and Warsaw have signed outline agreements to develop nuclear power in Poland, according to ministries from both countries, as Poland strives to phase out coal and lower its carbon emissions and South […]

China’s suspension of climate dialogue with the US has raised concerns that progress on some issues could be delayed, such as the implementation of a global cross-border emissions trading mechanism and bilateral collaboration in key […]

We use cookies to ensure that we give you the best experience on our website. If you continue to use this site we will assume that you are happy with it.