The global push toward net zero emissions has been a cornerstone of climate policy and investment strategy for years, but recent developments suggest a significant shift. Major banks, once vocal supporters of environmental, social, and governance (ESG) initiatives, are increasingly retreating from these commitments. This trend raises critical questions for investors in the energy sector: What does it mean for portfolio returns, particularly when comparing renewable energy stocks like wind, solar, and hydrogen to traditional oil, gas, and liquefied natural gas (LNG) companies? Drawing from recent market data and insights from industry analyses, this article explores the implications, compares historical returns, and outlines what investors should prioritize moving forward.

Look to the banks and insurance companies to decide where to invest and find returns. When financial institutions try to force behavior, things don’t go as planned.

Are you from California, New Jersey or New York and need a tax break?

Why Banks Are Abandoning Net Zero Goals

The retreat from net zero isn’t happening in a vacuum. Political pressures, especially following the re-election of Donald Trump—who has championed fossil fuels with his “drill baby drill” mantra and previously withdrew the U.S. from the Paris Climate Agreement—have played a pivotal role. Banks are also facing shareholder demands to prioritize tangible business value over costly ESG programs that haven’t always delivered results. Regulatory hurdles, such as challenges in climate scenario analysis and data access for risk assessment, further complicate implementation. Critics argue that many net zero pledges were more about public relations than substantive change, with distant targets like 2050 offering little immediate accountability.

Specific examples abound. Goldman Sachs exited the UN’s Net Zero Banking Alliance (NZBA) shortly after Trump’s election, followed by JPMorgan, Citi, Bank of America, Morgan Stanley, and Wells Fargo. Canadian banks like Royal Bank of Canada and Toronto-Dominion also departed, erasing North American representation in the alliance. HSBC delayed its net zero target by 20 years and shelved a carbon credits desk, while Barclays and Lloyds watered down their pledges, including removing climate goals from executive bonuses and easing restrictions on long-haul flights.

This exodus could slow the energy transition by reducing funding for low-carbon projects. For investors, it signals potential volatility: renewables may face tighter capital access, while fossil fuels could see renewed support amid policy shifts favoring domestic production.

Comparing Investor Returns: Renewables vs. Fossil Fuels

To gauge the impact on investors, let’s examine stock performance in key subsectors. We’ve focused on year-to-date (YTD) returns as of mid-2025 and 5-year total returns, using representative top companies and sector indices. Data is drawn from market analyses and reflects the broader trends: renewables have struggled amid high interest rates, supply chain issues, and policy uncertainty, while oil, gas, and LNG stocks have benefited from steady demand and geopolitical tensions driving prices.

Sector-Level Comparison

Broad indices provide a high-level view:

The clean energy index peaked in early 2021 but has since declined sharply due to rising interest rates impacting project financing.

In contrast, the energy sector saw massive gains in 2022 (65.72%) from post-pandemic recovery and the Ukraine conflict, though returns moderated in subsequent years.

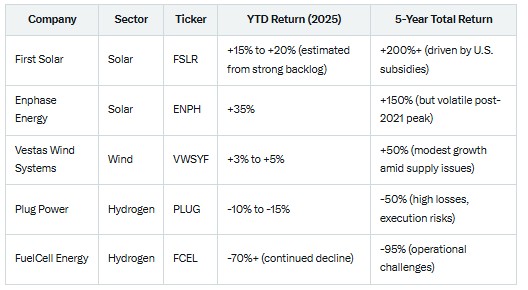

Company-Level Comparison: Top Renewables

Top wind, solar, and hydrogen firms have shown mixed but generally underwhelming performance, with some outliers in niche areas like wave energy. Many have faced cost inflation and competition.

Hydrogen stocks like FuelCell have been particularly hard-hit, with massive losses over five years due to scaling difficulties and unprofitable projects.

Solar leaders like First Solar benefited from the Inflation Reduction Act, but overall, the sector’s YTD underperformance reflects broader clean energy woes.

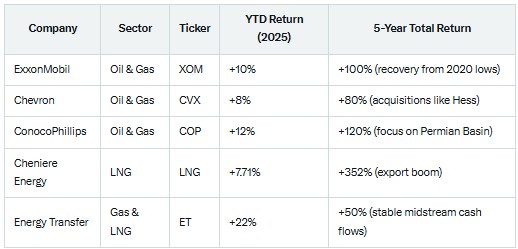

Company-Level Comparison: Top Oil, Gas, and LNG

Fossil fuel giants have delivered more consistent returns, supported by high dividends and cash flows from elevated commodity prices.

LNG players like Cheniere have shone, with 5-year returns exceeding 350% amid global demand for U.S. exports.

Oil majors like Exxon have balanced fossil production with lower-carbon investments, yielding solid gains.

The oil & gas exploration and production (E&P) industry as a whole posted a 14.83% YTD return, outperforming the S&P 500’s 7.88%.

In summary, over the past five years, fossil fuel stocks have generally outperformed renewables, with average annualized returns of 4-7% for energy sector indices versus flat or negative for clean energy. YTD trends amplify this gap, as banks’ retreat exacerbates funding shortages for capital-intensive renewables.

What Investors Should Look For

As banks pull back from net zero, investors face heightened risks in pure-play renewables but opportunities in diversified energy plays. Key factors to consider:

Strong Balance Sheets and Cash Flows: Prioritize companies with low debt and stable revenues, like midstream gas firms (e.g., Enbridge) or integrated oil majors (e.g., Exxon), which can weather volatility.

Policy and Regulatory Support: Monitor U.S. subsidies under the Inflation Reduction Act for renewables, while anticipating shifts under pro-fossil administrations. Globally, EU green deals could bolster wind and solar.

Diversification and Transition Strategies: Firms bridging fossils and renewables, such as NextEra Energy (with solar and gas) or Chevron (investing in hydrogen), offer resilience.

Dividend Yields and Value Metrics: Fossil stocks often pay higher dividends (e.g., 4-6% for pipelines), appealing in uncertain times. Avoid overvalued hydrogen plays with negative earnings.

Long-Term Demand Trends: Despite the retreat, global energy demand will rise; renewables could rebound with technological advances, while LNG bridges the gap to cleaner fuels.

Consult your tax professional, as there are oil and gas investments offering tax advantages with good returns. These are in the private sector and not all are equal, so do your homework.

In a world where banks are ditching net zero, investors must balance idealism with pragmatism. While renewables promise future growth, current data favors fossil fuels for near-term stability. Diversifying across both, with an eye on adaptable companies, could mitigate risks and capture upside in the evolving energy landscape.

Avoid Paying Taxes in 2025

Crude Oil, LNG, Jet Fuel price quote

ENB Top News

ENB

Energy Dashboard

ENB Podcast

ENB Substack