Solar power in California just had a good decade. Thanks to strong policy and, yes, good sun, solar expanded to become a significant proportion of the state’s electricity mix and help substantially decarbonize its power generation fleet. It has been so successful, in fact, that its previous success imposes challenges on its future. Solar has become the snake that eats its own tail, reducing its own revenue and creating new imperatives for solar generators.

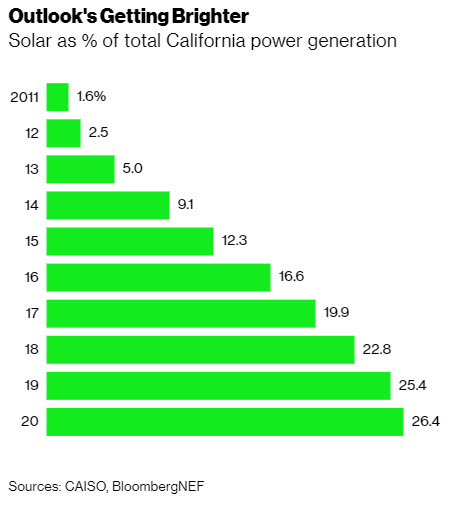

Here are two ways of looking at that success. The first is as a percentage of total power generation. In 2011, solar was just 1.6% of the state’s electricity mix; in 2020, it was 26.4%, growing 15-fold in 10 years. That percentage also makes solar the second-largest source of power in the state, after natural gas and ahead of nuclear and wind.

Solar is a huge part of California’s zero-carbon electricity ambitions. The state’s annual electricity demand is about the same as it was 15 years ago, which means that all this new solar power is displacing something else in the grid. This is a good thing from an emissions perspective in that solar is displacing hydrocarbon fuels. In so doing, though, it upends the dynamics of the California power market.

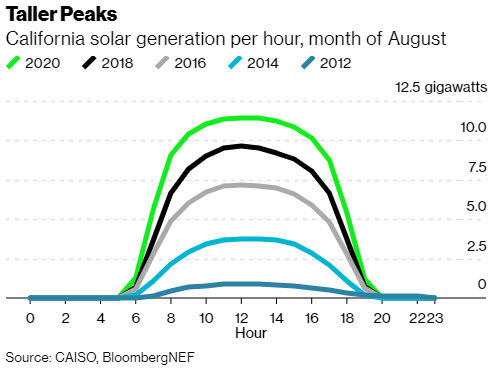

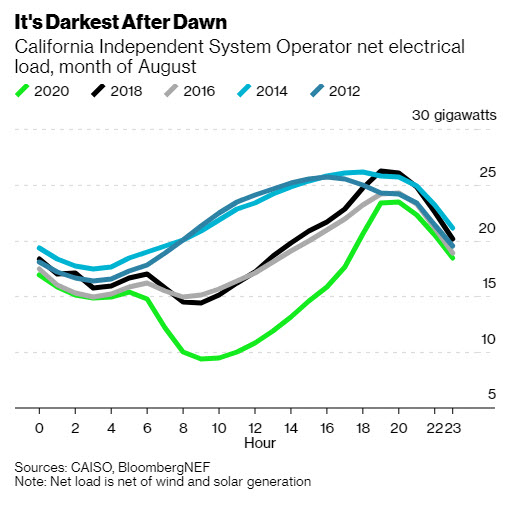

Back in the day, thermal power plant generation ramped up when demand was highest—usually early afternoon, close to midday—and then down again as it dropped. But because solar is mostly consumed as it’s generated, it reduces net demand during peak solar hours—also around midday—and then creates a spike in demand as the sun sets. This net demand curve—dubbed the “duck curve” by the California Independent System Operator—no longer has a midday peak; in fact, midday is when net demand is at its lowest. This feature of the net demand curve becomes more pronounced every year.

Here is where solar begins to eat its own tail, reducing and eventually destroying some of the economic benefits it once created. In a competitive power market, the marginal unit that satisfies total demand sets the price that all competitive generators receive. Historically, that unit would have been a gas plant with a high marginal cost, designed to run during summer midday hours; the result of that paradigm was high prices for any generator operating at those hours.

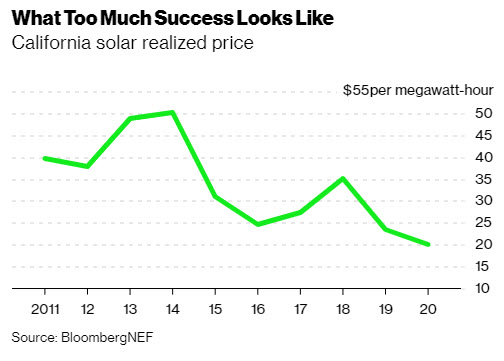

That was good for the early solar plants. However as solar generation increased and net demand fell further and further, fewer other power generators were needed to meet that net demand during solar hours. Those generators were lower-cost, with the result being that solar’s realized price—what it earns during generating hours—has fallen steadily. Last year it was barely $20 per megawatt-hour, down from $50/MWh in 2014.

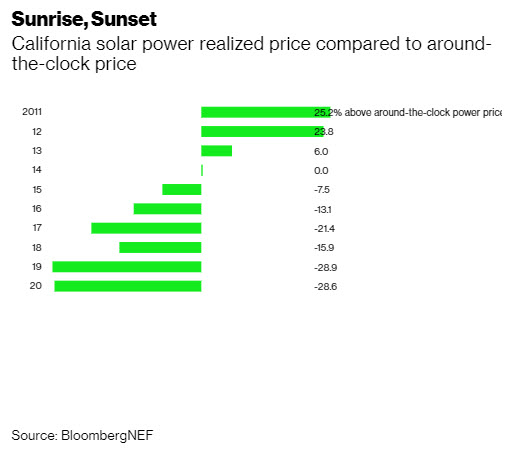

There’s another wrinkle to this realized price phenomenon. Solar’s challenge is not just that its realized price has fallen; it’s also that the realized price is now a substantial haircut to the “around the clock” power prices that plants with 24-hour operations see. In 2011, when a small volume of solar captured high daytime prices, solar generators saw a significant premium to the around-the clock price. Today, a large volume of solar has depressed daytime prices, and solar generators now see a noticeable discount to the around-the-clock price.

This realized price trend is a problem in search of a solution. One certainly exists already: utility-scale energy storage in the form of large batteries that can store bulk power during solar hours and discharge it again when demand peaks in the evening. California has already studied the notion in depth, and there are plenty of commercial developers already pursuing utility-scale solar and storage projects.

Another solution is something I’ve written about before in the case of even more solar-rich South Australia: creating new sources of demand. Get used to this refrain, and not just from me. Abundant, inexpensive, zero-carbon electrons are in search of companies and business models to use them. Those could include electrolyzing hydrogen, performing energy-intensive computation in large data centers, charging electric vehicles, or—just as importantly—other electricity-intensive processes and businesses that do not yet exist.

1 Trackback / Pingback

Comments are closed.