US Treasury Secretary Janet Yellen is at the forefront of calls for a cap on Russian oil export prices. Sounds like a great idea. Just don’t expect it to work.

Here’s the problem. Russia earns billions of dollars from exporting oil. Those dollars are helping to fund President Vladimir Putin’s invasion of Ukraine. Meanwhile, the world needs Russian oil to keep flowing because markets are already tight and nobody has spare capacity to make up for its loss. But countries in North America, Europe and parts of Asia want to cut off the flow of funds to the Kremlin’s war machine.

So, what’s the solution? Revenue is a pretty simple product of volume times price (minus some costs). To cut the Kremlin’s revenue, you need to hit either volume or price. We don’t want to reduce the volume, so that leaves price. Restrict the price at which Russia can sell its oil, and you reduce the Kremlin’s revenue without hitting the volume of oil on the international market.

Neat, simple, I wonder why nobody’s done it before. Why didn’t the US do this with Iran or Venezuela, rather than imposing secondary sanctions that cut off oil flows and damaged relations with trading partners in Asia? Perhaps the main reason is: It stands very little chance of actually working.

Under the plan, insurance would be withheld from cargoes for which the buyer pays Russia more than an as-yet-to-be-determined price. Since about 95% of the world’s tanker fleet is insured through the International Group of Protection & Indemnity Clubs in London and some firms based in continental Europe, a ban is certainly feasible. But I’m not convinced it’s enough.

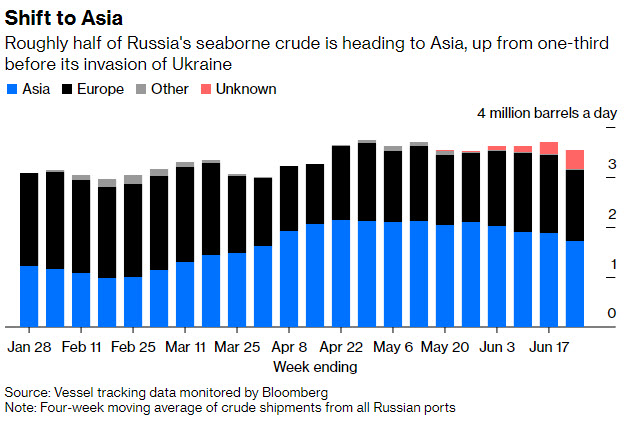

The European Union has just concluded several weeks of brutal internal wrangling over oil sanctions on Russia. Those sanctions, even watered down from the original proposals, included a ban on insurance. Moscow has already begun to put in place an alternative to the P&I clubs, offering insurance through the Russian National Reinsurance Company. That may be good enough for some of the Indian and Chinese companies that are now providing the bulk of the market for Russian crude.

The plan being pushed by Yellen would require the EU to revoke the sanctions it has just agreed to — not an attractive option after the bruising negotiations the bloc went through to get them accepted by all 27 members. I can’t see many European countries being keen to agree on new sanctions that would allow Chinese and Indian companies to buy heavily discounted crude, while their own are prohibited from purchasing at any price. It’s more likely that the EU ban on seaborne imports of Russian crude and refined products would end up being dropped alongside that on insurance.

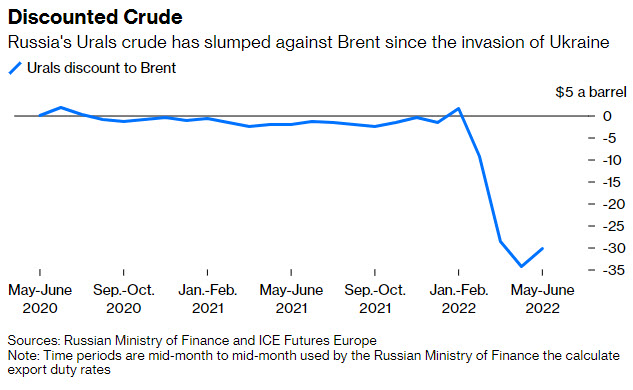

So we’d end up with no attempt to cut the volume of Russian oil exports in the hope — and it still would be just a hope — of being able to reduce their value. But the value of Russia’s crude shipments has already been hit.

Figures from the Russian Ministry of Finance show that since the attack on Ukraine was launched in February, the price of Russia’s benchmark Urals export grade has plummeted relative to Brent, a global benchmark based on crude produced in the North Sea. That discount averaged almost $35 a barrel between mid-April and mid-May, although it narrowed a bit the following month, widening from an average of $1.50 a barrel in the 12 months before the invasion.

The widening discount has probably cost Russia about $7 billion in income from its seaborne crude exports, compared with what it would have earned had Urals retained its historical price relationship to Brent. The figure would rise to $10 billion by the end of July.

The biggest obstacle to capping Russian oil prices, though, is Putin just saying, “No.” How do you compel Russia to sell its oil at an externally imposed discount?

You could set the cap at a level that ensures a small positive return for Russian oil companies in the hope they’ll decide it’s still worth pumping, but they’re not the ones making the decision. Their oil is carried to market (either directly or to export terminals on the Russian coast) by a pipeline network that’s owned by the Russian state. Putin simply has to close the valves on those pipes and the companies can’t export, even if they want to.

The Russian president has already shown that the country’s economy is of secondary importance to his imperialist ambitions, as his troops lay waste to eastern Ukraine. His calculation will almost certainly be that cutting off Russian oil exports will do more damage to the economies of buyers in Europe than it will to Russia. So it’s hopeless to expect him to acquiesce to a price cap imposed by the West.

Source: Bloomberg