In a significant pivot within the global energy landscape, China—the world’s largest oil importer and refiner—has ramped up its exports of refined petroleum products, including gasoline and diesel, as domestic demand softens and overseas margins prove more lucrative. This shift, accelerating in 2025, reflects broader economic and structural changes in China’s energy sector. As refiners capitalize on export opportunities, questions arise about the implications for internal consumption, crude oil demand, and the broader global market.

The Drive Behind Increased Fuel Exports

China’s fuel exports are projected to hit a 16-month high in July 2025, with combined shipments of gasoline, diesel, and other light and middle distillates reaching approximately 859,000 barrels per day (bpd), up from 796,000 bpd in June. This surge is primarily driven by refining margins that have climbed above $20 per barrel for gasoil, a more than 50% increase since March, making international sales far more profitable than domestic ones. Refiners have also benefited from unused export quotas allocated by the central government, with half of the annual quota still available as of mid-2025.

The end of seasonal maintenance periods has further boosted refinery throughput, which rose 8.5% year-over-year to 15.2 million bpd in June. However, this increased activity contrasts with sluggish domestic fuel demand, prompting refiners to redirect output abroad. In the first half of 2025, China released 12.8 million metric tons (mt) of clean oil product export quotas and 5.2 million mt for low-sulfur fuel oil (LSFO), marking a 10% year-over-year increase for LSFO. Gasoil exports alone are expected to soar 88% month-over-month in July, underscoring the export-led strategy.

Key Customers and Export Destinations

China’s refined fuel exports are finding eager buyers across Asia-Pacific and beyond, with regional hubs absorbing the bulk of shipments. Singapore remains the dominant destination for gasoline, accounting for 72.3% of Southeast Asian imports from China in the first half of 2025 and taking in 674,100 tons in April alone. Malaysia follows, though its volumes dipped 74.83% in April amid regional market fluctuations.

For diesel (gasoil), the Philippines led with 1,185,000 mt in the first half of the year (down 16% year-over-year), followed by Hong Kong at 583,000 mt (up 28%) and Australia at 264,000 mt (down 52%). Emerging markets like Mexico have also ramped up purchases, importing 176,000 mt of Chinese gasoline in the first five months—a 149.6% surge year-over-year—driven by competitive pricing and supply needs. Other notable importers include Pakistan and various Southeast Asian nations, where Chinese fuels help bridge local refining shortfalls.

These destinations highlight China’s role as a key supplier in the Asia-Pacific refining ecosystem, where Singapore acts as a trading and blending hub, redistributing fuels to further markets.

The Downstream Market in China: Refining and Petrochemical ShiftsChina’s downstream sector, encompassing refining, petrochemical production, and distribution, is undergoing a transformation amid these export trends. The market is projected to grow at a compound annual growth rate (CAGR) exceeding 4.58% through the forecast period, driven by investments in petrochemicals rather than traditional fuels. Refineries are increasingly focusing on higher-value products like naphtha and aromatics for plastics and chemicals, as fuel demand plateaus.

In 2025, the sector faces challenges from overcapacity and policy shifts, including reduced value-added tax rebates on certain exports, which could temper competitiveness. However, state-owned giants like Sinopec and PetroChina are adapting by integrating refining with petrochemical operations, aiming to offset weak fuel margins. The midstream and downstream oil and gas market is expected to expand, with a focus on efficiency and green technologies, though overall refinery throughput may stagnate due to domestic demand constraints.

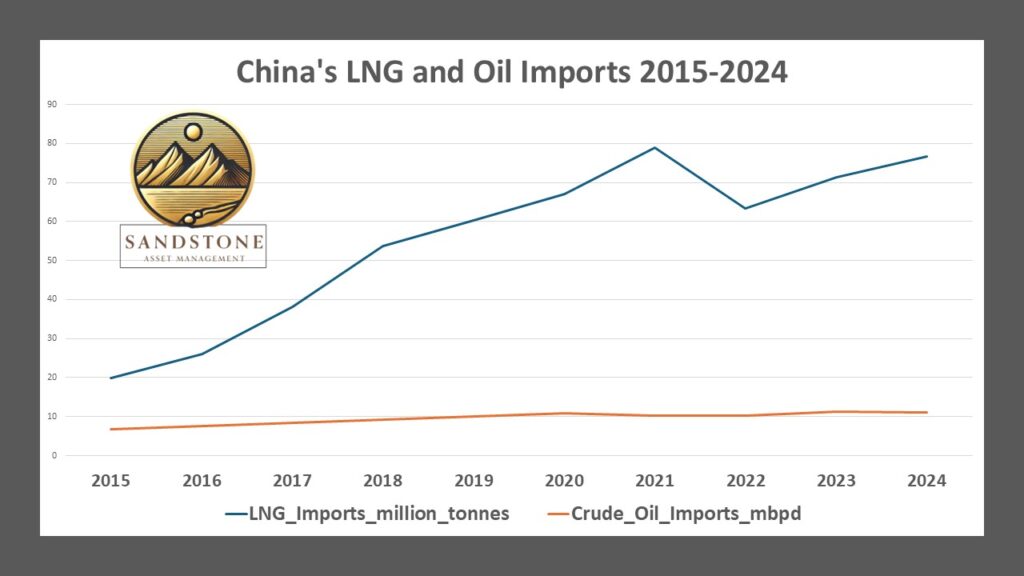

China’s LNG and Crude Oil Imports (2015-2024)

Below is a summary of China’s annual imports for liquefied natural gas (LNG) in million tonnes and crude oil in million barrels per day (mbpd) over the last 10 years (2015-2024). This data is compiled from official sources such as Chinese customs reports, the U.S. Energy Information Administration (EIA), and industry analyses. Note that figures represent annual averages or totals, and minor variations may exist across sources due to rounding or methodological differences.

|

Year

|

LNG Imports (million tonnes)

|

Crude Oil Imports (mbpd)

|

|---|---|---|

|

2015

|

19.82

|

6.71

|

|

2016

|

26.07

|

7.63

|

|

2017

|

38.13

|

8.43

|

|

2018

|

53.78

|

9.24

|

|

2019

|

60.26

|

10.12

|

|

2020

|

67.13

|

10.85

|

|

2021

|

78.93

|

10.26

|

|

2022

|

63.44

|

10.17

|

|

2023

|

71.32

|

11.28

|

|

2024

|

76.65

|

11.04

|

Key observations:

- LNG imports saw rapid growth from 2015 to 2021, peaking at 78.93 million tonnes in 2021, before a dip in 2022 due to high global prices and domestic economic factors. They recovered in 2023-2024 but remain below the 2021 peak.

- Crude oil imports steadily increased over the period, with a record high of 11.28 mbpd in 2023, followed by a slight decline in 2024 amid softening domestic demand and economic shifts.

Data sourced from the Chinese General Administration of Customs, EIA reports, and industry publications.

Is Internal Demand for Petroleum Products Lowering?

Yes, China’s domestic demand for petroleum products is indeed declining, marking a structural shift away from fossil fuels. In 2024, consumption of oil-based fuels—gasoline, diesel, and jet fuel—stood at 8.1 million bpd, 2.5% below 2019 levels, and is expected to see another narrow decline in 2025. Gasoline demand has fallen sharply, returning to 2022 levels during Shanghai’s zero-COVID lockdowns, primarily due to electric vehicle (EV) penetration, which accounted for half of new car sales in 2025 and displaced 3.5% of potential fuel demand.

Diesel consumption has dropped 3.52% in the first half of 2025, hit by a sluggish construction sector and the rise of liquefied natural gas (LNG)-powered trucks, which displaced another 2% of demand. Broader factors include economic rebalancing toward services and high-tech manufacturing, expanded public transport like high-speed rail (aiming for 50,000 km by 2025), and government policies promoting energy security and pollution reduction. Refined oil demand is forecasted to decline at a faster pace in 2025, accelerating from previous years as green development intensifies.

Analysts from CNPC now predict China’s overall oil demand could peak at 15.4 million bpd in 2025, earlier than prior estimates.

Is Internal Demand for Petroleum Products Lowering?

China’s domestic demand for petroleum products is indeed declining, marking a structural shift away from fossil fuels. In 2024, consumption of oil-based fuels—gasoline, diesel, and jet fuel—stood at 8.1 million bpd, 2.5% below 2019 levels, and is expected to see another narrow decline in 2025. Gasoline demand has fallen sharply, returning to 2022 levels during Shanghai’s zero-COVID lockdowns, primarily due to electric vehicle (EV) penetration, which accounted for half of new car sales in 2025 and displaced 3.5% of potential fuel demand.

Diesel consumption has dropped 3.52% in the first half of 2025, hit by a sluggish construction sector and the rise of liquefied natural gas (LNG)-powered trucks, which displaced another 2% of demand. Broader factors include economic rebalancing toward services and high-tech manufacturing, expanded public transport like high-speed rail (aiming for 50,000 km by 2025), and government policies promoting energy security and pollution reduction. Refined oil demand is forecasted to decline at a faster pace in 2025, accelerating from previous years as green development intensifies.

One key note is that Stu Turley on the Energy News Beat podcast has been saying the global demand portion of the oil pricing formulas depends on China and India. If India’s growth outpaces China’s decline, we will have strong support for the $80 range in oil. The lack of investment in drilling is the cause, and we need trillions of dollars to meet normal decline curves. Investing in oil and natural gas production is a great balance for portfolios.

Analysts from CNPC now predict China’s overall oil demand could peak at 15.4 million bpd in 2025, earlier than prior estimates.