Annual Energy Outlook 2022: Extended and Sunset Tax Credit Cases

Executive Summary

We released our Annual Energy Outlook 2022 (AEO2022) in March. The AEO2022 Reference case assumes that existing laws and regulations remain as enacted throughout the projection period, including when the laws or policies are scheduled to end (or sunset). However, laws and regulations often change, creating uncertainty in energy system outcomes. For example, tax credits supporting wind and solar electric generation are often extended year to year, and efficiency standards are a frequent subject of legislative and executive debate and action.

Extending the duration of renewable tax credits beyond their current expiration dates both decreases electricity prices and increases renewable generation capacity relative to the AEO2022 Reference case. Extending energy efficiency incentives reduces energy consumption in the commercial and residential sectors. Starting in 2023, sunsetting renewable tax credits has a smaller effect on both utility-scale solar and wind capacity and distributed generation adoption. Energy consumption remains about the same, in part, because most of the energy efficiency incentives expire at the same time or only slightly earlier than in the AEO2022 Reference case. Electricity prices are slightly higher throughout the projection period because sunsetting tax incentives early results in less solar and wind generation; generation from higher-cost fuels, such as natural gas, takes its place.

This Issues in Focus article presents two cases related to the availability of select tax credits and federal efficiency incentives. We analyze how extending tax credits for renewable energy and combined-heat-and-power technologies or how ending the credits by 2023 could affect long-term renewable and distributed generation deployment and the mix of resources used for electricity generation. We also explore how changing the timespan of available energy efficiency incentives affects end-use demand for energy, electricity prices, equipment stocks, and building shell efficiencies over time.

Unless otherwise specified, the cases in this article start with the AEO2022 Reference case and change particular assumptions to address uncertainty about the future of selected existing laws and regulations.

In this analysis, we quantify uncertainties in energy system inputs associated with a specific set of potential future changes in laws and regulations. We do not represent the full range of policy options available to energy policymakers. We also do not express a view on the likelihood of the assumed policy changes.

Although this analysis focuses on federal efficiency incentives and tax credits, we do not assume an extension or update to tax credits for electric vehicles or Corporate Automobile Fuel Economy (CAFE) standards, which can affect overall energy demand and prices.

’s long-term outlooks do not incorporate the effects of state-level and local policies that have not been enacted into law, such as roadmaps and targets to reach net-zero electricity or renewable energy goals, which can offer additional incentives for deployment of low- and zero-emission resources. Furthermore, in this analysis, we do not alter assumptions about local or regional interconnection potential for distributed generation systems. Consistent with the AEO2022 Reference case, in the credit cases, we represent state-level interconnection policies’ effects on projected installations of solar photovoltaics deployed in the buildings sector.

Extended Credit case

This case assumes that existing tax credits for renewable energy and federal energy efficiency incentives, instead of maintaining currently scheduled reductions and sunset dates, are extended through 2050. Tax credits for wind and solar electric generation capacity remain at their 2022 values through 2050. Federal energy efficiency incentives are extended at their 2021 values through 2050.

Extending the duration of renewable tax credits both decreases prices in the electric power, buildings (residential and commercial), and industrial sectors and increases renewable generation capacity in the electric power and buildings sectors relative to the AEO2022 Reference case. Increasing adoption of distributed generation in the buildings and industrial sectors and prolonging the availability of energy efficiency incentives through 2050 reduces delivered energy consumption through 2050 by less than 1% from Reference case projections.

Sunset Credit case

This case assumes that existing tax credits and federal efficiency incentives expire completely by 2023, at the latest, before their currently scheduled phase outs and expirations as represented in the Reference case.

The Sunset Credit case has a smaller effect on both utility-scale solar and wind capacity and distributed generation adoption than the Extended Credit case. Although electricity prices in the Sunset Credit case are slightly higher throughout the projection period because most of the energy efficiency incentives expire at the same time or only slightly earlier than in the AEO2022 Reference case, long-term delivered energy consumption in the residential, commercial, and industrial sectors remains about the same.

Tax Credits and Incentives in Power Generation and Energy Demand Markets

The AEO2022 Reference case assumes that existing laws and regulations remain as enacted throughout the projection period, including when the laws or policies are scheduled to sunset. The alternative cases in this article assume changes to laws and regulations that have historically been extended beyond their legislated sunset dates or that have required periodic updates beyond current standard levels. In particular, these cases analyze potential effects on energy consumption and energy-related emissions by varying policies affecting renewable electric generation and end-use energy consumption and efficiency.

In the Extended Credit case, we assume the permanent extension, through 2050, of federal production tax credits (PTC) and investment tax credits (ITC) for renewable generation technologies, renewable end-use technologies, and combined-heat-and-power (CHP) technologies in the electric power, buildings, and industrial sectors. In addition, we assume a permanent extension of federal end-use energy efficiency rebates and tax credits, including energy efficiency tax credits for newly constructed homes. We do not assume that tax credits for electric vehicles or Corporate Automobile Fuel Economy (CAFE) standards are extended or updated. Table 1 describes specific renewable energy and energy efficiency policies represented in these cases.

In the Sunset Credit case, we assume the permanent repeal, starting in 2023, of federal tax credits for renewable generation technologies in the electric power, buildings, and industrial sectors and the permanent repeal of federal end-use efficiency rebates and tax credits. These repeals include tax credits and incentives that are represented in our AEO2022 Reference case as permanently available through the end of the 2050 projection period.

Federal energy efficiency incentives, including rebates for energy-consuming equipment and housing shell subsidies, ended in 2021, consistent with current laws and regulations (as reflected in the AEO2022 Reference case). The residential energy efficient property tax credit is the exception; it ends two years earlier than in the Reference case. The final year of availability of energy efficiency tax credits is itemized in Table 2.

Table 1. Federal tax credits for renewable energy generation and energy efficiency, Reference case and credit cases

| Federal policy | Policy description |

|---|---|

| Production tax credit (PTC) 26 U.S. Code § 45 | Per-kilowatthour tax credit for electricity generated by qualifying renewable energy sources. The tax credit remains in effect for 10 years after the facility is placed in service. |

| Investment tax credit (ITC) 26 U.S. Code § 48 | Tax credit offsetting investments in distributed generation technology investments, including solar photovoltaic, small wind, and geothermal heat pump technologies in the residential and commercial buildings sectors. |

| Nonbusiness energy property tax credit 26 U.S. Code § 25C | Tax credit offsetting the cost of replacing existing end-use equipment with more efficient alternatives. |

| Residential energy efficient property tax credit 26 U.S. Code § 25D | Tax credit offsetting a share of labor and installation costs for technologies that generate renewable energy. Installations in newly constructed and existing homes are eligible for the credit. |

| New energy efficient home credit 26 U.S. Code § 45L | Tax credit for newly constructed homes that save 50% more heating and cooling energy relative to the 2006 International Energy Conservation Code. |

| Data source: U.S. Energy Information Administration, Summary of Legislation and Regulations Included in the Annual Energy Outlook 2022 | |

Key findings

Extending the duration of renewable tax credits, as assumed in the Extended Credit case, increases renewable generation capacity in the electric power, buildings, and industrial sectors relative to the AEO2022 Reference case. Increasing adoption of distributed generation in the buildings and industrial sectors and prolonging the availability of energy efficiency incentives through 2050 reduces delivered energy consumption through 2050.

The Sunset Credit case shows a less notable effect on both utility-scale solar and wind capacity and adoption of distributed generation than the Extended Credit case. Although electricity prices in the Sunset Credit case are slightly higher throughout the projection period than in the Reference case, and because most of the energy efficiency incentives expire at the same time or only slightly earlier than the AEO2022 Reference case, the effect on long-term delivered energy consumption in the residential, commercial, and industrial sectors is negligible.

Methodology

The AEO2022 Reference case generally assumes existing laws and regulations, and it serves as a starting point for analysis of possible changes in legislation or regulations. Current laws and regulations in the Reference case include any sunset dates or any specific changes over time as defined in the law or regulation. To develop these cases, we modified the timespan for available incentives for electricity generating technologies in the electric power and end-use sectors. We also modified the timespan for available new housing construction incentives and for federal end-use equipment replacement subsidies. Changes in the availability of incentives directly affect modeled distributed generation and combined-heat-and-power (CHP) costs and end-use equipment and new housing shell costs, which in turn affect the projected:1

- Electricity Market Module generation mix and end-use electricity prices

- Commercial Demand Module (CDM) and Residential Demand Module (RDM) distributed generation installed costs and investment decisions

- Industrial Demand Module and CDM CHP installed costs and investment decisions

- RDM building shell efficiencies for new construction and end-use equipment purchasing decisions

The alternative cases in this article assume changes to laws and regulations that have historically been extended beyond their legislated sunset dates. We present distinct cases to compare them with Reference case projections.

- Extended Credit case. Extends production tax credit (PTC) or investment tax credit (ITC) at 2022 levels from 2023 through 2050. Maintains federal efficiency incentives and residential building shell subsidies at 2021 levels from 2022 through 2050.

- Sunset Credit case. Ends PTC and ITC after 2022, ends federal efficiency incentives in 2021 or 2022, and ends residential building shell subsidies after 2021.

Most federal energy efficiency policies expire early in the projection period in the Reference case, so varying the federal energy efficiency policy assumptions in the Sunset Credit case only affects the first few years of the projection period. In contrast, varying the federal energy efficiency policy assumptions in the Extended Credit case creates a larger change relative to Reference case assumptions (Table 2). These factors contribute to the credit cases’ differences in delivered energy consumption, fuel use, and emissions.

Table 2. Federal energy efficiency tax credits and final year of availability, Reference case and credit cases (2021–2050)

| Federal energy efficiency policy | Reference case final year of availability | Sunset Credit case final year of availability | Extended Credit case final year of availability |

|---|---|---|---|

| Nonbusiness energy property tax credit 26 U.S. Code § 25C |

2021 | 2021 | 2050 |

| Residential energy efficient property tax credit 26 U.S. Code § 25D |

2024 | 2022 | 2050 |

| New energy efficient home credit 26 U.S. Code § 45L |

2021 | 2021 | 2050 |

| Data source: U.S. Energy Information Administration, Annual Energy Outlook 2022, Reference case and credit cases | |||

In the AEO2022 Reference case, solar projects in the electric power sector receive a tax credit at 30% through 2023, 26% for projects entering service after December 31, 2023, and a permanent 10% tax credit for projects entering service in 2026 and beyond. For commercial and residential sectors, the ITC for solar projects continues to decline from 26% in 2022 to 22% in 2023. For installations in 2024 and beyond, the credit decreases permanently to 10% for the commercial sector and phases out completely for the residential sector. The PTC continues for select technologies in the electric power sector, including wind, at 60% until 2025, and it remains in effect for 10 years after the project’s in-service date.

Extended Credit case assumptions

This case assumes that existing tax credits with scheduled reductions and sunset dates remain at their 2022 values through 2050. Federal energy efficiency incentives are extended at their 2021 values through 2050. In particular, the Extended Credit case adopts the following assumptions:

- The PTC continues to be available at 60% of the full value for utility-scale wind facilities through 2050 instead of phasing out for projects coming online after December 31, 2025, as assumed in the Reference case. Other PTC-eligible technologies, including closed-loop biomass, landfill gas, and incremental hydroelectric, continue to receive the full value of the PTC through 2050.

- Standalone solar photovoltaic (PV) systems in the electric power sector receive the full 30% ITC through 2050. In addition, the Extended Credit case assumes battery storage in solar PV hybrid systems recharges exclusively from the co-located solar facility, making it eligible for the ITC.

- Wind projects that are eligible to claim the ITC in lieu of the PTC will opt for the 30% ITC through 2050 as a result of high capital costs.

- The ITC 2022 value of 26% remains in effect through 2050 for residential and commercial sector solar PV systems. For CHP systems and ground-source heat pumps, the ITC value of 10% remains in effect through 2050 across the buildings and industrial sectors.

- Federal subsidies for residential energy efficient building shell construction and the purchase of energy efficient end-use equipment (such as water heaters, heat pumps, furnaces, and air conditioners) that are available through 2021 in the Reference case are extended at 2021 levels through 2050.

- Federal minimum efficiency standards for residential and commercial major end-use equipment are aligned with current provisions in the Reference case. No new energy efficiency standards are modeled, and no existing standards are expanded.

- Emissions attributed to the end-use sectors include CO2 emissions associated with the generation, transmission, and distribution of electricity that is ultimately consumed in industrial facilities or buildings.

Sunset Credit case assumptions

This case assumes existing tax credits and incentives expire completely by 2023, at the latest, before their currently scheduled phase-outs and expirations in the Reference case. Specifically, the Sunset Credit case includes the following assumptions:

- All renewable generation tax credits expire by 2023, including a complete sunset of the ITC for solar PV in the residential, commercial, and electric power sectors and for all other ITC-eligible technologies in the electric power sector. The PTC for all PTC-eligible technologies also expire by 2023.

- The available ITC for solar water heaters in both the residential and commercial sectors sunsets by 2023.

- Existing federal energy efficiency tax credits and subsidies expire in 2021, consistent with the Reference case, except for the residential energy efficient property tax credit (26 U.S. Code § 25D), which expires in 2022, two years earlier than in the Reference case.

- Emissions attributed to the end-use sectors include CO2 emissions associated with the generation, transmission, and distribution of electricity that is ultimately consumed in industrial facilities or buildings.

Results

Electricity generation, fuel mix, and emissions in the electric power sector

Electricity generation

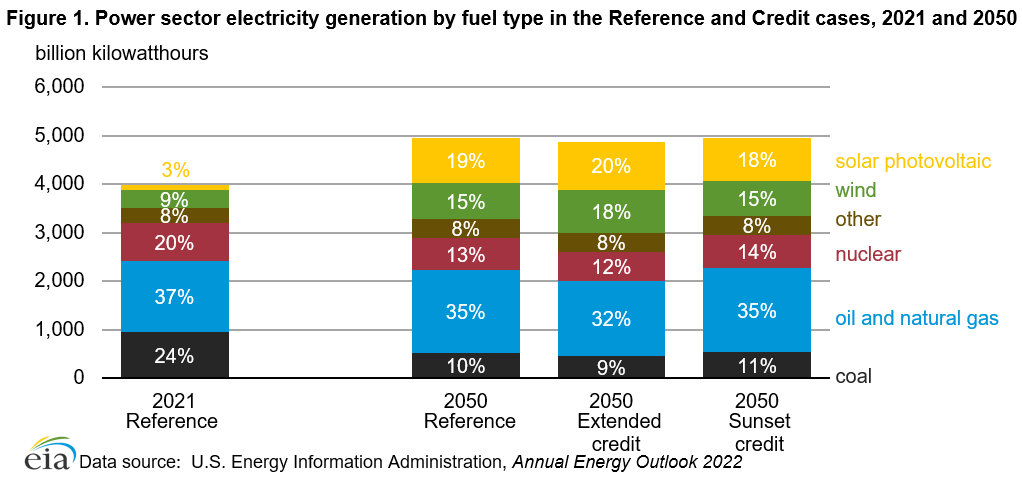

Although altering the assumptions in these cases results in little impact on overall electricity demand, the electricity generation mix does change over time. The share of generation for each fuel type in 2050 (Figure 1) varies across the different cases: 9%–11% for coal, 12%–14% for nuclear, 32%–35% for oil and natural gas 2, and 33%–38% for wind and solar photovoltaic. Although we observe a trade-off between electricity generation from oil and natural gas and from renewables across all cases, it is most evident in the Extended Credit case. In that case, the share of electricity generation from oil and natural gas decreases to 32% by 2050 compared with 35% in the Reference case, although the share of electricity generation from wind and solar increases from 34% in the Reference case to 38% as additional renewable capacity is installed through 2050 (Figure 1).

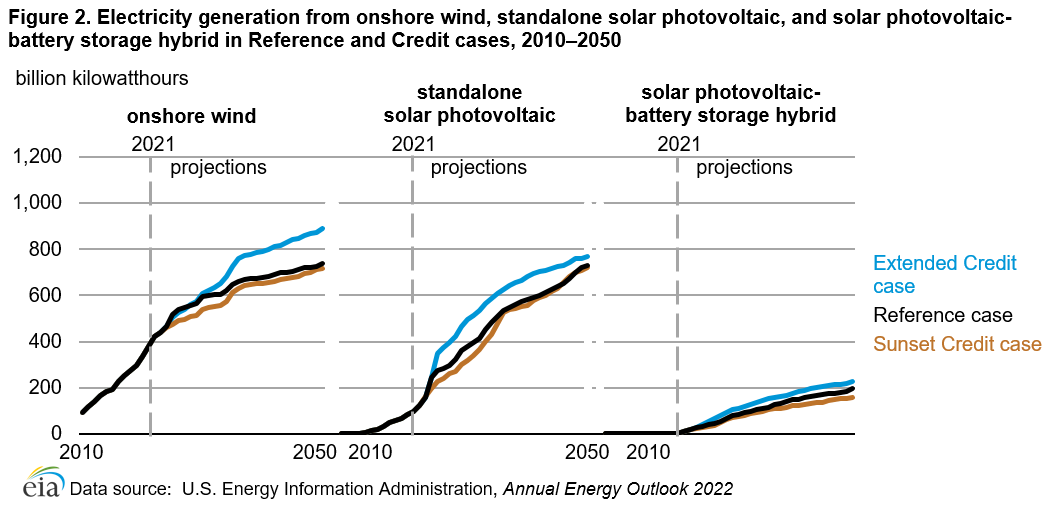

In the Extended Credit case, we project more electricity generation from wind resources than in the Reference case (Figure 2). In 2050, electricity generation from wind accounts for 18% (889 billion kilowatthours [BkWh]) of total electricity generation, compared with 15% (736 BkWh) in the Reference case. Electricity generation from both standalone solar PV and solar PV-battery storage hybrids is higher in the Reference case, although slightly smaller than the increase in wind generation between the two cases. Standalone solar PV generation shows a larger response in the near- to mid-term because of more capacity additions in response to the ITC extension, while solar PV-battery storage generation increases at a more moderate pace through the projection period. Although the extension of these credits through the projection period significantly increases mid- and long-term market adoption of wind and solar technologies, effects on other eligible renewable generation technologies, including hydropower, biomass, and geothermal, are minimal in comparison as a result of their higher installed costs.

Expiration of the PTC and the ITC in 2023 in the Sunset Credit case has a small effect on both utility-scale solar PV and wind projects compared with the Reference case because the current credit levels are not sufficient to significantly affect investment decisions, as the installed costs for both technologies are expected to continue to decline. In 2050, compared with the Reference case, this case expects 1% less electricity generation from both standalone solar PV and solar PV-battery hybrid, 8 BkWh, and wind is 19 BkWh (3%) less. Without the permanent 10% ITC, as assumed in the Reference case, fewer utility-scale solar PVs are built. Both wind and solar PV are added more gradually over time at only slightly lower levels than in the Reference case, as we assume that wind and solar PV continue to be cost competitive with other sources in later projection years, even with the expiration of their respective tax credits.

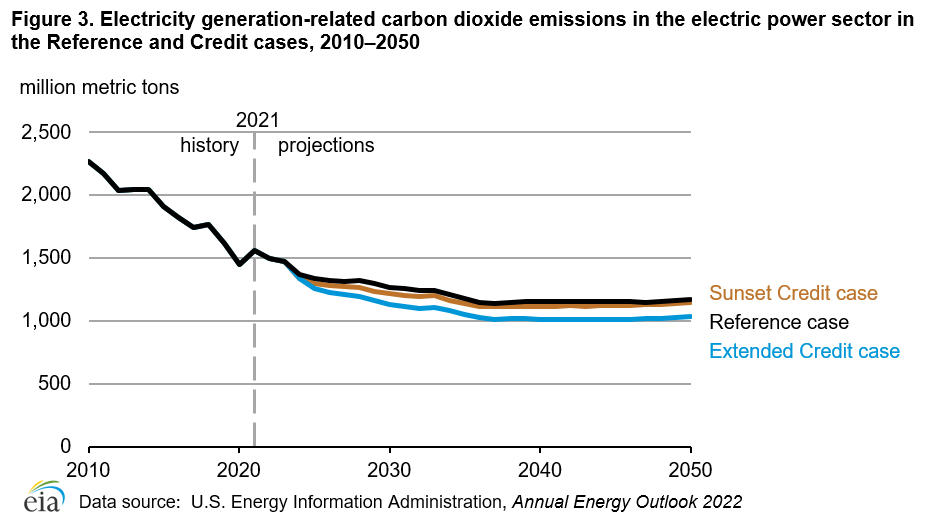

Electricity-related CO2 emissions decline in all cases in the near term as a cumulative effect of increased coal plant retirements, more natural gas-fired generation and renewable generation, and stable electricity demand. Increased penetration of end-use solar PV in the Extended Credit case further reduces overall demand for purchased electricity, resulting in less electricity-related CO2 emissions than in the other cases (Figure 4). In the Reference case, electricity-related CO2 emissions decrease from 1,560 million metric tons (MMmt) in 2021 to 1,145 MMmt (27%) in 2050. Electricity-related CO2 emissions in 2050 are a further 111 MMmt (10%) lower in the Extended Credit case compared with the Reference case. CO2 emissions in the Sunset Credit case are generally slightly higher than the Extended Credit case for most of the projection years because less renewables capacity is available for electricity generation. In 2050, electricity-related emissions in the Sunset Credit case are 23 MMmt (2%) higher than in the Reference case.

Electricity prices, tax credit payments, and other market impacts

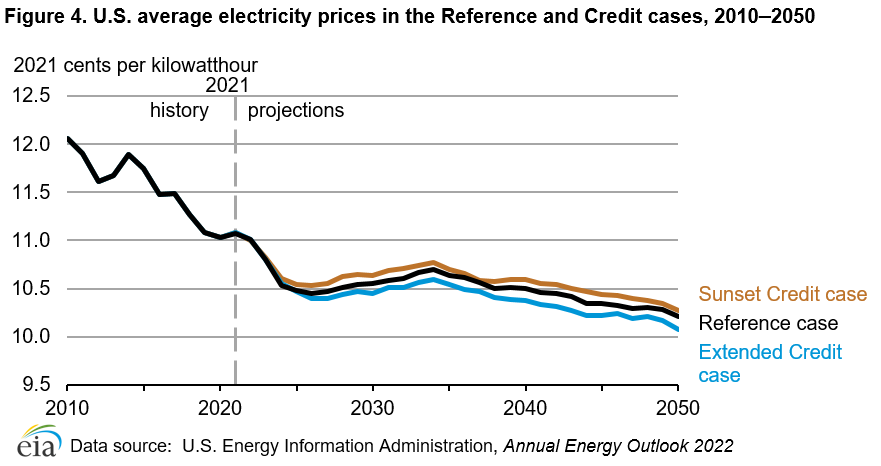

All-sector average electricity prices between the Reference, Extended Credit, and Sunset Credit cases remain within a 5% range throughout the projection period, with the spread in 2050 at 2%. Average prices range from 10.1 to 10.3 (2021 cents per kilowatthour) in 2050 (Figure 3). In the Extended Credit case, electricity prices are slightly lower than in the Reference case throughout the projection period. In response to the certainty of continued tax credits, significantly more renewable capacity—particularly wind and utility-scale solar—is added than in the Reference case, resulting in less electricity generation required from higher-cost sources such as natural gas. Electricity prices in the Sunset Credit case are slightly higher throughout the projection period than in the Reference case because more generation from higher-cost fuels such as natural gas compensates for less wind and solar generation.

In all cases, we project U.S. average electricity prices to decline in the near term before rising in the mid-term, in line with natural gas consumption and prices, partially offset by rising transmission and distribution costs as a result of new renewable capacity in the system. The average electricity price across all sectors begins to decline after 2034 as the generation cost component—which represents the largest share of the price of electricity—decreases, partially because of increased generation from renewables.

Table 3. Average annual expenditures for buildings consumer indicators, Reference case and credit cases (2021–2050)

| Average annual expenditure (billion 2021 dollars per year) | Reference | Extended Credit | Sunset Credit |

|---|---|---|---|

| Buildings consumer capital costs for solar equipment | $10.07 | $12.18 | $9.66 |

| Percentage change from Reference case | – | 21.00% | -4.00% |

| Government tax expenditures for buildings solar equipment | $0.65 | $3.17 | $0.23 |

| Percentage change from Reference case | – | 387.70% | -64.60% |

| Buildings electricity purchases | $359.56 | $354.37 | $361.94 |

| Percentage change from Reference case | – | -1.40% | 0.70% |

| Data source: U.S. Energy Information Administration, Annual Energy Outlook 2022, Reference case and credit cases Note: Percentages calculated based on rounded figures. |

|||

Residential and commercial consumers incur higher equipment costs in the Extended Credit case, but these higher costs are offset by savings on grid electricity purchases because of increases in distributed generation. Compared with the Reference case, consumers in the residential and commercial sectors save an average of $5.2 billion (2021 dollars) in annual electricity costs from 2021 to 2050 in the Extended Credit case. Tax credits are available to any consumer who purchases eligible equipment, regardless of whether they may have purchased the equipment without an incentive. The Extended Credit case also reflects increased tax expenditures that reduce net tax revenue for the U.S. government (Table 3).

In the Sunset Credit case, residential and commercial consumers save an average of $0.4 billion per year (2021 dollars) on solar equipment from 2021 to 2050 than in the Reference case, and the government’s tax expenditures decrease by $0.4 billion per year (Table 3). Total electricity purchases in buildings increase by $2.4 billion per year in the Sunset Credit case relative to the Reference case.

Table 4. Average annual government tax expenditures for selected technologies, 2023–2050

| Technology | Reference | Extended Credit | Sunset Credit |

|---|---|---|---|

| Onshore wind, hydro, geothermal, wood biomass | $2.00 | $4.00 | $1.40 |

| Solar PV and offshore wind | $2.70 | $5.00 | $0.00 |

| Total | $4.70 | $9.00 | $1.40 |

| Data source: U.S. Energy Information Administration, Annual Energy Outlook 2022, Reference case and credit cases Note: PV = photovoltaic |

|||

In the electric power sector, the extension of the PTC in the Extended Credit case increases government tax expenditures between 2023 and 2050 by an additional $2.0 billion per year relative to an average of $2.0 billion per year in the Reference case (Table 4). This difference is largely due to increased tax expenditures for onshore wind technologies in the Extended Credit case. Similarly, for utility-scale PV and offshore wind, the extension of the ITC increases government tax expenditures in the electric power sector by an additional $2.3 billion per year from 2023 to 2050 in the Extended Credit case relative to an average of $2.7 billion per year in the Reference case. By contrast, government tax expenditures decrease in the Sunset Credit case once the PTC and ITC expire in 2023. Compared with the Reference case, tax expenditures for the PTC decrease by an average of $0.6 billion per year, and tax expenditures for the ITC decrease by an average of $2.7 billion per year in the Sunset Credit case.

Commercial, residential, and industrial energy consumption

Extending federal tax credits and incentives, as in the Extended Credit case, has a larger impact on commercial, residential, and industrial delivered energy consumption than ending the tax credits early, as in the Sunset Credit case. Ending the ITC and federal energy efficiency subsidies earlier than in the Reference case has a minimal impact on long-term delivered energy consumption or electricity generated from on-site technologies in the buildings and industrial sectors.

Energy consumption in the buildings and industrial sectors

Delivered energy consumption across the residential, commercial, and industrial sectors in 2050 is 0.5% higher in the Reference case than in the Extended Credit case, but 0.1% lower in the Sunset Credit case.

The differences between the projections for the different cases result from:

- Different end-use fuel prices

- Differences in federal efficiency incentives

- The duration and availability (or lack thereof) of tax credits for distributed generation equipment and technologies such as solar water heaters

In the Extended Credit case, despite lower natural gas and electricity prices, we project less delivered energy consumption than in the Reference case. Increased distributed generation reduces the amount of electricity that must be purchased from the grid to meet industrial and buildings energy demand, while more efficient end-use equipment reduces the overall energy that buildings use.

In the Sunset Credit case, we project higher natural gas and electricity prices among each of these end-use sectors relative to the Reference case. Despite higher prices, delivered energy consumption in the Reference case and the Sunset Credit case are virtually identical throughout the projection period. In the residential and industrial sectors, on-site electricity generation capacity is nearly identical to the Reference case through 2050. Sunsetting the ITC earlier has a larger impact on the commercial sector, where CHP and distributed generation capacity in 2050 is reduced by 11% relative to the Reference case. Because of the commercial sector’s sensitivity to the availability of the ITC, we project slightly higher electricity purchases through 2050 in the Sunset Credit case.

The difference in cumulative delivered energy consumption from 2021 to 2050 is 4.7 quadrillion British thermal units (quads) between the Extended Credit case and the Sunset Credit case. The difference between the cumulative energy consumed in the Reference case and the Extended Credit case over the same time period is 4.0 quads. To put this energy savings into perspective, we project 4.5 quads of electricity will be used to power televisions and related equipment across all U.S. homes from 2021 to 2050 in our Reference case.

Distributed generation for on-site use in buildings and the industrial sectors

In the buildings and industrial sectors, changes in distributed generation capacity and generation are the most significant contributors to the differences in delivered energy between the Reference case and the credit cases. Across all cases, solar photovoltaic (PV) systems account for the largest share of net electricity generation from distributed sources in the buildings sectors, and natural gas-fired CHP systems account for the largest share of net electricity generation from distributed sources in the industrial sector.

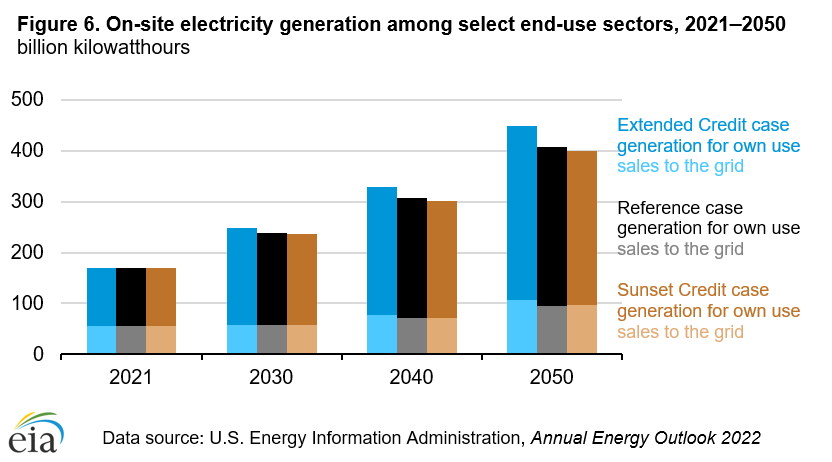

In these sectors, we project that the consumer cost savings related to the ITC increase the adoption rate of distributed generation technologies over time (Figure 6). The increase in own-use generation directly reduces how much electricity these end-use consumers purchase from the grid. Varying the ITC indirectly affects the amount of electricity that end-use sectors sell back to the grid as well, because higher overall PV and CHP capacity allows increased generation relative to the Reference case, and a portion of that additional generation is sold back to electric utilities.

Extending the ITC at 2022 levels through 2050 increases industrial CHP investment and results in 2% higher projected CHP generation in the industrial sector in 2050, compared with the Reference case. In the case of natural gas-fired CHP technologies, the industrial sector adds 8.0 gigawatts of alternating current (GWac) generating capacity from 2021 to 2050 in the Extended Credit case, compared with 7.0 GWac of additional capacity added in the Reference case.

This increased generation results in higher overall natural gas consumption as a fuel. In 2050, natural gas CHP use is 0.6% higher in the Extended Credit case than in the Reference case.

Given the relatively minor change from the ITC credit expiration date in the Sunset Credit case, both the projected industrial CHP generation and associated natural gas fuel consumption change very little compared with the Reference case.

Extending the ITC leads to more penetration of solar PV in residential and commercial buildings, despite lower projected electricity prices relative to the Reference case for both commercial and residential customers. Cumulatively, from 2021 to 2050, the Extended Credit case has an additional 605 BkWh of solar generation relative to the Reference case.

In the Extended Credit case, as a result of longer-lasting incentives for solar PV equipment, solar PV capacity expands by 32 GW direct current relative to the Reference case in 2050 (Figure 7). Solar PV generation in the buildings sector increases to nearly six times 2021 levels by 2050. Buildings directly consume 80% of this electricity generation to fulfill demand for space cooling, ventilation, refrigeration, and other end-uses. This reduces the amount of electricity that buildings must purchase from the grid to meet demand for energy-consuming services through 2050.

Equipment and building shell efficiencies in the buildings sector

Changing incentive end dates affects energy consumption in buildings in distinct ways. Although federal minimum energy efficiency standards for end-use equipment in buildings remain consistent with the Reference case across all cases, federal energy efficiency incentives in buildings are extended through 2050 in the Extended Credit case (Table 2). In the Sunset Credit case, efficiency incentives are ended at the legislated sunset date, with the exception of the Residential energy efficient property tax credit (26 U.S. Code § 25D). In the Reference case, this policy is in place until 2024, but in the Sunset Credit case, it ends after 2022.

In the Extended Credit case, the growth of delivered energy consumption in the buildings sector slows partly because of the extension of federal tax incentives for replacing end-use equipment with more efficient models or technologies (Figure 8). Extending energy efficiency incentives generally leads to higher overall stock efficiency of space heaters, air conditioners, and water heaters relative to the Reference case, which, in turn, reduces projected demand for electricity and natural gas in buildings. In 2050, natural gas purchases in buildings are 0.6% lower in the Extended Credit case than in the Reference case. Among buildings sector delivered energy sources, electricity is most affected by changes to incentive end dates. In 2050, electricity purchases are 1.7% lower relative to the Reference case.

Extending federal incentives also changes the mix of equipment that we project will be in use through 2050. Extending the existing federal subsidies for residential solar thermal water heaters, for example, expands the stock of this equipment by over 200% relative to the Reference case by 2050. This equipment displaces some existing electric resistance and natural gas-fired water heaters, which, nonetheless, remain the most common water heating technologies by a wide margin among U.S. homes in all cases.

The New Energy Efficient Home credit (26 U.S. Code § 45L) is available to home builders through 2021 and is reflected in our AEO2022 Reference case. This federal subsidy applies to new energy efficient homes that achieve 50% energy savings for heating and cooling relative to the 2006 International Energy Conservation Code (IECC). Extending this subsidy through 2050 in the Extended Credit case has two main effects. Relative to the Reference case, the Extended Credit case exhibits:

- An increase in the number of new homes built to exceed the IECC standard after 2021

- Less energy consumption associated with residential space heating and cooling as a result of improved building envelope performance

As new homes are constructed, trends in fuel prices affect equipment choice. Higher prices drive market uptake of more efficient building shells to reduce space heating and cooling loads.

End-use sector energy-related emissions

The credit cases affect the amount of distributed generation and CHP net generation relative to the Reference case. In turn, differences in the electricity generation fuel mix affect the CO2 emissions associated with energy use in the industrial and buildings sectors (Figure 9). Across all cases, CO2 emissions attributed to the end-use sectors include emissions associated with the generation, transmission, and distribution of electricity that is ultimately consumed in industrial facilities or buildings.

From 2021 to 2050, the cumulative difference in industrial and buildings energy-related emissions, including emissions associated with the consumption of electricity, is 3.5 billion metric tons of CO2 higher in the Sunset Credit case than in the Extended Credit case. Compared with the Reference case, in the Extended Credit case, energy-related emissions are 4% lower in 2050, and Sunset Credit case emissions are 1% higher.

Buildings energy expenditures

The reductions in delivered energy consumption in the Extended Credit case are accompanied by higher end-use equipment costs for consumers. In comparison with the AEO2022 Reference case, residential and commercial consumers in the Extended Credit case pay an extra $2.2 billion per year (2021 dollars), on average, from 2021 to 2050 for end-use equipment and residential building shell improvements.

The additional investments by consumers in the Extended Credit case are more than offset, however, by savings on energy purchases as a result of efficiency improvements. Compared with the Reference case, consumers in the residential and commercial sectors increasingly save money on nonrenewable energy expenditures each year—up to $11.7 billion savings in 2050 alone, with an average annual savings of $6.2 billion in annual nonrenewable energy expenditures from 2021 to 2050 in the Extended Credit case.

Average annual consumer investments in the Sunset case are much closer to Reference case projections. Residential and commercial consumers pay close to the Reference case average from 2021 to 2050 for end-use equipment and residential building shell improvements in the Sunset Credit case. However, annual energy expenditures are higher for residential and commercial consumers in this case, averaging $2.7 billion per year more than in the Reference case.

Conclusion

The results of the Extended Credit and Sunset Credit cases demonstrate that changing the duration of renewable tax credits affects the evolution of the generation resource mix over time more than it affects overall electricity demand. In particular, extending the credits results in higher penetrations of both standalone and hybrid solar photovoltaic generation, and much higher penetration of onshore wind-powered generation. Likewise, the Sunset Credit case results in lower penetrations of those three technology types, although they all trend closer to the Reference case than to the Extended Credit case results.

Changes in buildings- and industrial-sector distributed generation and CHP technology tax credits and federal efficiency incentives affect energy consumption and equipment stocks. Specifically, ending tax credits and energy efficiency incentives slightly earlier than or in tandem with the Reference case has a limited effect on projected delivered energy consumption by 2050. Extending tax credits and energy efficiency incentives through 2050 reduces delivered energy consumption and increases adoption of these technologies across U.S. buildings and the industrial sectors relative to our AEO2022 Reference case.