By Wolf Richter for WOLF STREET.

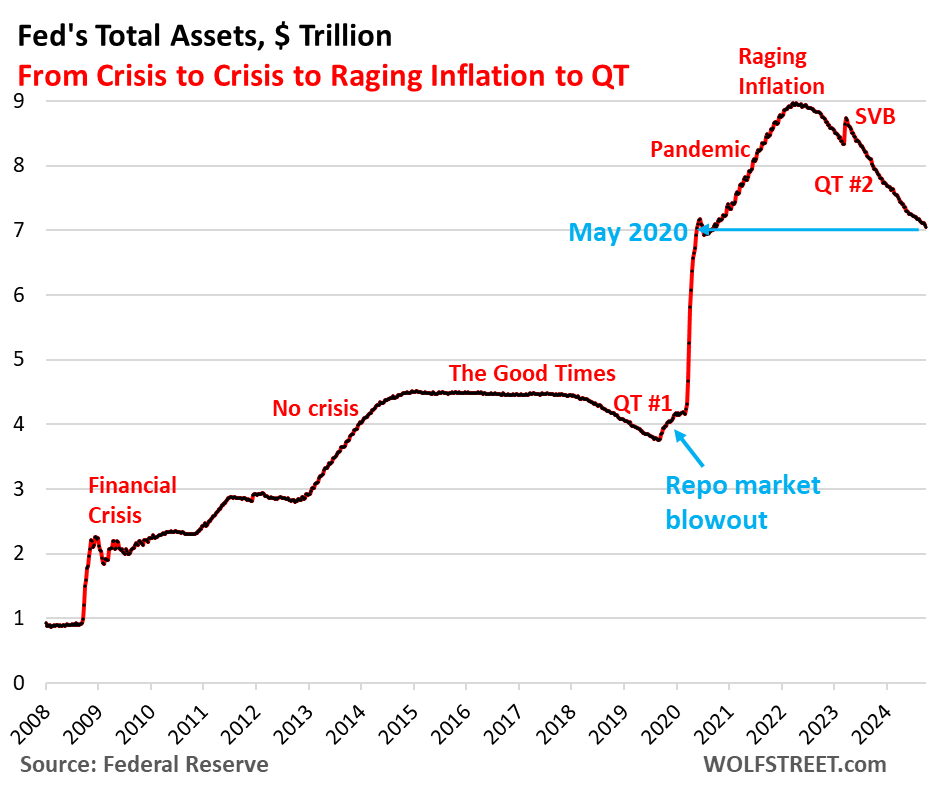

Total assets on the Fed’s balance sheet dropped by $66 billion in September, to $7.05 trillion, according to the Fed’s weekly balance sheet today. The balance sheet first reached this level on May 20, 2020, towards the end of the three-month mega-QE (blue arrow in the chart).

Since the end of QE in April 2022, the Fed has shed $1.92 trillion, or 40% of the assets that it had added during pandemic QE.

QT assets by category.

Treasury securities: -$24 billion in September, -$1.41 trillion from peak in June 2022, to $4.36 trillion, the lowest since August 2020.

The Fed has now shed 43% of the $3.27 trillion in Treasury securities that it had added during pandemic QE.

Treasury notes (2- to 10-year) and Treasury bonds (20- & 30-year) “roll off” the balance sheet mid-month and at the end of the month when they mature and the Fed gets paid face value. The roll-off is now capped at $25 billion per month. About that much rolled off in September, minus a small amount of inflation protection the Fed earns on its Treasury Inflation Protected Securities (TIPS) that was added to the principal of the TIPS.

Mortgage-Backed Securities (MBS): -$18 billion in September, -$458 billion from the peak, to $2.28 trillion, the lowest since June 2021. The Fed has shed 33% of the MBS it had added during pandemic QE.

MBS come off the balance sheet primarily via pass-through principal payments that holders receive when mortgages are paid off (mortgaged homes are sold, mortgages are refinanced) and when mortgage payments are made. But sales of existing homes have plunged, as had mortgage refinancing, though over the past two months, refinancing has risen sharply but is still low. So fewer mortgages got paid off, and passthrough principal payments to MBS holders, such as the Fed, have been reduced to a trickle. As a result, MBS have come off the balance sheet at a pace that has been below $20 billion in most months.

Bank liquidity facilities.

Only two bank liquidity facilities currently show a balance: The Discount Window and the Bank Term Funding Program (BTFP). The other bank liquidity facilities — Central Bank Liquidity Swaps, Repos, and Loans to the FDIC — are either at zero or near zero.

Discount Window: roughly unchanged in September, at $1.6 billion. During the bank panic in March 2023, loans had spiked to $153 billion.

The Discount Window is the Fed’s classic liquidity supply to banks. Since the rate cut in September, the Fed charges banks 5.0% in interest on these loans and demands collateral at market value, which is expensive money for banks. In addition to the cost, there’s a stigma attached to borrowing at the Discount Window. So banks don’t use this facility unless they need to.

The Fed has been exhorting banks to make more regular use of the Discount Window, or at least figure out how to use it (apparently SVB hadn’t), practice using it with small-value exercise transactions, and pre-position collateral so that they can use it when they need to.

Bank Term Funding Program (BTFP): -$27 billion in September, to $71 billion, the lowest since March 2023.

The BTFP had a fatal flaw when it was cobbled together over a panicky weekend in March 2023 after SVB had failed: Its rate was based on a market rate. When Rate-Cut Mania kicked off in November 2023, market rates plunged even as the Fed held its policy rates steady, including the 5.4% it paid banks on reserves. Some banks then used the BTFP for arbitrage profits, borrowing at the BTFP at a lower market rate and leaving the cash in their reserve account at the Fed to earn 5.4%. This arbitrage caused the BTFP balances to spike to $168 billion.

The Fed shut down the arbitrage in January by changing the rate. It also decided to let the BTFP expire on March 11, 2024. Loans that were taken out before that date can still be carried for a year from when they were taken out, and that’s what we’re seeing here.

No later than March 11, 2025, the BTFP will be zero, removing another $71 billion by then from the Fed’s balance sheet.

Balance Sheet below $7.0 Trillion…

The level of the balance sheet, today at $7.047 trillion, will fall below $7.0 trillion when another $48 billion in assets come off.

Currently, Treasury securities roll off at a rate of about $24 billion a month, and MBS at a rate of about $18 billion a month, so about $42 billion combined. In addition, there is the BTFP, whose decline is unpredictable, but can be substantial, as we say today. In addition, there are other smaller balance sheet items that can go into different directions, and if they add up to anything more than just a few billion we discuss them here.

At the current rate of decline, with no other issues interfering, the balance sheet is likely to get very close to, or drop below $7.0 trillion with the Treasury roll-off on October 31 (to show on the November 7 balance sheet); and if it misses in October, it will drop below $7.0 trillion in November, and that would be another round-number milestone for QT, from $8.97 trillion at the peak in April 2022.

We give you energy news and help invest in energy projects too, click here to learn more