ENB Pub note: Excellent article from White & Case about the Energy Transition. Looking at the money is like the old phrase “Follow The Money.”

For years, climate change campaigners and policymakers have argued that leading energy companies must play a key role in decarbonisation if the world is to move towards net zero. Now, research suggests the industry is prepared to rise to the challenge.

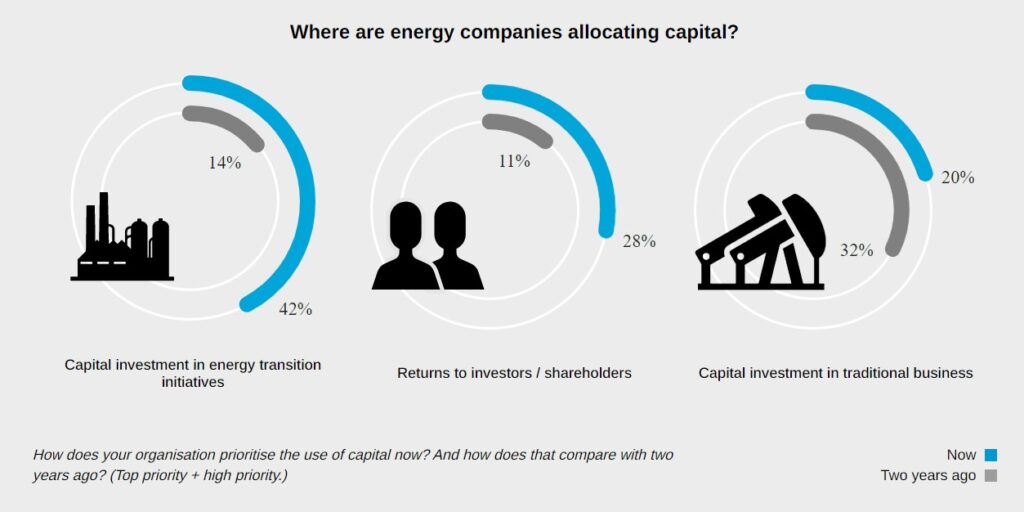

The proportion of energy companies that regard capital investment in energy transition as a top priority has tripled over the past two years, according to a study by law firm White & Case. Today, 42 per cent of energy businesses take this view, up from 14 per cent from 2021.

The shift reflects a growing realisation that simply investing more in greener energy while maintaining traditional production will not be enough to accelerate global decarbonisation at sufficient pace, argues Sandra Rafferty, a partner at White & Case. “Initially, when corporates, funds and banks considered energy transition, it was with a view to identifying and funding renewable energy sources such as wind and solar, as well as newer technologies,” she says. “The more forward-thinking players in the sector now recognise that full energy transition will also encompass taking fossil-based systems of energy production and consumption and decarbonising them.”

The scale of the challenge

Even with this shift, the figures remain daunting. The International Energy Association believes that, in order to reach net zero by 2050, clean energy investment worldwide will need to more than triple in this decade to US$4tn. Progress is being made – the first half of 2022 saw an 11 per cent increase, year-on-year, in investment in renewable energy, to US$226bn – but there is some way to go.

The good news is the energy sector expects to be able to tap into a range of funding sources to bridge the gap. For example, private equity investors are growing enthused by the opportunity, with 40 per cent of energy companies in White & Case’s research study expecting to access PE funding over the next 18 months. “The investment community has really made climate action the new business imperative,” says Annette Clayton, CEO of Schneider Electric North America. “It’s a business opportunity because less carbon is less cost; it’s a time for organisations to reimagine themselves, their solutions and their stakeholders.”

It’s not only cash that these investors provide. A growing number of deals in the sector have seen energy companies team up with financial sponsors that have expertise in major infrastructure projects. These joint venture partners bring funding, certainly, but also the experience of funding and managing large-scale projects. “Bringing capital into this sector is enormously important, but there is also a skill in being able to create assets,” says David Tilstone, a Managing Director at Macquarie Asset Management. “It requires expertise and experience to be able to go through that development period and to commercialise a project.”

Such initiatives are also enabling the sector to explore new business models, adds Clayton, who points to two Schneider Electric joint ventures to create energy-as-a-service solutions: AlphaStruxure with The Carlyle Group, and GreenStruxure with Huck Capital and ClearGen. “This is an absolutely new way of serving the market,” she says. “The energy-as-a-service business model eliminates all the upfront customer cost for the project, as well as giving them long-term cost predictability for energy supply and insulating the customer from rising energy costs.”

Investment appeal

For investors, the decarbonisation story looks increasingly attractive. In 2021, private equity investors allocated US$21.5bn to the US renewable energy sector; last year, a single infrastructure fund, Brookfield Asset Management, raised US$15bn for its Global Transition Fund.

Energy companies are not only looking outwards for funding, however; 32 per cent say they will turn to their existing balance sheets to finance energy transition initiatives, particularly following a period in which soaring energy prices have generated outsized revenues. Many also point to plans to raise new funding from the debt or equity markets.

It helps that the sector expects to be able to raise finance through a variety of different sources and mechanisms. Alongside sources such as project finance and acquisition funding, the rapid growth of the green bond market offers an increasingly rich vein for energy companies to tap into. Green bond issuance exceeded $500bn for the first time in 2021, when fundraising increased by 73 per cent compared with 2020. According to White & Case’s research, 35 per cent of capital finance providers said they intended to make use of corporate green bonds.

The evolution of such funding will reassure governments, which are under pressure to offer more support – directly or indirectly – to energy companies seeking to decarbonise. The implications for public finances, as well as the political debate, make this challenging.

Energy companies that do push for such support should expect it to come with strings attached, warns White & Case’s Sandra Rafferty. “Governments need to ensure that any such support is proportionate and does not result in super profits for the recipients, particularly at the expense of the consumer,” she says. “To ensure this, it is likely that there will be greater scrutiny and regulation in the energy sector, not dissimilar to what happened to the financial services sector following the global financial crisis.”