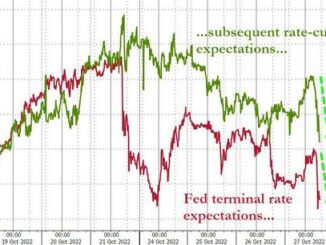

This morning’s melt-up in stocks appears to be more of the same panic-hedge unwind, vol-driven buying-panic as hopes/hints of a “pause” or “pivot” or “step-down” remain the over-arching narrative as rate-trajectory expectations drift dovishly (lower terminal rate and faster subsequent rate-cuts)…

As SpotGamma notes, its RiskReversal metric closed at -0.03 which is the highest (most bullish) in 2 years.

This is a signal that put values are low relative to calls – and this comes from call buying and/or put selling.

(We’ve been of the opinion that it has more to do with put selling in a high vol environment vs ferocious call demand).

The center of options activity is now forming in/around 3800 which likely makes this a key level into 11/2 FOMC.

As there are still a few sessions before FOMC, traders may see an opportunity to short ultra-short-term put options. We think that impulse likely fades into next Wednesday. Similarly we do not think traders will suddenly start adding long calls now, as they didn’t bother over the last few days. Therefore we favor rallies >3800 as unstable and prone to mean reversion.

Plotted below is the SPX term structure, and you can see how pre-FOMC IV is quite low compared to post-FOMC.

This is clearly where the big money is focused.

However, Nomura’s Charlie McElligott notes that the clearing of EPS event risk this week is allowing for a resumption of Vol-suppressing Corp-Buyback flows… but generally-speaking, with SPX/SPY and IWM sitting back above “Neutral Gamma” in LONG territory… those are acting far more stable… versus Nasdaq turmoil and still stuck “Short Gamma” location (spot $270 in QQQ vs “Gamma Flip” level up at $281)…

As seen in markets this morning…

…stocks continue to “Crash UP” versus just “grind down,” while also too AAPL does the work of Atlas and props almost single-handedly…

And as Spotgamma explains below, there’s a tactical floor appearing from the options market for META and AMZN…

Accordingly, McElligott reminds readers that the average SPX move on “up” days is over 2:1 that of the move magnitude on “down days” – which is part of the super-rare “Corr 1” on UPSIDE days (92% of SPX 500 stocks up on up days) vs typically being a “downside day” occurrence (now just 69% of SPX stocks down on down days) as traders grab into the Call Wing, far more worried about “Crash UP” (because they under-own / high Cash / low Nets) than “Crash DOWN”.

These past few days / weeks of “premature FCI easing” on this central bank “dovish step-down” thing that’s trending (more commentary below) has been such an irritation / frustration for Macro and L/S hedge funds on their (bearishly positioned) Equities exposure side…

But, away from the market’s moves, McElligott is stunned by the arrogance and hubris of the recent flurry of “almost coordinated” G10 central banks (RBA first in Sep, then the remarkable BoC and ECB meetings this week) who have communicated a *sudden* new “balance of risks”.

Central banks are making a big bet that inflation is being solved-for in “lagged and variable” fashion through the past year’s tightening efforts, in addition to the roll-over port backlogs and freight / shipping, inventory “bullwhip” disinflation, and simple “base effect”…trusting the market’s pricing of forward inflation

But the issue is that the reflexive nature of markets, where we “anticipate the anticipators” and take this “pause / mini-pivot / “step-down” information to then then “EASE” financial conditions on the forward projection versus prior expectations…which in-order to actual have the Fed’s desired effect on inflation need to be RESTRICTIVE / “TIGHT” (through impacting “demand” on cost of capital and destruction of wealth effect / animal spirits).

Accordingly, McElligott warns that markets may have “shot their shot” a few months too early.

So, as the Nomura strategist concludes, reiterating his recent thesis: perversely yet-again, the anticipation of what we all logically know has to eventually happen with the Fed’s hiking cycle – that you can’t hike rates at increasing magnitude forever…and that eventually, the hikes turn to a pause before finally, cuts to address the slowdown – becomes yet-another headwind for the Fed and other central banks who still have not yet slayed the inflation dragon…

And that “premature anticipation” of a tilt back towards EASING then acts to stimulate wealth effect and “animal spirits” which is not what The Fed wants to see (and does not fit with any of this morning’s inflation-related indicators – all of which signaled no let up at all in rising prices).

Crucially, the Nomura strategist warns that, I really think there is potential for another “rug pull” coming down the road, either from Fed acknowledging these realities again and as early as next week’s meeting – or worse, from inflation data remaining problematic and likely to stay “sticky higher,” closer to 4.0% than 2.0%, as we sit in 1Q23 with my previously described “now what?” moment.