A Los Angeles tower, FEMA headquarters in Washington, 100-year-old tower in Manhattan join list; some delinquent loans were “cured,” including by transfer to a custodial receiver and extend and pretend, and came off the list.

By Wolf Richter for WOLF STREET.

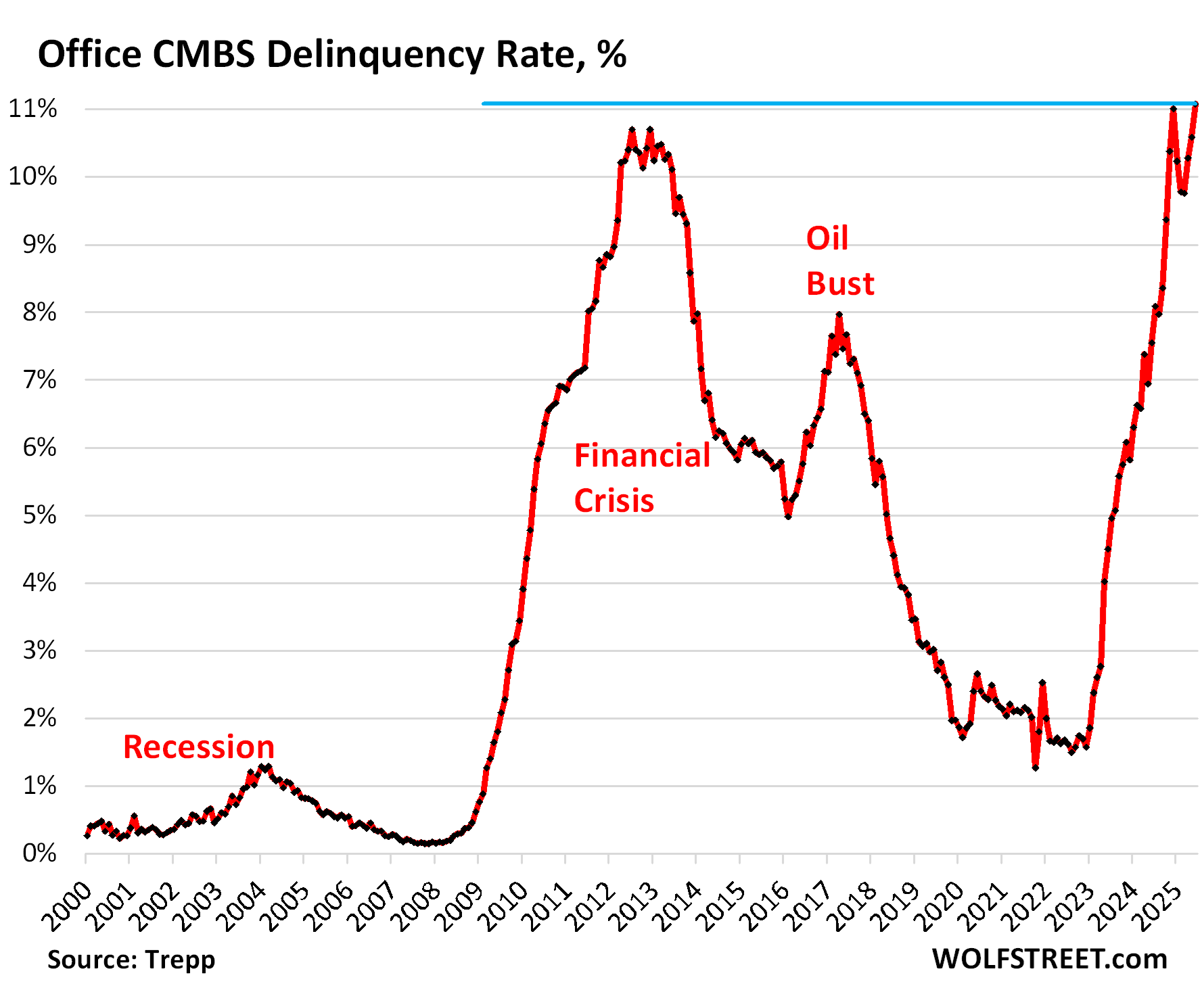

The delinquency rate of office mortgages that have been securitized into commercial mortgage-backed securities (CMBS) spiked to 11.1% in June, a new all-time high, re-blowing past even the Financial Crisis meltdown high, and squeaking past the December 2024 high, according to data by Trepp , which tracks and analyzes CMBS.

Since the beginning of 2023, the delinquency rate for office CMBS has exploded by 9.5 percentage points. And so the depression in the office sector of commercial real estate drags on, despite well over a year of pronouncements that “the worst is behind us.”

The last three months were a majestic relapse from February and March when the delinquency rate seemed to be on the mend.

A total of $156 billion of office loans have been securitized, Trepp said. The CMBS were sold to institutional investors, such as bond funds, insurers, etc. Banks are off the hook here.

In June, $1.8 billion of these CMBS office loans became newly delinquent, including the three discussed below, while $1 billion of delinquent office loans were “cured” and came off the list, including the three discussed below, one of which was “cured” when a court transferred the property into receiver, and another was “cured” by extend and pretend. It’s ugly out there.

The delinquent balance rose by $800 million – the difference between the newly delinquent loans ($1.8 billion) and the “cured” loans ($1 billion).

The top three June additions to the “delinquent” balance:

1 Cal Plaza, Los Angeles: $300 million, foreclosure. The 42-story 1-million square-foot 1980s office tower, formerly known as One California Plaza, was purchased in 2017 by a partnership between Rising Realty Partners and Colony Northstar.

The tower was financed with a 3.8% fixed-rate interest-only mortgage of $300 million that was then sliced into three pieces and securitized: An A-note of $86 million and a B-note of $164 million comprise the single-asset CMBS, CSMC 2017-CALI. The third piece, an A-note of $50 million, makes up 6.97% of the CMBS, CSAIL 2017-CX10, which is part of CMBX 11, according to an earlier note by Trepp.

At the time of securitization in 2017, the collateral was valued at $459 million. By March this year, the collateral value had been slashed by 74%, to $121 million according to Special Servicer notes. The loan, which matured in November, has not been paid off and is now in foreclosure, according to Trepp.

75 Broad Street, New York City: $176 million, 30 days delinquent. The 34-story nearly 100-year-old tower in Lower Manhattan was acquired by JEMB Realty in 1999 and renovated in 2017, according to JEMB. In 2017, it borrowed $176 million against the tower, at 4.077%. At the time, the tower was appraised at $403 million.

“This is the rebirth of a true original, a shining example of JEMB Realty’s expertise in value-enhancing properties so as to attain their full potential while remaining on top of ever-evolving trends and needs in office-using industries,” JEMB says.

The loan was sliced into three pieces and securitized: The AA1 piece of $59 million and the AB piece of $84 million are sole assets in the CMBS, NCMS 2017-75B. The AA2 piece of $33 million makes up 4.95% of UBSCM 2017-C1, according to Trepp.

JEMB failed to make interest payments, the 30-day grace period came and went, and in June, the loan was deemed 30 days delinquent.

Federal Center Plaza, Washington, DC: $130 million, maturity default. The property consists of two adjoining eight-story class-B office buildings of about 725,000 square feet combined.

About 71% of the space is leased by the US government: FEMA leases 64.7% of the space which serves as its headquarters; that lease expires in 2027; and USAID leases 6.5%, and that lease expires in six months.

The property was appraised at $309 million when the loan was issued. In February 2023, before the DOGE chaos snowed upon government-leased buildings, the appraised value was cut to $237 million. Earlier this year, KBRE estimated that the collateral had a liquidation value of $122 million.

The loan came due in February and has not been paid off. After the forbearance period, it became delinquent. The loan makes up 56.5% of the remaining collateral behind COMM 2013-CR6.

The top three delinquent loans that were “cured” and came off the list:

Selig portfolio, Seattle, $220 million, cured by transfer to a “custodial receiver.” The office empire of Seattle’s “office king” Martin Selig, once counting 30 buildings in downtown Seattle, has been unraveling in recent months in large chunks. The latest hit came in June, when the court transferred a 9-office building portfolio to a custodial receiver, after Selig had defaulted on the debt.

That transfer to a custodial receiver took the loan off the delinquency list and “cured” that delinquency.

1000 Wilshire Boulevard, Los Angeles, $128 million, cured by “performing maturity balloon.” The loan went into maturity default in March 2025, when the borrower, an entity of Cerberus Capital Management, failed to pay off the loan. Apparently, some a deal has been reached. Trepp said that the loan is now listed as “performing maturity balloon” and is no longer considered delinquent.

393-401 Fifth Avenue, New York City, $94.8 million, cured by extend and pretend. The landlord (the Chetrit Organization) had failed to pay off the loan when it matured in January 2025. A deal has now been reached between them and the special servicer to extend the loan from the original maturity date for 18 months to July 2026, according to Trepp. Extend and pretend in all its glory.

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()