The de facto buyers’ strike on Russian crude that began a month ago propelled oil prices to their highest levels in years. Now the real effects are starting to create a second wave of impact on oil markets, disrupting Russian exports and threatening further price increases.

Major energy companies and commodity-trading houses balked at buying crude oil from Russia in the days following the invasion of Ukraine. Banks also stopped financing these trades, shippers refused to load cargoes and insurers stopped covering them, fearful of running afoul of sanctions or upsetting company stakeholders.

Oil is typically shipped around three weeks after a deal is struck, meaning that the drop in deal making in the early days of the war led to real disruptions in supply starting in the past week. The turmoil is being strongly felt in Europe, where prices for diesel, which powers cars, trucks and tractors, have soared.

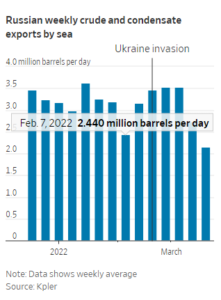

Exports of Russian oil by sea fell to the lowest level in nearly eight months last week, according to data from Kpler. In the first two weeks following the invasion, these volumes remained strong as trades made before Russian troops crossed the border on Feb. 24 were delivered.

UBS estimates that around 2 million barrels a day, or about a fourth of the Russian output, has been disrupted. The International Energy Agency forecast that the level could reach 3 million by next month, warning of a potential spark in the worst energy-supply crisis in decades.

“Commodities tend to price in the now, not the future,” said Giovanni Staunovo, a commodity analyst at UBS. “We are starting to see some disruption in the volumes of both crude oil and products from Russia. If we get more disruptions going forward, the price will react even more.”

Global benchmark Brent crude rose 9% last week, settling around $117 a barrel after two consecutive weeks of declines. Oil prices have long responded to the push and pull between speculators in futures markets and traders who buy and sell actual barrels of oil, with both trying to assess how much supply there is at the moment and how much there will be in the future. It is harder for oil traders to make those judgments now, with the usual buyers of Russian oil on the sidelines.

Russia is the world’s third-largest oil producer, behind the U.S. and Saudi Arabia. Before the war, it supplied about 7.5% of the world’s crude oil and refined products. The U.S., Canada, the U.K. and Australia have barred oil imports from Russia, while the European Union, its biggest customer, continues to buy but has started discussions about curbing purchases in the future.

There has been an exodus of oil companies from the country, including BP PLC and Shell PLC, as well as oil-services firms including Halliburton Co. , Baker Hughes Co. and Schlumberger Ltd.

The world consumes around 100 million barrels of oil a day. The hit to global supply affects a market already tight because of curbs in output by the Organization of the Petroleum Exporting Countries and its allies. Oil companies have been slow to spend on new oil fields with shareholders pushing for a shift to cleaner energy sources and fatter cash payouts.

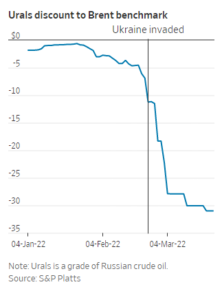

A common type of Russian oil, known in the industry as Urals, is priced at an increasingly wide discount, signaling that buyers of Russian oil remain skittish. The trading arm of the Russian oil major Lukoil tried to sell Urals crude at $31 below Brent last week, according to a trader. That was bigger than the gap two weeks ago, when the gap was around $28. Before the war, Urals mostly traded close to benchmarks.

A Lukoil spokesperson didn’t immediately respond to a request for comment.