There is growing speculation that the Organization of the Petroleum Exporting Countries and allied producers (OPEC+) will agree on June 4 to cut production. Brent crude prices fell below $73 per barrel this week, and price declines in recent weeks erased all of the gains since the last voluntary OPEC+ cuts were announced in early April. The Saudi energy minister recently issued a warning to “speculators” betting on deeper declines, which the market interpreted as a signal of potential cuts. Whether OPEC+ announces a steeper production cut or decides to stay the course this weekend, it faces a dilemma. Russia has failed to dial back production as promised in recent months, and maintaining credibility will be difficult without better compliance from Moscow.

It would be somewhat surprising to see a deeper OPEC+ cut. In early April, several OPEC+ countries abruptly announced 1.16 million barrels per day (b/d) in voluntary cuts just before the group’s scheduled meeting. Those reductions began only in May, and it may be too soon to judge the impact. Both OPEC and the International Energy Agency expect a tighter market in the second half of the year. OPEC anticipates 2.3 million b/d in oil demand growth in 2023, with China contributing 800,000 b/d of that total. OPEC expects an especially strong third quarter, with 2.5 million b/d in year-on-year demand growth. Apparent oil demand in China topped 16 million b/d in April for the first time in history, partly due to domestic refiners taking advantage of discounted Russian oil. Bullish demand forecasts suggest that if OPEC+ maintains its previously agreed production cuts, the market will move into deficit in the third and fourth quarters, supporting higher prices.

Still, a cut remains quite possible. Saudi energy minister Abdulaziz bin Salman has repeatedly argued that price fluctuations are disconnected from market fundamentals. Bank failures and fears of financial sector contagion led to a sharp sell-off in March, prompting Saudi Arabia and others to make surprise voluntary cuts. A similar pattern has taken place in recent weeks, with a sharp increase in short speculative positions as the market remains concerned about economic weakness in the United States and Europe. The April cuts suggested OPEC+ will guard against downside risks, and the group may conclude that without further reductions at this meeting, prices will tumble. More importantly, the talk about “speculators” could be masking deeper concerns about the macroeconomic outlook. In China, for example, a recovery in mobility and a sharp increase in domestic flights have boosted oil demand, but there are ongoing concerns about weakness in the construction and property sectors that could dampen commodity demand.

OPEC+ also seems keen to defend a higher price floor. Saudi Arabia is in the early stages of an economic transformation plan that depends on a massive state-led investment push. Its government budget fell into deficit in the first quarter of 2023, despite an increase in non-oil revenue, and Riyadh anticipates large capital expenditures this year. Saudi Arabia’s fiscal breakeven price for 2023 is $81 per barrel, according to the International Monetary Fund. To be sure, Saudi Arabia would have no trouble absorbing budget deficits for several years. The kingdom still has about $410 billion in foreign exchange reserves, sufficient for nearly 30 months of import cover, although its reserves are now at the lowest level in more than a decade. But lower oil revenue certainly complicates Saudi Arabia’s spending plans. An $80 per barrel market is much more comfortable for Saudi Arabia and its partners than $70 per barrel or below. OPEC+ may be more confident that the global economy can absorb slightly higher prices, with economy-wide inflation now less of an acute threat to growth in the United States and other markets.

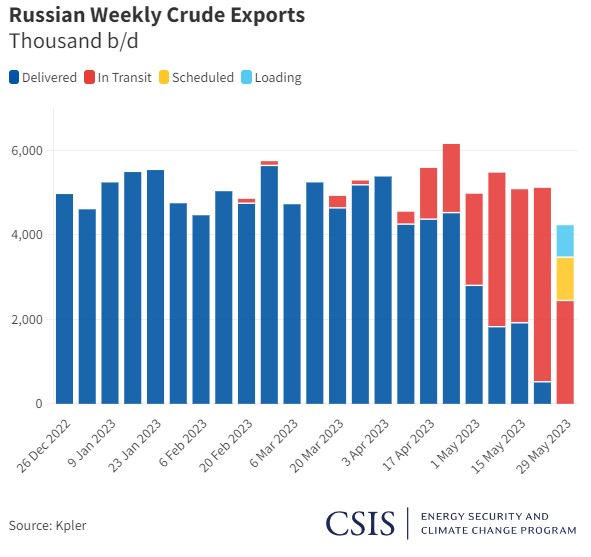

In managing this market, OPEC has a Russia-sized problem. Russia pledged to cut output by 500,000 b/d beginning in March, but through the end of May it had failed to make sizeable reductions. Instead, the country has been maximizing output. The goal is probably to offset Russia’s declining revenue per barrel due to the EU embargoes and price caps that are forcing it to ship oil over longer distances to a dwindling pool of buyers. Poor compliance with OPEC+ targets is nothing new for Russia. Since the signature of the Declaration of Cooperation which created the OPEC+ grouping in December 2016, Russia has frequently produced above its target. Saudi Arabia, the United Arab Emirates, and others in OPEC+ have often talked about the success of OPEC+ and the benefits of cooperation with Russia. But patience with Moscow’s lack of production discipline may be wearing thin.

The problem for OPEC+ is that deeper production cuts without better Russian compliance would only hurt other producers—and could well disincentivize others from adhering to the cuts if they regard Russia as a free rider. Russia’s pivot in oil sales to India and China has also expanded its market share in those critical centers of demand growth, placing the Gulf producers at a disadvantage. (Gulf producers are exporting more crude to Europe and other markets to replace Russian volumes, but these are regions with flat to declining demand.)

At this stage, it may be more important for OPEC+ to urge stronger compliance from its members, above all Russia, than to announce larger production cuts that may be hard to enact. For years, Saudi energy ministers have worked to build consensus and cohesion within OPEC. But the EU embargoes, EU-G7 price caps, and changes in global energy flows resulting from Russia’s war on Ukraine are starting to expose some latent tensions between Russia and its OPEC+ partners.

Ben Cahill is a senior fellow with the Energy Security and Climate Change Program at the Center for Strategic and International Studies in Washington, D.C.