Forecast overview

- The November 2022 Short-Term Energy Outlook (STEO) marks the release of our new text format. We have reconfigured the text to provide readers with discussions and visualizations we think best convey our energy forecast and its key drivers.

- Uncertainty in macroeconomic conditions could significantly affect energy markets in the forecast period. Based on the S&P Global macroeconomic model, we now expect U.S. GDP will fall slightly in 2023, which we forecast will contribute to a drop in total U.S. energy consumption next year.

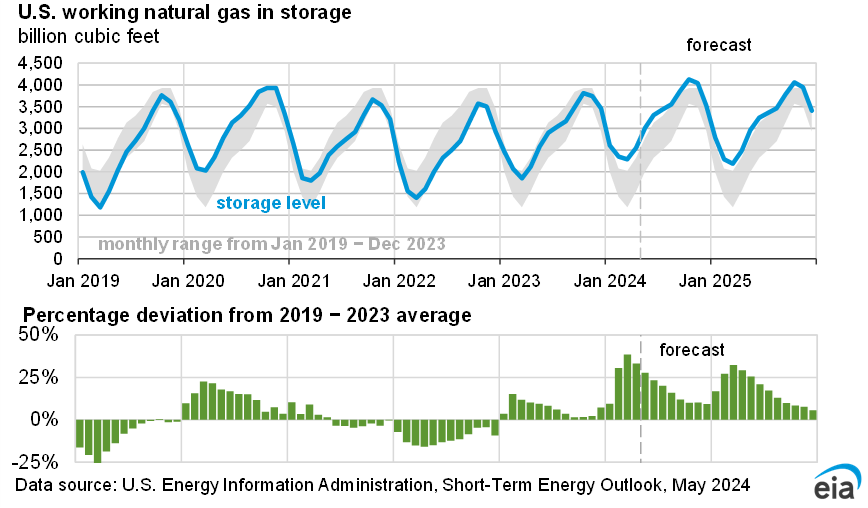

- We estimate U.S. natural gas inventories ended October 2022 at more than 3.5 trillion cubic feet (Tcf), which is 4% below the five-year average and higher than what we had been forecasting in recent months. They fall in our forecast by 2.1 Tcf this winter to 1.4 Tcf by the end of March 2023. This withdrawal would be similar to the five-year average and result in inventories that are 8% below the five-year average at the end of March 2023.

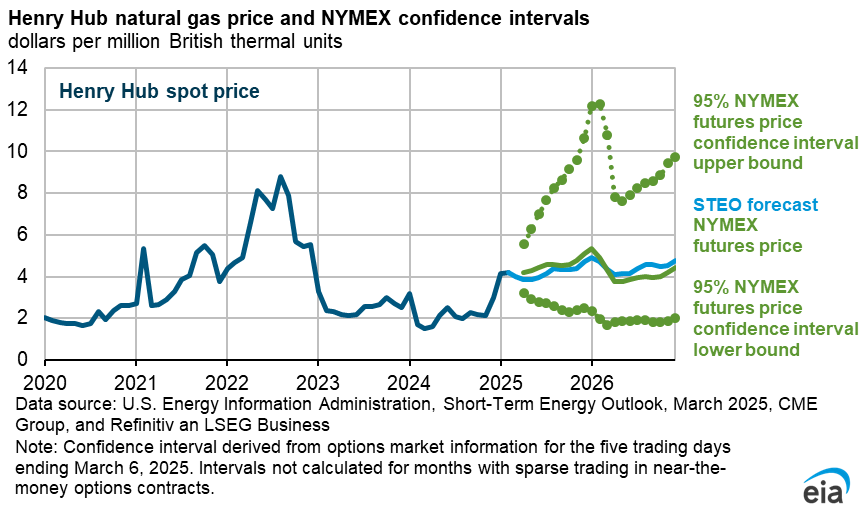

- Because of higher-than-expected storage levels heading into winter our forecast natural gas spot price at Henry Hub averages about $6 per million British thermal units (MMBtu) across 4Q22 and 1Q23, which is more than $1/MMBtu lower than we forecast in the October STEO. We expect natural gas prices will decline after January as the deficit to the five-year average in inventories decreases.

- We expect renewable sources to provide 22% of U.S. electricity generation in 2022 and 24% in 2023 as generation from natural gas declines from 38% in 2022 to 36% in 2023. The increase in renewables generation comes mostly from solar and wind capacity additions.

- U.S. distillate fuel inventories average 17% below the five-year average in our forecast for 2023. We estimate distillate inventories were 104 million barrels at the end of October, the lowest end-of-October level since 1951.

- Retail heating oil and diesel prices will continue to average more than $5 per gallon for the rest of 4Q22. We expect a slightly contracting U.S. economy will reduce distillate prices in the first half of 2023 (1H23). However, the EU’s ban on seaborne imports of petroleum products from Russia creates supply uncertainty for distillate markets in early 2023.

- Higher heating oil prices and consumption, due to colder forecasted temperatures this winter, result in our expectation that the average U.S. home that uses heating oil as its primary space heating fuel will see expenditures increase by 45% compared with last winter. In last month’s Winter Fuels Outlook, we forecast expenditures would rise 27% over last winter in the baseline.

- We forecast OPEC crude oil production will fall in November and December. Annual OPEC production averages 28.9 million barrels per day (b/d) in 2023, up by 0.3 million b/d from 2022.

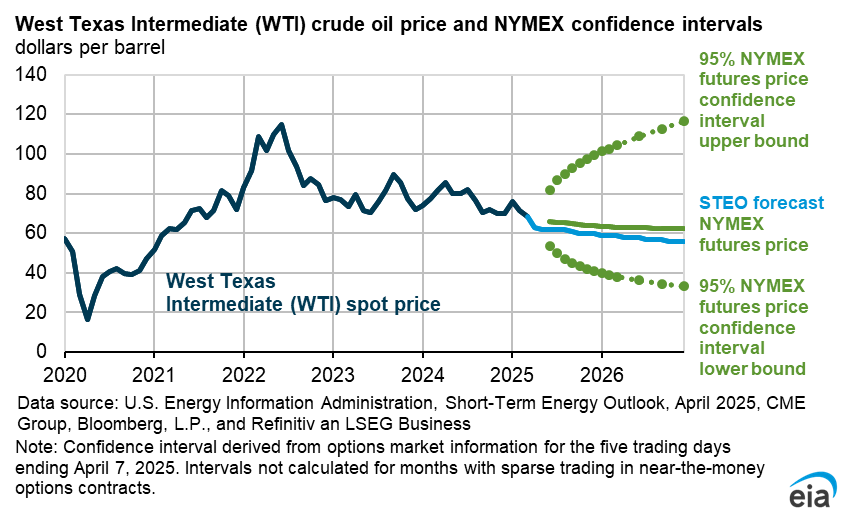

- Growth in OPEC and non-OPEC oil production—most notably production in the United States—keeps the Brent crude oil price in our forecast lower on an annual average basis in 2023 than in 2022. However, we expect the Brent crude oil price will begin rising in 2H23.

| Notable Forecast Changes | 2021 | 2022 | 2023 |

|---|---|---|---|

| The current STEO forecast was completed November 3. The previous STEO forecast was completed October 6. |

|||

| U.S. Real GDP (percentage change) | 5.9% | 1.7% | -0.1% |

| Previous | 5.7% | 1.7% | 1.3% |

| Percentage point change | 0.2% | 0.0% | -1.4% |

| Henry Hub spot price (dollars per million Btu) | $3.91 | $6.49 | $5.46 |

| Previous | $3.91 | $6.88 | $5.77 |

| Percentage change | 0.0% | -5.8% | -5.4% |

| Diesel retail price (dollars per gallon) | $3.29 | $5.09 | $4.65 |

| Previous | $3.29 | $4.97 | $4.29 |

| Percentage change | 0.0% | 2.5% | 8.4% |