QT has drained ON RRPs to their normal level of near-zero, while QT hasn’t even touched reserve balances yet.

By Wolf Richter for WOLF STREET.

Balances at the Fed’s facility for Overnight Reverse Repurchase agreements (ON RRPs) have dropped below $80 billion for the second day in a row today, the lowest since April 2021, down from $2.4 trillion at the peak in December 2022, and well on their way to near-zero, where they were in normal times, and where the Fed wants them to be again as part of its QT, which by now has removed $2.1 trillion from the Fed’s balance sheet.

RRPs represent excess liquidity in the money markets that they don’t know what else to do with. This liquidity is outside the banking system. And it dropped by more ($2.3 trillion) than the liquidity removed via QT ($2.1 trillion).

To help ON RRPs get to near-zero, the Fed lowered its ON RRP offering rate – one of its five policy rates – at the December meeting by 5 basis points, in addition to the 25-basis-point cut on all its five policy rates. At 4.25%, the offering rate is now at the bottom of the Fed’s target range for the federal funds rate, as it had been before June 2021.

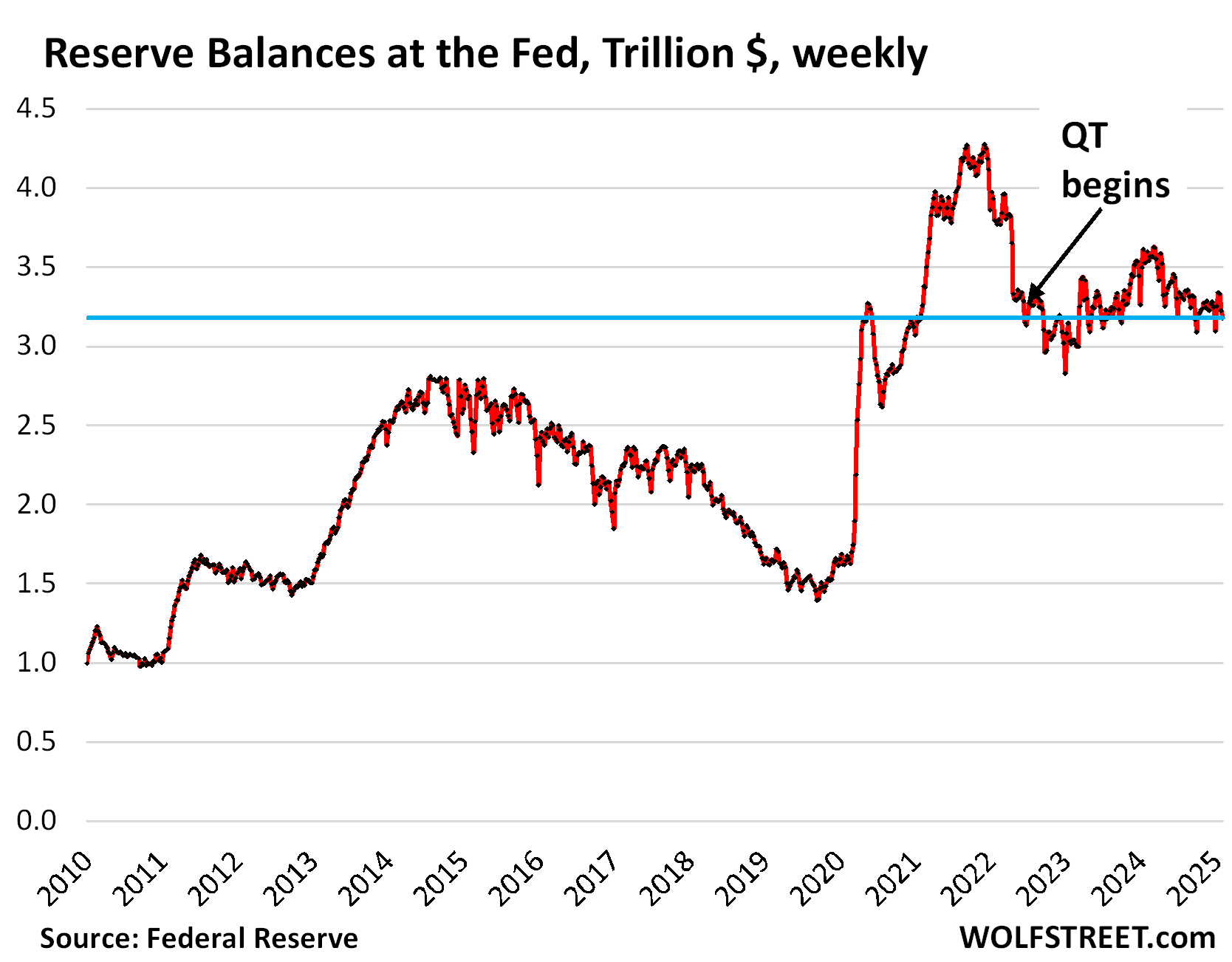

By contrast, reserve balances have not come down at all since QT started in July 2022. They’re now at $3.18 trillion, as of today’s balance sheet, about where they’d been in July 2022 when QT started, despite some ups and downs in between.

Yet bringing down reserve balances from the current “abundant” levels to merely “ample” (sufficient, adequate) levels is the primary purpose of QT. Reserves represent excess liquidity in the banking system that banks have deposited at the Fed.

All of the QT so far has come out of ON RRPs. But it’s reserve balances that indicate how much longer QT can continue – not ON RRPs. And as far as reserves are concerned, the impact of QT hasn’t even started yet:

The spike and its unwind in reserves started in January 2021, peaked in December 2021 at $4.25 trillion, and then liquidity shifted from banks to money markets, which caused reserves to plunge at the time and ON RRPs to balloon. But when QT started in July 2022, reserves were back at about $3.2 trillion and sort of stabilized at that level, while ON RRPs were being drawn down by QT.

Back in the day before QE, before 2008, reserve balances – then called “excess reserves” and “required reserves” – were small. Excess reserves were near-zero in the two decades before 2008, and required reserves, required by bank regulations, were between $38 billion and $60 billion in the two decades before 2008, just before QE kicked in.

Instead of piling up excess liquidity at the Fed, the banks satisfied their daily liquidity needs by borrowing from the Fed in overnight repo transactions at the Fed’s Standing Repo Facility (SRF) at the time. And that worked fine until QE messed up that system.

The Bernanke Fed, after it had started QE and reserves started piling up, killed the SRF because it was no longer needed.

Then in July 2021, in anticipation of QT drawing down the balance sheet, the Fed revived the SRF while no one was even paying attention because the Fed was still doing QE at the time. With the SRF, the Fed engages with approved counterparties (banks) in overnight repos. Banks can then lend those funds to the regular repo market if repo rates rise for some reason, and make money on the difference, which will keep repo rates from blowing out.

So in theory, the Fed now has the tools in place to shift from these huge piles of reserves on its balance sheet (and paying interest on them to the banks) to drawing down those reserves slowly but very substantially through ongoing QT and providing daily liquidity to banks as needed via its SRF (and charging interest on those repos).

When the repo market blew out in September 2019, the Fed did not have the SRF in place and was not prepared to deal with it, and was surprised by it. The revival of the SRF was a lesson learned from the repo market blowout. The mere presence of the SRF will prevent that sort of thing. And that, in theory, would allow the Fed to trim reserves slowly and over time by a lot more than Wall Street media outlet claim.

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the beer and iced-tea mug to find out how:

Would you like to be notified via email when WOLF STREET publishes a new article? Sign up here.

![]()