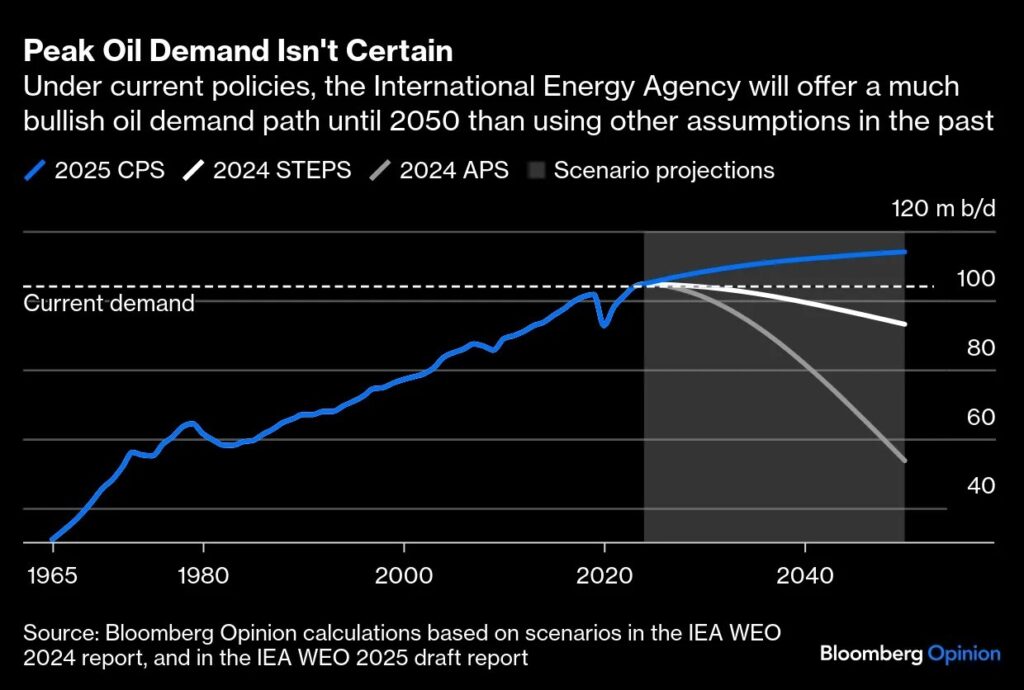

In the ever-evolving landscape of global energy, the narrative of an impending “peak” in fossil fuel demand has long been a cornerstone of climate policy and investment strategies. Proponents argued that as renewables like wind and solar scale up, oil, gas, and coal consumption would inevitably plateau and decline within the decade. However, recent projections and real-world data are dismantling this myth. A draft of the International Energy Agency’s (IEA) annual report, as highlighted in a Bloomberg opinion piece, reveals that under current policies, oil and natural gas demand will continue to rise through 2050.

On the Energy News Beat podcast, we just recorded an episode with Trisha Curtis, CEO of Petro Nerds, and it is in production, talking about Peak Permian and Peak oil. She is an outstanding energy leader, and we have a lot of insights to share on this topic. Investors will look for returns, and it is not happening in the wind, solar, and hydrogen space.

This isn’t just a minor adjustment—it’s a seismic shift that underscores the world’s ongoing reliance on fossil fuels amid surging demand from major economies.

Are you Paying High Taxes in New Jersey, New York, or California?

The article’s author, echoing broader industry sentiments, declares: “For the last few years, climate and energy policymakers have convinced themselves the world was inexorably moving away from fossil fuels. Breaking news: It is not.”

Instead, the global energy story is one of “energy addition,” where renewables supplement rather than supplant fossil fuels. With coal expected to peak in the 2030s but remain 50% higher than prior forecasts by 2050, and oil hitting 114 million barrels per day by mid-century under the IEA’s Current Policy Scenario (CPS), the peak demand illusion is crumbling.

This CPS, reinstated amid policy pressures, strips away optimistic assumptions about unfulfilled pledges, painting a more realistic picture of sustained fossil fuel growth.

Surging Demand in the Top Ten Countries

The top ten countries by fossil fuel consumption account for the lion’s share of global demand, and their trajectories are accelerating, not decelerating. In 2025, these nations—led by the United States and China—consume over half of the world’s oil and a similar proportion of total fossil fuels, driven by industrialization, population growth, and economic recovery.

Here’s a breakdown of the top ten by oil consumption, which serves as a proxy for broader fossil fuel trends, based on 2025 estimates:

(Data compiled from 2025 projections; total top 10: ~59.5 million bpd, ~60% of global demand.)

These figures show no signs of peaking. China alone consumed nearly 40% more coal than the rest of the world combined in recent years, with total fossil fuel use up due to hydropower variability and industrial needs.

India’s oil demand is projected to grow 4-5% annually through 2030, fueled by its expanding economy.

Even in the U.S., despite efficiency gains, total energy consumption hit record levels in 2024, with fossils still dominating at over 80% globally.

The IEA’s CPS aligns with this, forecasting oil growth into the 2040s, as emerging markets like India and Southeast Asia offset any Western declines.

The Hidden Costs of Wind and Solar: Why Renewables Aren’t a Quick Fix

While wind and solar have seen cost reductions in nameplate capacity—down significantly over the past two decades—their integration into grids reveals substantial additional expenses that undermine the peak demand narrative.

Intermittency requires baseload support from gas peaker plants or batteries, ballooning system costs. In Texas, for instance, wind and solar variability has added billions to ratepayer bills through backup generation and curtailment losses.

Transmission lines pose another hurdle. Global grids need a two-fold investment surge to $600 billion annually by 2030 to accommodate renewables, as remote wind and solar farms demand new high-voltage lines.

In the U.S., Northeast grid upgrades are estimated at $125 billion, while Western interconnections could cost $150 billion, driven by the need to wheel power from variable sources.

Balancing costs—offsetting forecast errors—and grid reinforcement further inflate expenses, often overlooked in levelized cost of energy (LCOE) calculations.

Land costs compound the issue. Utility-scale solar and wind require vast acreage—up to 10 times more than gas plants for equivalent output—driving up acquisition and environmental mitigation expenses in 2025’s inflationary environment.

Power purchase agreement prices for new projects have risen steadily since 2021, with wholesale electricity costs projected to jump 19% from 2025-2028 due to these factors.

Although some studies claim integration costs are “relatively small” compared to fuel savings, critics argue this ignores long-term reliability risks and the need for overbuilding capacity (e.g., 2-3x nameplate for intermittency).

These realities slow the renewables ramp-up, ensuring fossil fuels fill the gap for decades.

What Investors Should Look For in U.S. Public and Private Oil Companies

With fossil demand resilient, U.S. oil companies—public and private—offer compelling opportunities in 2025. The sector’s focus on capital discipline amid volatile prices (expected $70-90/bbl) positions well-managed firms for returns.

For public companies (e.g., ExxonMobil, Chevron, ConocoPhillips), prioritize:

Low breakeven costs: Firms with Permian Basin exposure, where production costs hover at $40-50/bbl, ensure profitability even in downturns.

Strong balance sheets and shareholder returns: Look for high dividend yields (3-5%) and buyback programs; energy stocks underperformed in 2024 but are poised for elevated prices in 2025.

Technological edge: Investments in AI-driven drilling and carbon capture for regulatory compliance.

Diversification: Companies with LNG export or petrochemical arms hedge against pure upstream volatility.

For private companies (e.g., via direct investments or funds), opportunities abound as private equity rebounds:Tax advantages: Direct participation programs (DPPs) offer deductions for intangible drilling costs (up to 70-80% in year one) and depletion allowances, ideal for high-income investors.

High-yield potential: Working interests in shale plays can yield 20-50% IRR, but vet for proven reserves and operator experience.

M&A activity: With $105 billion in 2025 deals, target consolidators in the Permian or Bakken for scale efficiencies.

Private firms face less regulatory scrutiny but require due diligence on liquidity—consider funds for diversification.

Geopolitical resilience: Focus on U.S.-centric assets to mitigate global risks.

Overall, blend public stocks for liquidity and private deals for alpha, allocating 5-10% of portfolios to energy amid supply constraints.

The Bottom line

The myth of peak fossil-fuel demand is not just falling apart—it’s being buried under the weight of real demand data and the practical barriers to renewables. As top countries like China and India drive consumption higher, investors who recognize this reality stand to benefit from U.S. oil’s enduring strength. In a world adding energy rather than transitioning away from fossils, the future looks bright for those betting on black gold.

We are seeing investors seek returns on their investments. That is not in the “renewable” wind, solar, or hydrogen space. As we conduct oil and gas evaluations in our day job, we are seeing the due diligence required for well economics in lower oil prices, as well as maintaining returns for investors. That means being selective about which wells are being drilled by oil and gas exploration companies.

Avoid Paying Taxes in 2025

Crude Oil, LNG, Jet Fuel price quote

ENB Top News

ENB

Energy Dashboard

ENB Podcast

ENB Substack