In the wake of geopolitical shifts and Europe’s ongoing quest for energy security, U.S. oil supermajors are ramping up their presence in the liquefied natural gas (LNG) market. Companies like ExxonMobil and Chevron are expanding their trading operations to capitalize on Europe’s demand for reliable, non-Russian gas supplies.

This strategic pivot follows the playbook of European giants such as Shell, BP, and TotalEnergies, who have long dominated LNG trading.

With U.S. LNG exports hitting record highs in August 2025, the stage is set for American firms to deepen their footprint in Europe, potentially reshaping global energy flows.

Pathways to Doubling U.S. LNG Production

The U.S. is already the world’s largest LNG exporter, shipping out 11.9 billion cubic feet per day (Bcf/d) in 2024, and projections indicate exports could grow by about 10% annually through 2030.

To double production capacity—from the current 11.4 Bcf/d to over 22 Bcf/d by 2028—industry leaders are focusing on expanding export terminals and upstream gas supplies.

Key enablers include:New Export Facilities:

Projects like Plaquemines LNG (Phases 1 and 2) and Corpus Christi Stage 3 are slated to come online, adding significant capacity.

Overall, North America’s LNG export capacity is on track to more than double between 2024 and 2028, driven by 80 million tonnes per annum (mtpa) under construction and another 141 mtpa proposed.

Shale Gas Ramp-Up: Growth in shale production from basins like Haynesville and Permian will fuel this expansion, with producers responding to demand from both domestic utilities and international exporters.

The domestic LNG market has quadrupled in the last 20 years and is poised to double again by 2030.

Infrastructure Investments: Billions are being poured into pipelines and terminals to handle the surge, with exports already up 21% in the first half of 2025 after a flat 2024.

However, challenges like oversupply risks and global demand uncertainties—particularly from China—could temper this growth.

This expansion not only boosts U.S. energy independence but also positions the country as a stabilizing force in global markets, especially amid volatility from OPEC+ policies and geopolitical tensions.

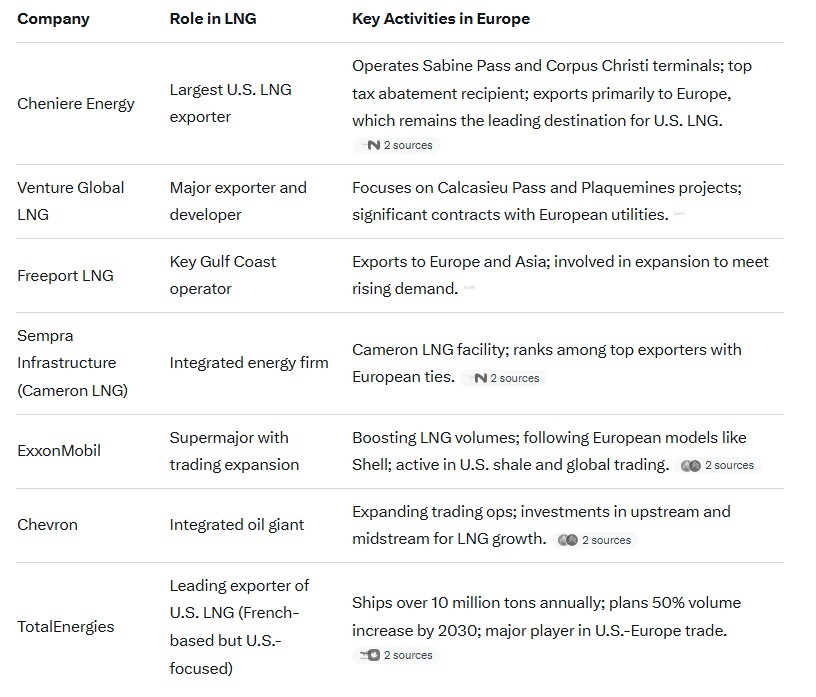

Key U.S. Companies Leading the Charge

Several major U.S. firms are at the forefront of LNG exports to Europe, blending production, trading, and infrastructure expertise. Here’s a breakdown of the top players:

These companies have propelled the U.S. to supply 45% of the EU’s LNG needs in recent years, with Europe still the top destination despite diversions to Egypt and Latin America.

Investments in Midstream, Upstream, and Shipping

To support this boom, investments are flowing across the LNG value chain:

Upstream (Oil and Gas Production): Focus on shale gas in Haynesville and Permian basins, where low costs and proximity to export hubs drive growth.

U.S. upstream firms have prioritized capital discipline and acquisitions, with production rebounding in 2025.

Producers scaled back in 2024 but are now increasing output to meet exporter demands.

Midstream (Pipelines and Terminals): Natural gas pipeline expansions are key, with the U.S. midstream sector eyeing growth tied to hydrocarbon exports.

LNG terminal capacity is set to double the industry’s economic footprint by 2040, with 90 mtpa current capacity and 80 mtpa under construction.

Dealmaking has accelerated post the January 2025 LNG export permit ban lift, benefiting midstream operators.

Shipping Companies: While specific U.S. shipping investments are less highlighted, global LNG tanker demand is rising with exports. Firms like those in the broader energy sector are investing in fleets to transport U.S. LNG to Europe, amid shifting dynamics in European gas imports and Middle Eastern competition.

Overall, these investments enhance resilience, with natural gas fueling midstream growth in 2025.

Existing U.S.-EU LNG Contracts and Agreements

The U.S.-EU relationship in LNG is underpinned by a recent non-binding trade deal, where the EU commits to importing $250 billion annually in U.S. energy—totaling $750 billion by 2028—including LNG, oil, and nuclear fuels.

Viewed as a political symbol rather than a market game-changer, it aims to bridge trade gaps and reduce Europe’s reliance on Russian gas.

Key details include:

Volume Commitments: Around 23 billion cubic meters per year (bcm/y) of contracts signed with U.S. LNG projects under construction, with 55% going to European utilities.

The U.S. provided 28% of EU LNG imports in recent data (22.3 bcm), making it the top supplier ahead of Qatar.

Strategic Purchases: Mix of spot buys and long-term contracts; the deal could boost U.S. exports but faces complexities like global oversupply.

Implications: No new U.S. LNG capacity is strictly needed for the EU to replace Russian gas, as recent additions already exceed requirements.

However, the pact sparks a “race” for European markets, potentially reshaping infrastructure and prices, and if they stop buying the 18% they are still buying from Russia, they will need more quickly.

As U.S. oil giants double down on European strategies, the LNG sector promises innovation, competition, and energy stability—but not without navigating oversupply and geopolitical hurdles.

We are starting a series of evaluations of companies in the midstream, LNG, and Exploration side of the natural gas and LNG markets for investors.

Avoid Paying Taxes in 2025

Crude Oil, LNG, Jet Fuel price quote

ENB Top News

ENB

Energy Dashboard

ENB Podcast

ENB Substack