By Michael Every of Rabobank

Stop projecting; and start projecting

This week is obviously dominated by the upcoming Fed meeting. On which note, please – stop projecting, at least in one regard.

US personal income and expenditure data on Friday showed a now-established decline in spending on goods and the start of a slowdown in spending on services, which had been hotter, while savings starting to rise again. That’s exactly what the Fed wants to see, and adds to recent softness in other data. However, to project this means the Fed will be slashing rates soon is projection in a psychological sense, i.e., putting one’s own feelings onto the actions of others. It’s the desire for big Fed rate cuts, leading to lower bond yields, and a weaker US dollar, and higher asset prices, and the status quo ante of the past 40 years.

We are seeing deflation: in memory chips, used cars (US auto delinquencies are now looking worse that during the GFC, apparently), and housing. The US fiscal tap may remain turned off in the outside the defence sector too. Yet the unemployment rate remains low, and so do weekly initial claims: Covid has changed things through deaths, early retirement, and walking away. Moreover, Europe may avoid recession and China has reopened and says –again– that it will boost consumption: they are proposing higher welfare payments for rural immigrants to cities, for example. In short, while inflation will fall back near-term, it could potentially start to rise again later this year.

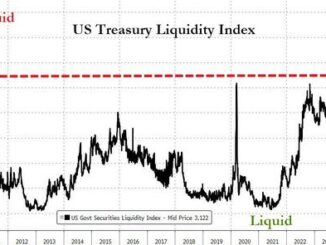

Consider what slashing rates would do against that backdrop. Indeed, alongside the easing in US financial conditions vs. a few months ago (the S&P +6% year-to-date; US 10-year yields 35bp lower) we see: Brent crude +1.8% y-t-d; copper +11.2%; gold +5.8%; and even Bitcoin +43.7%. Somebody is projecting more growth, more bubbles, and more supply-side inflation.

Worse, markets are refusing to project headlines such as the Financial Times saying: ‘Top US air force general predicts China conflict in 2025‘: if you cover the Fed or the ECB, or pensions or potatoes, or stocks or bonds, that headline warns current projections could be more dramatically wrong in 2025 than they were in 2022.

Of course, market analysts can never say what will happen in geopolitics, let alone markets. Yet the standard procedure in research is to note such a headline and say, “That’s wrong!” – with no professional experience in such matters; or to pretend one did not see it; or to say, “We don’t (know how to) look at such issues,” and, rightly, “We can’t price for them,”…and so to continue to project what one does know about and can price for; like Fed rate cuts and asset markets rallying. But is that really a good way to project things?

That headline is likely lobbying for even higher Pentagon budgets and more friend-shoring – yet that has inflationary implications and flusters businesses. So does Japan and the Netherlands joining the US in restricting exports of chip and chip-manufacturing tech to China (though the Dutch allowed millions of chips to be sold to Russia despite a US ban); and the headline, ‘Key lawmaker: Biden mulling broad prohibitions on U.S. investments in Chinese tech‘, noting, “The Biden administration “is talking about a theory where they would stop capital flows into sectors of the economy like AI, quantum, cyber, 5G, and, of course, advanced semiconductors… They actually want to say, right, you can’t invest in any [Chinese] company that does AI. You can’t invest in any company does cyber” or other similar sectors.

Nearer term, a few weeks from the first anniversary of the war, Russia is close to a new surge in Ukraine, which won’t get a small number of Western tanks for months. The fora discussing sending tanks a few months ago, as Germany said it would never allow that to happen, are now discussing sending fighter jets,… which Germany says it will never allow to happen. The escalatory spiral is obvious. The risks of an inflationary spiral should not be underestimated either, especially if Russia strikes at, or for, a Ukrainian port, and/or the Black Sea Grain Deal collapses.

Israeli drones just attacked Iranian factories manufacturing the drones they are exporting to Russia for use against Ukraine. While there are no immediate risks of outright Iran-Israel war on the back of that, despite the recent, huge US-Israeli military exercise for exactly that kind of thing, it is literally explosive in a volatile region again central to global energy-price —and so inflation— projections.

Against this backdrop, Germany’s Chancellor Scholz was just in Latin America, ‘racing with China for lithium’, as Bloomberg puts it. That’s for his auto sector facing a pincer squeeze from surging Chinese auto exports, notably of lithium-using EVs, and a higher cost of energy now Russian pipeline gas is gone, benefitting the US, who are selling the LNG replacing Russian pipeline gas. Meanwhile, arms-maker Rheinmetall is ready to greatly boost the output of tank and artillery munitions to satisfy strong demand in Ukraine and the West, and may start producing HIMARS multiple rocket launchers in Germany, says its CEO. So, a shift in German industry from cars to tanks? However, after the debacle over German-built tanks, demand for them is, excuse the pun, tanking. So, a shift from German-made cars to US-brand military goods? What does this project about EU “strategic autonomy”, or even the level of the Euro, longer term?

Though it addresses deglobalisation more loosely, and focuses more on demographics, the Financial Times also has a pre-Fed op-ed worrying about structurally higher inflation rates – ‘The world is not ready for the long grind to come’. At least markets aren’t if they continue to project a 25bp hike this week, then a short pause, and then rate-cutting business as usual. What if the Fed goes 25bp, but hawkishly stresses that not only might it do so again one more time, but that it won’t be cutting rates for a *long* time? Could Powell push back directly against the market’s constant easing of financial conditions? If so, how do people with psychological projection problems react when confronted? Denial, then anger, then denial; and then very expensive therapy, if they want to become better-adjusted.

Relatedly, last week I noted famed economist Schumpeter, seen as always favoring “creative destruction”, ended up arguing for a quasi-‘Christendom’ corporatism to deal with problems of economic imbalances, based on the Catholic principle of Quadragesimo anno put forward by Pope Pius XI in 1931 – to no effect at all, as we saw from 1939-45. On that note, Friday saw economist Mariana Mazzucato (‘For the Common Good‘), argue we should follow the call of the current Vatican in a similar light: “Tackling our biggest challenges and reversing the undue concentration of wealth and power will require a fundamental change in political economy. Currently, the principle of the common good is seen as merely a corrective for the current system’s excesses, but it should be the system’s primary objective.”

Despite having argued for years that political economy and “-isms” were going to be the next big thing, I am in no way projecting that the change described above is going to happen anytime soon, or at all: would that it could. Yet project this: would a return to big Fed rate cuts make things relatively better or worse in that regard? Geopolitically, the answer is also clear: higher rates are a US weapon – yet, oddly, one the market expects to soon be holstered.

Loading…