Tesla’s energy storage division—once a quiet, high-margin moneymaker that outpaced the company’s slowing EV sales—has hit an unexpected bump. Bloomberg’s latest report highlights how the battery business, which fueled rapid revenue growth amid softening auto demand, suddenly stalled in early 2026.

In Q1 2026, Tesla deployed just 8.8 GWh of energy storage products—down about 15% year-over-year and a sharp drop from the record 14.2 GWh in Q4 2025. Full-year 2025 was a blowout: 46.7 GWh deployed (up 49% YoY), generating roughly $12.8 billion in revenue (up 27%) with gross margins hitting a strong 29.8%.

Why the stall? Analysts point to low-cost competition (especially from China), pricing pressure on Megapacks, tariff impacts, and policy uncertainty. Average selling prices (ASPs) have declined as the market matures, and short-term supply-chain frictions or project delays may have played a role. Yet Tesla’s backlog remains “strong and well-diversified globally,” and the company is already launching next-generation products like Megapack 3 and the 20 MWh Megablock.

Tesla’s Secret Weapon: A Supply Chain Like No Other

While the headlines focus on the slowdown, Tesla is doing something no other automaker or energy-storage player is matching at this scale: vertically integrating and localizing an entire battery supply chain in the West. Most competitors remain heavily reliant on Chinese cells, cathodes, and raw materials. Tesla is building resilience from mine to megapack.

Key moves reshaping the chain in real time:

Lithium refining: Tesla’s Texas lithium refinery—the first spodumene-to-lithium-hydroxide facility in North America—began operations and is scaling to support 30 GWh of annual capacity.

Cathode and cell production: Early cathode output is underway (target ~10 GWh/year). Gigafactory Nevada is nearing LFP cell production (initial 7 GWh/year) using CATL-derived equipment, with first output expected early 2026—primarily for energy storage.

Dry-electrode technology: Acquired via Maxwell, this solvent-free process cuts energy use, factory space, and toxic chemicals—already applied to 4680 cells.

Megapack factories: Lathrop, California (expanding), Shanghai (ramping past 2,000 units in 2025), and a new Houston, Texas plant targeting up to 50 GWh/year of Megapack 3 production starting late 2026.

Strategic partnerships and localization: A $4.3 billion deal with LG Energy Solution for a U.S. LFP battery plant in Michigan (online ~2027) plus aggressive phase-out of Chinese parts for the U.S. market by 2027 to dodge tariffs.

Tesla topped 2026 global sustainable supply-chain rankings with a historic jump in battery transparency—scoring over 50% in that category for the first time by any automaker.

This isn’t incremental tweaking—it’s total vertical integration at unprecedented speed and scope. While rivals face 18-month factory conversions and tariff headaches, Tesla is already deploying U.S.-made LFP cells for storage to qualify for full IRA tax credits and mitigate geopolitical risk.

How Investors Should View Tesla Long-Term

Short-term noise (EV sales softness, energy-deployment dip, high capex) has created volatility, but the long-term investment thesis has never been stronger for patient capital.

Diversified, high-margin growth engine: Energy storage is on track for ~$18.3 billion in 2026 revenue (up from $12.8 billion in 2025), with margins holding near 29% even amid compression. It already contributes a growing share of gross profit and is less cyclical than autos.

Structural tailwinds: Explosive AI/data-center power demand, renewable grid integration, and global decarbonization create a multi-trillion-dollar addressable market. Tesla’s software edge (Virtual Power Plants, grid optimization) and integrated ecosystem (Powerwall + Megapack + Solar) are difficult to replicate.

Moat from vertical control: By owning lithium refining, cathode, cells, packs, software, and deployment, Tesla controls costs, quality, and supply security in ways peers cannot. New products and factories position it to capture market share as competitors scramble.

Capital allocation reality: 2026 capex tops $20 billion, funding factories, AI/robotics, and energy scale-up. Free-cash-flow pressure is real near-term, but the payoff is a platform company with recurring software-like margins across energy, autonomy, and beyond.

Investors should value Tesla as a technology + energy infrastructure leader, not just an automaker. The battery business stall is a speed bump—not a structural flaw. With a strong backlog, new U.S. capacity coming online, and unmatched supply-chain agility, Tesla is positioned to rebound harder and dominate the next decade of energy storage growth.

Don’t count them out.

Appendix: Charts, Announcements & SourcesKey Charts

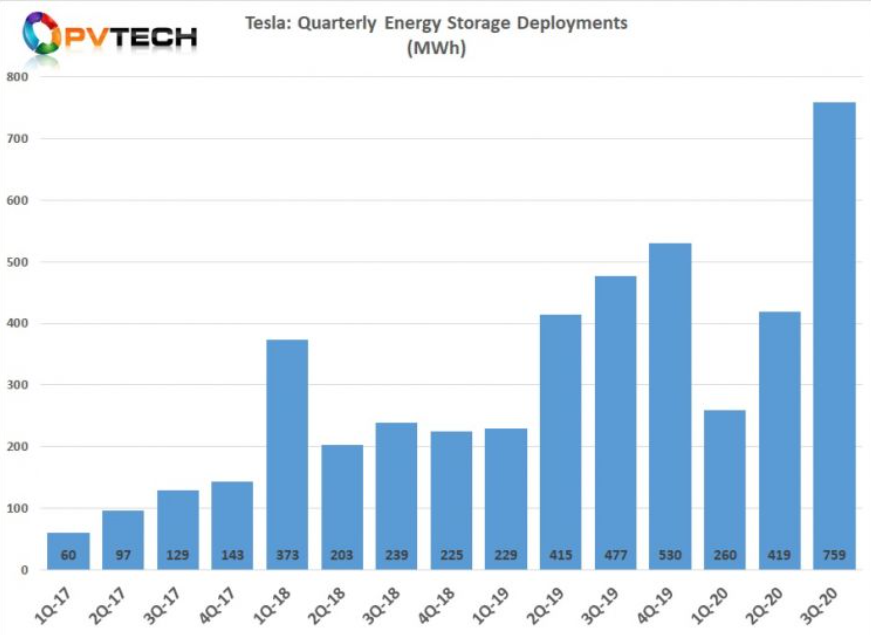

- Quarterly Energy Storage Deployments (historical growth through 2025 record)

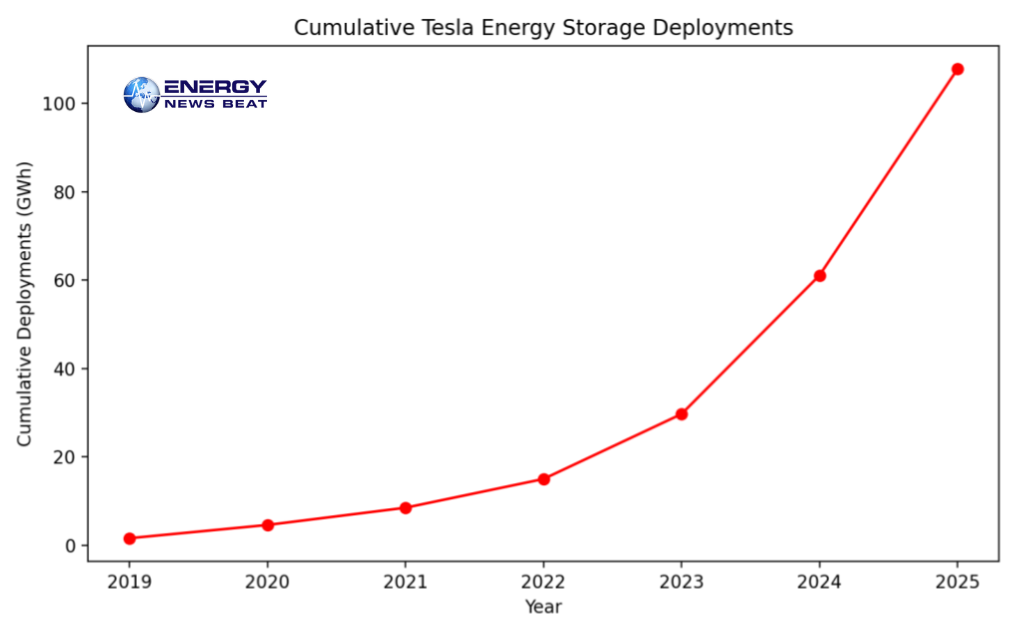

- Cumulative Tesla Energy Storage Deployments 2019–2025 (showing explosive scaling)

- Tesla Megapack deployment sites (Lathrop, Houston-area visuals)

Major Announcements

- Q4 2025 & FY 2025 Results (Jan 2026): Record 46.7 GWh deployed, $12.8B energy revenue.

- Houston Megapack 3 factory (50 GWh/year target, late 2026 start).

- LG Energy Solution $4.3B U.S. LFP plant (Michigan, ~2027).

- Nevada LFP cell production ramp (early 2026).

- Megapack 3 + Megablock launch (faster installs, higher density).

All Sources

- Bloomberg: “Tesla’s Battery Business, a Quiet Moneymaker, Suddenly Stalls” (April 22, 2026) → https://www.bloomberg.com/news/articles/2026-04-22/tesla-s-battery-business-a-quiet-moneymaker-suddenly-stalls

- Tesla Q4 2025 Update & Earnings Materials → https://assets-ir.tesla.com/tesla-contents/IR/TSLA-Q4-2025-Update.pdf

- Energy-Storage.News & Utility Dive coverage of 2025 records and 2026 outlook.

- Tesla IR Q1 2026 Production/Deliveries (April 2, 2026).

- Benchmark Mineral Intelligence & industry reports on Tesla’s supply-chain leadership.

- Reuters, Electrek, and Tesla Accessories blog on factory expansions and LG deal.

Full links and primary documents are available on the Energy News Beat website or the Tesla Investor Relations page. Stay tuned for deeper analysis on the upcoming Q1 2026 earnings call.