In a major move to supercharge its long-term production and solidify its position in North America’s premier shale plays, oil giant Shell plc has agreed to acquire Canadian energy company ARC Resources Ltd. for a total enterprise value of approximately $16.4 billion. The all-cash-and-shares deal marks one of the largest energy transactions in Canada this year and underscores the supermajors’ continued push to bolster hydrocarbon resources amid strong global demand.

Under the terms, ARC shareholders will receive CAD 8.20 in cash plus 0.40247 ordinary shares of Shell for each ARC share held — roughly a 25% cash / 75% shares split. This values ARC’s equity at about $13.6 billion (a 20% premium to its 30-day volume-weighted average price) and brings in an additional $2.8 billion in net debt and leases. The transaction is expected to close in the second half of 2026, subject to shareholder, court, and regulatory approvals.

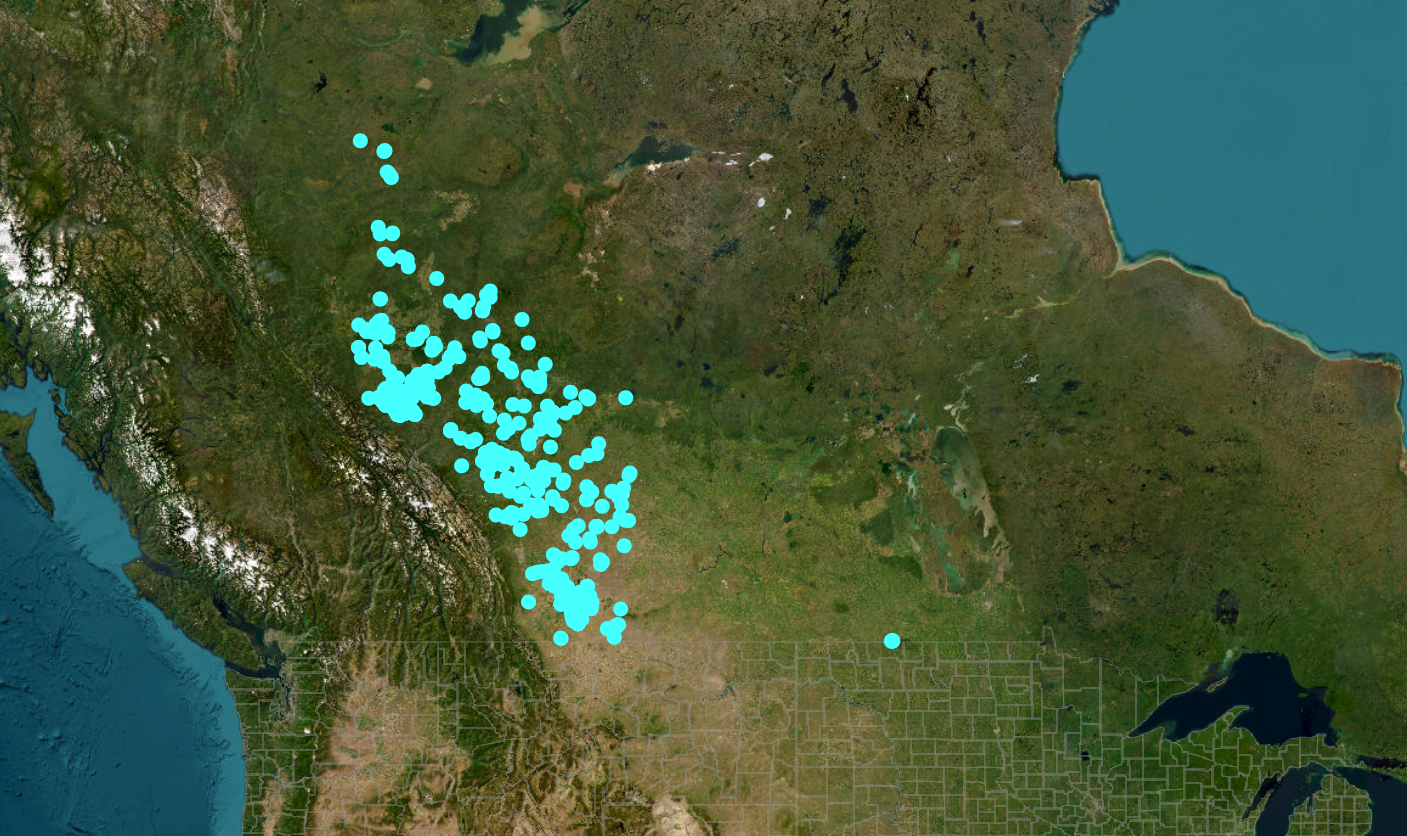

ARC’s World-Class Montney Assets: Low-Cost, High-Impact Production

ARC Resources is Canada’s largest pure-play Montney producer, with operations concentrated in the prolific Montney shale basin spanning Alberta and northeast British Columbia. The company holds more than 1.5 million net acres in the play — one of the largest contiguous land bases in the Montney fairway — which will combine with Shell’s existing ~440,000 net acres for a total footprint of nearly 2 million acres.

Key assets include:

Liquids-rich zones in Alberta (Kakwa and Ante Creek near Grande Prairie) — delivering high-value condensate and NGLs with strong economics.

Natural gas and condensate assets in northeast BC (Greater Dawson, Sunrise, Attachie, Septimus, and Sundown near Dawson Creek and Fort St. John) — strategically located with access to pipelines, third-party egress, and low-carbon hydroelectric power.

ARC’s balanced portfolio produces roughly 374,000–410,000 barrels of oil equivalent per day (boe/d), with ~40% liquids (crude oil, condensate, and NGLs) accounting for about 70% of revenues. The company operates an extensive owned-and-operated infrastructure network with ~2.0 Bcf/d of natural gas processing capacity and significant liquids handling capability, driving some of the lowest operating costs in the basin. It boasts more than 20 years of high-quality drilling inventory, with many areas featuring breakevens below C$3.00/Mcf and top-quartile low-carbon intensity thanks to efficient operations and access to clean power.

The deal immediately adds ~370,000 boe/d (post-royalty) of low-cost production to Shell’s portfolio, along with ~2 billion barrels of oil equivalent in proved-plus-probable reserves (as of end-2025).

Strategic Fit and Synergies for Shell

Shell CEO Wael Sawan called the assets “uniquely positioned,” noting they complement Shell’s existing Canadian footprint — including the Groundbirch asset in BC (which supplies gas to the LNG Canada project, where Shell holds a 40% stake) and the Gold Creek project in Alberta. The acquisition will be integrated into Shell’s leading Integrated Gas division and is expected to deliver annualized synergies of around $250 million within a year of closing.

“This establishes Canada as a heartland for Shell while furthering our strategy to deliver more value with less emissions,” Sawan said. “We are accessing uniquely positioned assets and welcoming colleagues that bring deep expertise, which, combined with Shell’s strong basin-level performance, provides a compelling proposition for shareholders.”

ARC President and CEO Terry Anderson added: “Our assets and staff will play an important role in helping Shell to further strengthen Canada’s resource landscape whilst also providing the secure energy that the world needs.”

A Clear Win for Investors

For Shell shareholders, the deal accelerates growth: it lifts Shell’s production compound annual growth rate (CAGR) from 1% (as outlined at the 2025 Capital Markets Day) to 4% through 2030 compared with 2025 levels. It helps sustain material liquids production at ~1.4 million barrels per day long-term, generates double-digit returns, and becomes accretive to free cash flow per share starting in 2027. The low-cost, long-duration resource base enhances Shell’s resilience and cash-flow visibility in a world that continues to demand reliable oil and gas.

For ARC shareholders, the 20% premium plus exposure to Shell’s global portfolio, dividend growth, and buyback program delivers immediate value and long-term upside. The transaction reflects strong confidence in the Montney’s profitability and the sector’s fundamentals.

Overall, the move signals continued capital discipline and value-accretive M&A in the upstream space — music to investors’ ears in an era of energy transition rhetoric that still requires massive hydrocarbon investment.

A Win for Consumers and Energy Security

Consumers stand to benefit from an increased, reliable supply of North American oil, natural gas, and liquids produced under some of the world’s strictest environmental and safety standards. The Montney’s low-carbon-intensity output — supported by hydroelectric access and efficient operations — helps meet growing energy demand while supporting Shell’s integrated LNG ambitions in Canada. More LNG feedstock means greater potential for exports that can displace higher-emission fuels in Asia and beyond, ultimately contributing to global emissions reduction through market forces.

By expanding production in a stable, allied jurisdiction like Canada, the deal enhances North American energy security and helps insulate consumers from geopolitical supply shocks. The result? More predictable supply chains, downward pressure on price volatility, and continued affordability for homes, vehicles, industry, and power generation.

Shell expects to fund the equity portion with $3.4 billion in cash and $10.2 billion in new shares while keeping its shareholder distribution policy (40-50% of cash flow from operations) and capital expenditure guidance intact. The company’s 2030 climate targets remain unchanged.

This acquisition is more than a deal — it’s a statement that world-class shale resources like the Montney remain vital to powering the future. Energy News Beat will continue tracking the regulatory process and integration milestones.

- CNBC Article: “Oil giant Shell to buy Canada’s ARC Resources for $16.4 billion in push to boost output” (April 27, 2026) – https://www.cnbc.com/2026/04/27/shell-arc-resources-acquisition-16-billion-energy-oil.html

- Shell Official Press Release (April 27, 2026) – https://www.shell.com/news-and-insights/newsroom/news-and-media-releases/2026/shell-announces-agreement-to-acquire-canadian-energy-company-arc-resources.html

- ARC Resources Operations Page – https://www.arcresources.com/what-we-do/our-operations/

- ARC Resources Q1 2026 Investor Presentation (PDF) – https://www.arcresources.com/wp-content/uploads/2026/02/Q1-2026-Investor-Presentation.pdf

- Additional context from Globe and Mail, StockTitan, and Enverus reports on Montney play scale and economics (various 2024–2026 dates).

All data and quotes sourced directly from company releases and the referenced CNBC coverage as of April 27, 2026.