Europe’s ongoing quest for energy security—diversifying away from Russian supplies amid geopolitical tensions—has spotlighted the Eastern Mediterranean as a promising alternative source of natural gas. At the heart of this potential lifeline lies Israel’s Leviathan gas field, one of the region’s largest offshore discoveries. While current exports primarily flow to neighboring Egypt and Jordan (with some volumes reaching Europe indirectly via Egyptian LNG), ambitious pipeline proposals like the EastMed project could one day deliver Leviathan gas directly through Greece and into broader European markets.

As of mid-2026, upstream expansion at Leviathan is advancing rapidly, but the long-discussed pipeline route remains in a state of renewed discussions rather than active construction. This article examines the field, its operators, proposed infrastructure, gas volumes, project status, and potential investment angles.

Leviathan: A Giant in the Levantine Basin

Discovered in 2010 in the Mediterranean Sea, approximately 47 km southwest of Israel’s Tamar field, Leviathan sits in the Levantine Basin in waters about 1,700 meters deep. The field holds an estimated 635 billion cubic meters (BCM) of recoverable natural gas reserves (roughly 22.4 trillion cubic feet), making it one of the largest in the Eastern Mediterranean.

Commercial production began in December 2019. The field currently operates with a platform capacity of around 12 BCM per year. In 2025, it sold approximately 10.8–10.9 BCM, with the bulk exported to Egypt and Jordan alongside domestic Israeli supply.

In January 2026, the partners reached a Final Investment Decision (FID) on a $2.36 billion Phase 1B expansion. This includes drilling three additional offshore wells, installing new subsea infrastructure, and upgrading the production platform. The project aims to boost annual delivery capacity to approximately 21 BCM by the end of the decade (target online around 2029). The expansion is expected to support increased exports to Egypt and Jordan, with potential spillover to Europe via LNG.

Geopolitical risks remain a factor: the field was temporarily shut in for about a month in early 2026 amid regional conflicts but resumed full operations in early April 2026.

Chevron Mediterranean Limited (a Chevron subsidiary) serves as operator with a 39.66% working interest. Israeli firms hold the balance: NewMed Energy (part of the Delek Group) at 45.34% and Ratio Energies at 15%.

Chevron’s leadership has driven recent growth, including the 2026 expansion FID and parallel development of nearby assets like Israel’s Tamar field and Cyprus’s Aphrodite field (where Chevron also participates). NewMed and Ratio provide local expertise and have seen share price gains tied to expansion news.

Proposed Pipelines from the Mediterranean Through Greece

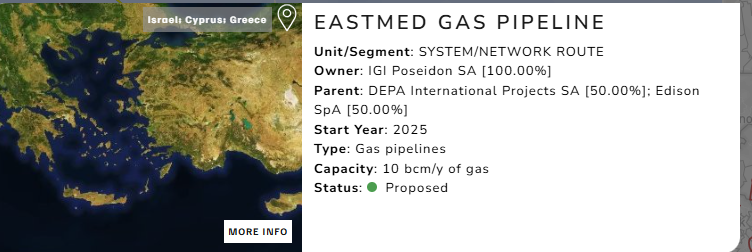

The flagship proposal for direct delivery to Europe is the EastMed (Eastern Mediterranean) Pipeline, a subsea and onshore system designed to transport gas from Leviathan and Cyprus’s Aphrodite field to mainland Greece (via Cyprus and Crete), then onward via the Poseidon pipeline to Italy and other Southeast European markets.

Route and Specs: Approximately 1,900–2,100 km long, with sections in water depths up to 3 km. Initial capacity: 10 BCM per year (potentially expandable to 20 BCM).

Status (as of May 2026): The project holds EU Project of Common Interest (PCI) status and benefited from an intergovernmental agreement signed in 2020 by Israel, Greece, and Cyprus. Front-end engineering and design (FEED) work and environmental studies were completed years ago, but no FID has been taken. The U.S. withdrew support in 2022 over economic viability, environmental concerns, and diplomatic tensions. High costs (estimated €6–7 billion), technical challenges in ultra-deep water, and regional politics (including Turkish objections) have stalled progress.

Discussions revived in November 2025 with meetings involving energy ministers from Greece, Cyprus, Israel, and the United States. As of early 2026, the project is described as “not dead yet,” with renewed governmental commitments and exploration of complementary routes (such as shorter Cyprus–Israel links). However, no construction timeline has materialized, and commissioning estimates (once targeted for 2025–2028) remain uncertain.

In practice, Leviathan gas reaches Europe today primarily through existing pipelines to Egypt, where it is liquefied and shipped as LNG. The Leviathan partners have invested in additional export infrastructure to Egypt to support higher volumes.

Pipeline Development Companies

The EastMed project is promoted by IGI Poseidon S.A., a 50/50 joint venture between Greece’s DEPA International Projects S.A. and Italy’s Edison S.p.A. (part of the EDF Group). These entities have led feasibility work, market testing, and regulatory efforts. No other major pipeline consortia have emerged for a direct Greece-route project from Leviathan.

Gas Volumes and European Reach

Leviathan Potential: Post-expansion, ~21 BCM/year total output. Current regional exports already exceed 8 BCM annually to Egypt and Jordan combined; incremental volumes from the expansion could support additional LNG cargoes to Europe.

EastMed Design: 10 BCM/year initial (enough to meet a meaningful share of Southeast Europe’s needs if realized). Phase 2 could double this.

Europe’s diversification strategy makes any scalable Eastern Mediterranean supply strategically valuable, though LNG rerouting via Egypt currently serves as the practical bridge.

Potential Investment Opportunities

Upstream Exposure: Chevron (NYSE: CVX) offers direct, liquid exposure to Leviathan expansion and broader Eastern Mediterranean growth (including Aphrodite). The company has signaled confidence with its recent FID.

Israeli Partners: NewMed Energy (Tel Aviv-listed) and Ratio Energies provide higher-beta plays on Leviathan cash flows and potential export upside. Both reported resilience during the 2026 production pause.

Infrastructure/Pipeline Angle:

If EastMed advances, DEPA (Greek state-linked) and Edison/EDF could benefit from development contracts and long-term tariffs. However, the lack of FID makes this speculative.

Broader Themes: LNG-related infrastructure in Egypt or Cyprus, or floating LNG concepts, may capture near-term volumes before any pipeline materializes. Regional cooperation (e.g., Egypt–Israel export deals worth tens of billions) underpins steady revenue.

Risks include geopolitics, high project costs, the global energy transition, and competition from other LNG suppliers. Investors should monitor FID milestones and intergovernmental updates.

Conclusion

Leviathan’s expansion positions the Eastern Mediterranean as a more reliable supplier for regional markets today and a potential direct lifeline to Europe tomorrow. While the EastMed pipeline through Greece remains a compelling long-term vision rather than an imminent reality, the underlying gas resource and operator momentum are real. As Europe seeks non-Russian supplies, Leviathan—and the companies developing it—stand at the center of a strategically vital energy story.

Appendix: Sources and Links

All information is drawn from publicly available reports and news as of May 2026. Key references include:

- Chevron press release on Leviathan FID (Jan 16, 2026): https://www.chevron.com/newsroom/2026/q1/chevron-takes-final-investment-decision-on-leviathan-gas-expansion

- Reuters coverage of production restart and expansion: https://www.reuters.com/business/energy/chevron-takes-final-investment-decision-leviathan-gas-expansion-2026-01-16/

- Wikipedia entries on Leviathan field and EastMed pipeline (for background; cross-verified with primary sources): https://en.wikipedia.org/wiki/Leviathan_gas_field and https://en.wikipedia.org/wiki/EastMed_pipeline

- Jerusalem Post on 2025 pipeline discussions: https://www.jpost.com/israel-news/article-872979 (Nov 6, 2025)

- Global Energy Monitor and GOGEL updates on EastMed status: https://www.gem.wiki/EastMed_Gas_Pipeline and https://gogel.org/eastmed-poseidon-pipeline (updated Jan 2026)

- NewMed Energy project page: https://newmedenergy.com/operations/leviathan/

- Additional reporting from Upstream Online, MEES, OilPrice.com, and DEPA/IGI Poseidon materials.

Energy markets evolve quickly—consult professional advisors for investment decisions.