For years, net-zero advocates have pointed to Levelised Cost of Energy (LCOE) charts from Lazard, IRENA, and government reports to claim that wind and solar are now the cheapest forms of electricity. These models supposedly prove renewables beat gas, coal, or nuclear on cost. But as Energy News Beat has long argued, this narrative is built on sand. David Turver, in his powerful new Substack post “Levelised Cost of Energy Models are Junk” (published April 12, 2026), dismantles the entire framework with forensic detail. His conclusion? LCOE is not just flawed — it is actively misleading policymakers and the public. The models suffer from “garbage-in, garbage-out” syndrome, fail to compare like-for-like, rely on wildly optimistic assumptions, and completely ignore the massive system costs of intermittency. Turver is singing from the same hymn sheet as Energy News Beat and host Stu Turley. On our podcast and in our own analysis, we have repeatedly called LCOE the “Liars Cost of Energy.” We have pushed for a full-system metric — what we and others term Levelized Full System Cost of Energy (LFSCOE) or Levelized System Cost of Energy — that includes balancing, backup, storage, transmission upgrades, and grid resiliency. David’s latest piece provides the most rigorous, data-driven takedown yet. The alignment is striking, and the timing is perfect as policymakers continue to bet the farm on intermittent renewables.

Why LCOE Models Are Fundamentally Broken

Turver starts with the basics. LCOE was originally designed in the 1970s to compare dispatchable technologies — gas, coal, hydro, nuclear — that can ramp up or down to match demand. Applying the same model to weather-dependent wind and solar creates a fatal flaw: it ignores when electricity is produced. A kilowatt-hour from solar at noon on a sunny day when the grid is already oversupplied has near-zero value. A kilowatt-hour from a gas plant at 6 pm on a cold January evening when demand peaks is priceless. LCOE treats both as identical. It does not compare like with like. Even attempts to “correct” for this by adding firming costs are partial at best. Turver shows that most LCOE studies still dramatically understate the real-world expense of keeping the lights on when the wind stops blowing and the sun stops shining.

Garbage-In, Garbage-Out: The Optimistic Assumptions Exposed

The article lays bare how different organizations arrive at wildly divergent LCOE numbers — not just because of geography, but because of heroic assumptions:

Capital costs: IRENA assumes onshore wind costs just £771/kW — far below Lazard’s mid-point (>£1,500/kW) and the UK Government’s £1,693/kW. Real projects like the Sneddon wind farm that activated its CfD in 2024 came in at £1,865/kW. Solar and offshore wind show similar gaps.

Cost of capital: IRENA uses an unrealistically low 3–3.7% discount rate. Lazard and the UK Government use 7.6–8.9%. The Climate Change Committee’s 3.5% rate makes offshore wind look two-and-a-half times cheaper than recent auction results.

Load factors: IRENA, Lazard, and the UK’s 2025 Generation Cost report all assume capacity factors far higher than the UK renewables fleet actually achieved in 2024 (per Energy Trends data). Overstating generation spreads costs over more MWh and artificially lowers the per-unit price. UK solar, for example, runs at roughly 10% in reality.

Asset life: Models assume 30–38 years for wind and solar. Yet UK CfD contracts are only 20 years, after which projects must survive on market prices — often near zero when output coincides with everyone else’s.

The result? IRENA’s global averages show onshore wind at ~£25/MWh and solar at ~£32/MWh — numbers that bear no resemblance to the £72/MWh and £65/MWh strike prices won in the recent AR7a UK renewables auctions (2024 prices). Lazard’s mid-points are also too low; the UK Government report is closer to reality but still misses the bigger picture.

LCOE Comparison Across Countries: Why the Numbers Vary Wildly –

But the problem gets worse when you look across borders. Different nations’ LCOE figures for the same technologies—especially wind and solar—can differ by 200% or more. That’s not because physics changes at national borders. It’s because of wildly different assumptions on capital costs, discount rates, capacity factors, labor, permitting, and grid conditions. The result? Policymakers cherry-pick the lowest “global” or “favorable-country” numbers to justify massive renewable buildouts, while real-world auction prices and consumer bills tell a different story. As Stu Turley has hammered on the Energy News Beat podcast and in our April 1 Substack, it’s time to scrap plant-level LCOE and adopt Levelized Full System Cost of Energy (LFSCOE) that accounts for balancing, backup, storage, and transmission everywhere. Cross-country comparisons only strengthen that case.

Here’s a head-to-head look at the latest 2024–2026 data for key technologies. All figures are unsubsidized levelized costs for new utility-scale projects (in 2024–2025 USD/MWh unless noted). We pulled from IRENA’s Renewable Power Generation Costs in 2024, Lazard’s LCOE+ 2025 (U.S.-focused), UK DESNZ Electricity Generation Costs 2025, Wood Mackenzie, and supporting analyses.

|

Technology

|

Global Avg (IRENA)

|

China (lowest-cost leader)

|

India

|

U.S. (Lazard mid-range)

|

UK (DESNZ central, ~2030–2035)

|

Middle East & Africa (WoodMac)

|

Europe (higher end)

|

|---|---|---|---|---|---|---|---|

|

Onshore Wind

|

$34/MWh

|

$25–$29/MWh

|

$25–$70/MWh

|

$37–$86 (mid ~$62)

|

~$53/MWh (£41)

|

N/A

|

$50–$80+

|

|

Solar PV (utility-scale)

|

$43/MWh

|

$27–$33/MWh

|

$38/MWh

|

$38–$78 (mid ~$58)

|

~$57/MWh (£44)

|

$37/MWh (trackers)

|

$60–$118 (e.g., Japan)

|

|

Offshore Wind

|

$75–$80/MWh (Asia/Europe split)

|

Lower in Asia (~$78)

|

N/A

|

$70–$157 (mid ~$114)

|

~$77/MWh (£59 fixed)

|

N/A

|

~$80/MWh

|

Why the Massive Cross-Country Gaps?

Garbage In, Garbage Out—On Steroids

David Turver’s critique applies globally:

Capital costs & manufacturing: China’s supply-chain dominance crushes capex (solar PV installed costs ~$691/kW globally, but far lower domestically).

Cost of capital (WACC): IRENA often uses ultra-low 3–5% rates; Lazard and UK DESNZ use 7–12%. A 1% change can swing LCOE 10–20%.

Capacity factors & resource quality: Assumed 36–50% for wind in UK models vs. real 2024 UK fleet performance (often lower). China benefits from better sites.

Asset life, subsidies, and curtailment: Models assume 30+ years and ignore real-world curtailment or post-contract market exposure.

No system costs: None of these figures includes the backup, storage, transmission, or balancing required to make intermittent power reliable. Those costs vary enormously by country, higher in island grids (UK) or low-resource regions.

Result? Policymakers in Europe or the U.S. cite “China’s cheap solar” or IRENA global averages to push targets, then wonder why bills rise, and blackouts loom when the wind doesn’t blow.

The Missing Piece: Full System Costs

Even more damning, standard LCOE ignores the hidden costs that intermittency imposes on the entire grid:

Backup generation and balancing services

Transmission and distribution upgrades

Storage (batteries are expensive and limited in duration)

Curtailment and constraint payments

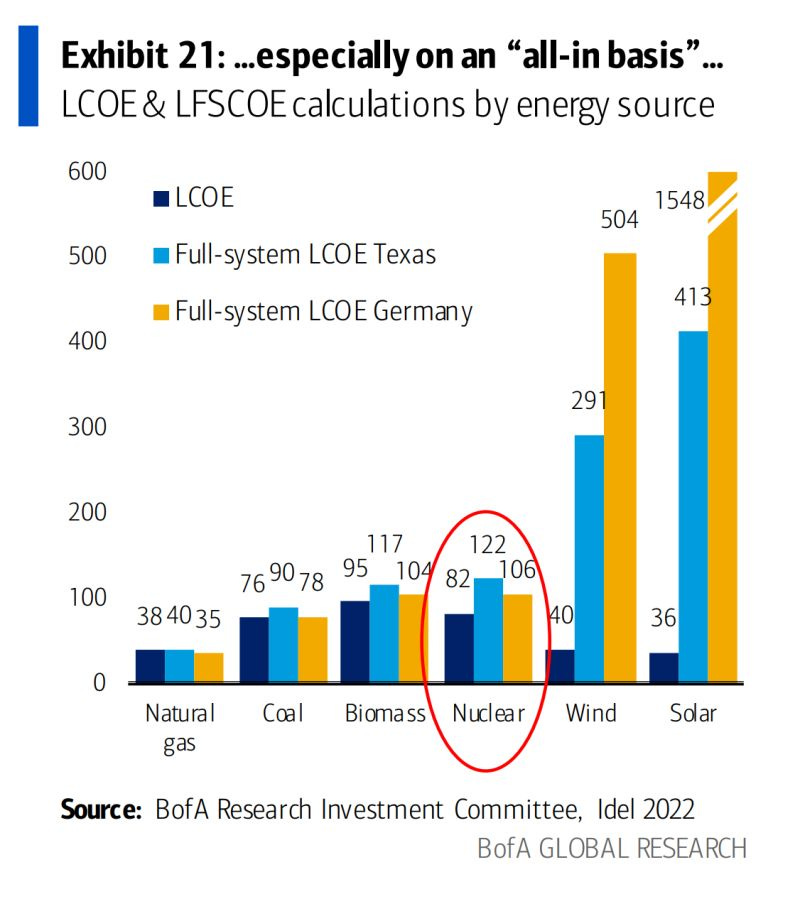

Turver estimates these integration costs alone can add ~£33/MWh or more. When you include proper firming — whether through gas peakers, long-duration storage, or overbuilding — the true system cost of renewables skyrockets. That is why David advocates shifting to a Levelised Full System Cost of Energy (LFSCOE) metric that captures the total cost to deliver reliable, dispatchable power to consumers.

This is exactly what Energy News Beat has been demanding. In our April 1, 2026, Substack post “The Redefining of Levelized Cost of Energy Needs to Be Implemented to Lower Energy Prices,” Stu Turley wrote that we must quit using the outdated LCOE and adopt a metric that reflects reality — including intermittency, integration, storage, and resiliency.

We have made the same case on the podcast, including in our October 2025 conversation with David Turver himself on “The Real Cost of Electricity to Consumers.” The message is consistent: honest accounting is the only path to affordable, reliable energy.

Why This Matters Now

Policymakers desperate to hit net-zero targets are using these flawed LCOE numbers to justify massive subsidies, contracts for difference, and grid overhauls that ultimately land on consumer bills. When the models lie, the bills rise — and energy security suffers. David Turver’s piece should be required reading in Whitehall, Brussels, and Washington. So should our own coverage. The era of pretending intermittent renewables are “cheap” on a plant-by-plant basis is over. It is time to adopt full-system costing so we can make rational decisions that actually deliver lower prices and higher reliability for families and industry.

Energy News Beat will continue to champion this fight. We thank David Turver for the detailed ammunition. The data is clear. The models are junk. It is time to redefine how we measure the true cost of energy. Stu will be reaching out to David to get him on the podcast and to go through this in detail.

Appendix: Sources Cross-Checked and Referenced

- David Turver, “Levelised Cost of Energy Models are Junk,” Eigen Values Substack, April 12, 2026 (primary source for all technical arguments above).

- Lazard LCOE Version 18.0 (2025 data).

- IRENA Renewable Power Generation Costs 2024.

- UK Government DESNZ “Generation Cost Report 2025”.

- UK CfD AR7 and AR7a auction results (strike prices and contract details).

- UK Energy Trends data (Table ET6.1) – actual 2024 renewables load factors.

- Energy News Beat Substack: “The Redefining of Levelized Cost of Energy Needs to Be Implemented to Lower Energy Prices,” April 1, 2026.

- Energy News Beat Podcast: “The Real Cost of Electricity to Consumers With David Turver,” October 2025 (direct alignment discussion).

- Additional context from Dr. Matthew Wielicki and related analyses referenced in ENB coverage.

All figures and auction results were cross-verified against official UK DESNZ and government statistical releases for accuracy. No discrepancies found with Turver’s analysis. Follow Energy News Beat for more straight-talking energy analysis, podcast episodes, and the fight for honest energy policy.