As the U.S.-imposed blockade of Iranian ports in the Strait of Hormuz enters its critical phase, global oil and LNG supply chains are in chaos. Tankers are idled, LNG prices have spiked, and energy-short nations in Asia and Europe are scrambling for alternatives. The result? Coal—reliable, abundant, and easy to stockpile—is surging back into favor faster than anyone expected.

Energy News Beat’s own reporting today highlights exactly this shift in “Coal Is Back in Play Around the World.” Countries like Japan are removing barriers to coal-fired generation, Taiwan is restarting plants, South Korea has lifted pollution caps, and India is accelerating maintenance to keep coal units online at full throttle. Europe is dusting off mothballed plants. Newcastle export thermal coal prices have jumped more than 20% in the past month to around $150 per ton, with analysts warning they could hit $200 if the blockade drags on.

In this new energy-security scramble, one American company stands out as uniquely positioned to benefit: Peabody Energy (NYSE: BTU), the nation’s largest coal producer and a major seaborne exporter out of Australia.

Forbes Spotlights Peabody’s Strategic Edge

Just weeks ago, Forbes detailed how Peabody is “behind coal’s comeback” in a story that now reads like a blueprint for the current crisis. CEO and Chairman Jim Grech—also chair of President Trump’s National Coal Council—put it bluntly: “The world, as they run into energy security problems, turns back to coal. There are no other options.”

Grech noted that customers in Japan, Korea, and Taiwan are pleading for more shipments, but Peabody’s Australian mines are already running at full capacity. “You can’t just turn on the spigot,” he said. Yet the longer the Hormuz crisis lasts, the more policymakers will recognize coal’s value as an emergency fuel that’s easy to stockpile—unlike oil or LNG tied up in geopolitical chokepoints.

Peabody’s Australian operations are the crown jewel here. The company produces high-quality seaborne thermal and metallurgical coal sold directly into the Asia-Pacific power and steel markets. Mines such as Wambo (3.5 million tons per year in JV with Glencore), the expanding Wilpinjong thermal operation (targeting a doubling to 10 million tons per year by 2030), and the ramping Centurion metallurgical mine are perfectly placed to capture the surge in Asian demand.

In the U.S., Peabody’s flagship North Antelope Rochelle Mine in Wyoming’s Powder River Basin produced roughly 80 million tons last year. While most PRB coal stays domestic, Grech sees a “domino effect” from the global crisis: as other producers divert more coal to export markets, domestic utilities will turn to Peabody’s low-cost PRB product to keep the lights on—especially with Trump administration policies supporting coal-fired generation and surging electricity demand from AI data centers.

Latest Earnings and 2026 Outlook: Built for This Moment

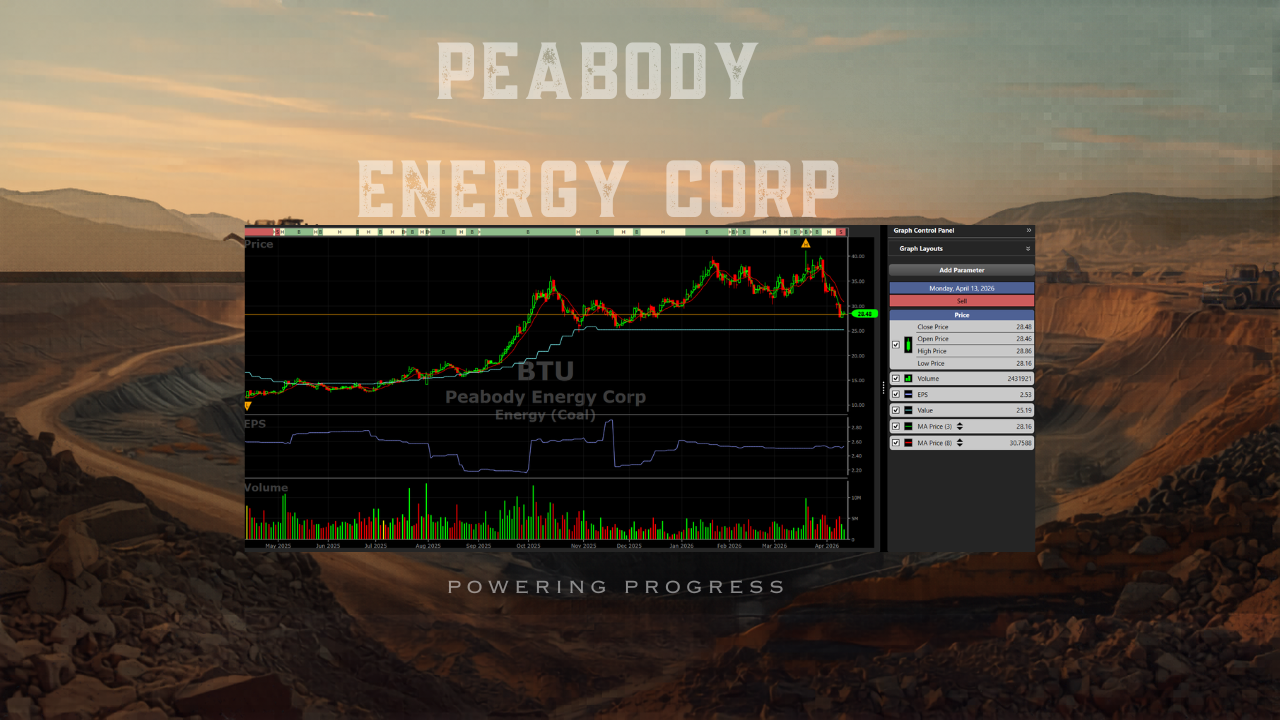

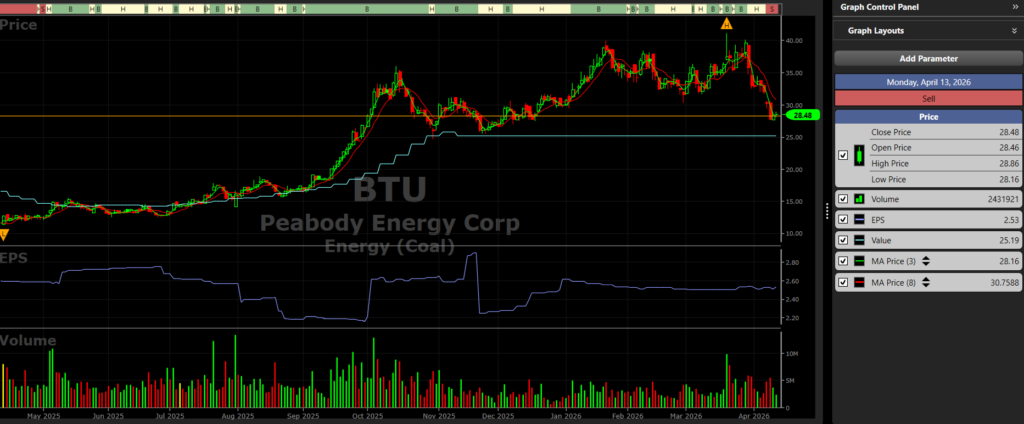

Peabody’s full-year 2025 results, released in early February 2026, showed resilience amid lower seaborne prices: revenue of approximately $3.8 billion, adjusted EBITDA of $455 million, and operating cash flow of $336 million. The company sold 122 million tons globally, with seaborne metallurgical coal at 8.6 million tons and thermal exports at 9.9 million tons.

The 2026 guidance—issued before the Hormuz escalation—already pointed higher: seaborne metallurgical coal sales targeted at 10.3–11.3 million tons (with Centurion’s longwall ramp adding premium volumes), seaborne thermal at 12–13 million tons total (7.5–8.5 million tons exported), and PRB thermal at 82–88 million tons. Costs remain competitive, and the company expects strong free-cash-flow generation with lower capex post-development. Peabody plans to return 65–100% of available free cash flow to shareholders and sits at zero net debt.

Many of Peabody’s export cargoes are unpriced, meaning rising spot prices flow straight to the bottom line. Analysts now forecast 2026 revenue north of $4.6 billion, EBITDA around $870 million, and positive EPS of $2.39—numbers that look even more attractive with today’s coal-price tailwinds.

Can Peabody Ramp Up Exports?

Yes—but with realistic timelines.Australia (the export engine): Mines are at full tilt, but expansions are already funded and underway. Wilpinjong is on track to double output by 2030; Centurion is ramping metallurgical volumes this year. Additional crews and equipment will be needed, but Grech has made clear the company is moving aggressively to meet Asian demand.

U.S. exports: Currently limited by logistics—Peabody has no direct export terminal for PRB coal today. However, the company is pursuing the Oakland terminal in California (after winning key lawsuits) and a major $700 million port project in Guaymas, Mexico, capable of handling up to 30 million tons per year. These projects could open new Pacific export lanes, but near-term upside for U.S. coal remains mostly domestic.

In short, Peabody’s Australian seaborne platform can respond fastest to the current crisis, while U.S. operations gain from the broader energy-security shift.

What Investors Should Watch

Q1 2026 earnings (due May 5): Look for realized pricing on unpriced cargoes, export volume execution, and any upward revisions to guidance.

Metallurgical coal ramp: Centurion’s contribution and premium pricing will be key margin drivers.

Free-cash-flow and shareholder returns: With zero net debt and a clear capital-return policy, dividends and buybacks could accelerate.

Rare-earth upside: Peabody is testing extraction of germanium, gallium, and other critical minerals from Wyoming seams in partnership with the Department of Energy and University of Wyoming—a potential “wild card” Grech has highlighted.

Policy tailwinds: Trump’s energy-emergency declarations and support for coal keep domestic demand robust.

Peabody’s stock has already risen 130% in the past year and more than 400% since Grech took the helm in 2021. At a forward P/E around 15, the market is pricing in growth—but the Hormuz blockade could deliver a pleasant surprise on both volume and price.

The Bottom Line

While the Strait of Hormuz blockade is a serious geopolitical and energy-security crisis for the world, it is underscoring a truth Jim Grech has been repeating: every time global supply chains falter—whether from war in Ukraine, Fukushima, or now Hormuz—the world turns back to coal. Peabody Energy, with its unmatched U.S. scale, Australian export platform, low-cost operations, and disciplined capital allocation, is structurally positioned to be one of the clearest winners.

As Energy News Beat has reported, coal is not just surviving—it is resurging as the bridge fuel the world keeps coming back to when it needs reliability most. For Peabody shareholders, that reality could translate into stronger earnings, higher cash returns, and renewed recognition of American coal’s strategic importance.

Here is a complete list of primary sources referenced in the article “Peabody Energy May Be the Only Winner of the Strait of Hormuz Blockade,” including direct links to the original reporting, earnings materials, company disclosures, and operational details.Core News Articles

- Energy News Beat – “Coal Is Back in Play Around the World” (April 14, 2026)

https://energynewsbeat.co/coal/coal-is-back-in-play-around-the-world/ - Forbes – “The American Miner Peabody Energy Behind Coal’s Comeback” (April 3, 2026)

https://www.forbes.com/sites/christopherhelman/2026/04/03/the-american-miner-peabody-energy-behind-coals-comeback/

Peabody Energy Official Earnings & Guidance

- Peabody Reports Results for the Quarter and Year Ended December 31, 2025 (Full-Year 2025 Results & Q4 2025) – Press Release (Feb 5, 2026)

https://www.prnewswire.com/news-releases/peabody-reports-results-for-the-quarter-and-year-ended-december-31-2025-302679605.html - Peabody Energy Investor Center (Q4 & Full-Year 2025 Earnings Conference Call replay, presentations, 2026 guidance, and latest filings)

https://www.peabodyenergy.com/Investor-Info/Investor-Center

Operational & Export Ramp Details (Australia Platform)

- Centurion Mine (Metallurgical coal longwall ramp – key 2026 export growth driver)

https://www.peabodyenergy.com/Operations/Australia-Mining/Queensland-Mining/Centurion-Mine - Wilpinjong Mine (Thermal coal expansion plans targeting doubling of output)

https://www.peabodyenergy.com/Operations/Australia-Mining/New-South-Wales-Mining/Wilpinjong-Mine

Additional Investor Resources

- Peabody Energy Presentations (includes 2026 guidance, capital allocation, and shareholder return framework)

https://www.peabodyenergy.com/Investor-Info/Shareholder-Information/Presentations - Peabody Energy 2025 Annual Report (10-K)

Available via the Investor Center above.

These links provide full transparency to the data, CEO commentary from the earnings call, volume and cost guidance for 2026, and operational updates on seaborne thermal and metallurgical coal export capacity. All materials are current as of April 2026 and directly support the analysis in the article.