The United States has stepped into an extraordinary role amid the 2026 Iran conflict and disruptions in the Strait of Hormuz: the world’s primary swing supplier of crude oil and refined products. Record exports are helping offset massive global supply shortfalls, but this “filling station” status comes with clear limits—depleting strategic reserves, tightening domestic inventories, and already-elevated costs for American consumers.

As energy markets grapple with one of the largest geopolitical supply disruptions in history, the question is no longer if the US can help, but how long it can sustain this pace without significant trade-offs at home.

The Export Surge: Filling the Global Gap

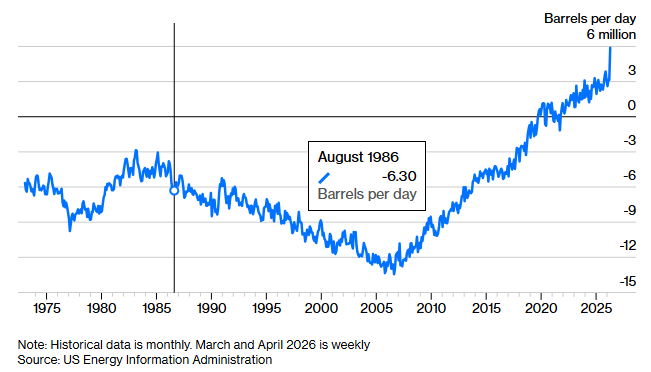

The scale of US exports is staggering. According to recent data highlighted in a May 13, 2026, Bloomberg Opinion column by Javier Blas (“Iran War: How Long Can US Oil Exports Keep Oil Prices Low?”), US net exports of crude and refined products averaged a record 5.9 million barrels per day over the prior four weeks—up sharply from 3.3 million barrels per day a year earlier. Just a decade ago, the US was a net importer of more than 5 million barrels per day.

More recent EIA data for the week ending May 8, 2026, showed US crude exports reaching 5.49 million barrels per day, with strong product exports (including gasoline and diesel) also hitting elevated levels. Total US petroleum exports (crude + products) have repeatedly set records in 2026 as buyers in Asia and Europe scramble for alternatives to disrupted Middle East supply.

This surge aligns with the broader context of the Iran-related conflict, which has effectively constrained flows through the Strait of Hormuz and idled significant production. The US shale sector’s flexibility and existing infrastructure have allowed it to ramp up deliveries rapidly—acting, in Blas’s analogy, like the “Federal Reserve of oil.” Unlike the Fed printing dollars, however, drillers cannot instantly create new barrels. New shale production involves drilling, completion, and infrastructure lags measured in months.

SPR Drawdowns: A Strategic Reserve Under Pressure

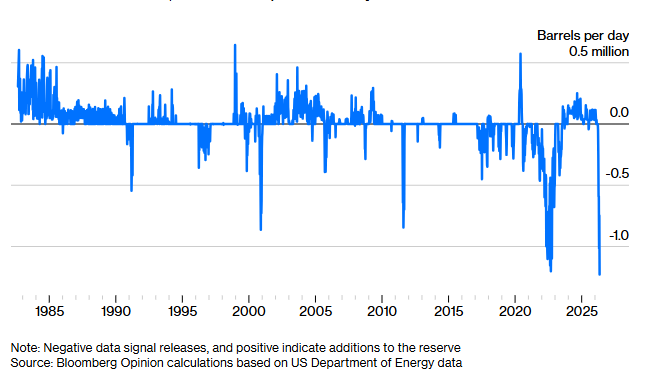

The Strategic Petroleum Reserve (SPR) tells a parallel story of rapid depletion. At the end of 2025, SPR inventories stood at approximately 411 million barrels. By early May 2026, levels had fallen to around 384 million barrels—roughly 54% of the roughly 714 million barrel authorized capacity.

In March 2026, the Trump administration authorized the release of 172 million barrels from the SPR as part of a coordinated International Energy Agency (IEA) effort to ease price spikes caused by the conflict. Deliveries were slated to occur over approximately 120 days.

However, actual drawdowns have been even more aggressive in recent weeks. Reports indicate multiple record weekly declines, including drops exceeding 8 million barrels in single weeks, with some analyses citing historic SPR releases amid high prices and market tightness. Commercial crude inventories (excluding SPR) have also drawn sharply, falling 4.3 million barrels to 452.9 million barrels in the week ending May 8, with further notable declines reported subsequently.

At current draw rates, continued heavy releases risk pushing the SPR toward levels not seen in decades, raising legitimate questions about its readiness for a true, prolonged national emergency.

When Do Massive Exports Start Hurting US Consumers?US consumers are already feeling the impact through higher fuel prices, even as producers and exporters benefit.

National average regular gasoline prices have climbed to the $4.45–$4.50 per gallon range in mid-May 2026 (with diesel significantly higher, around $5.60/gallon in recent readings). These are multi-year highs, driven primarily by the global crude price spike passing through to the pump.

The export boom contributes to this dynamic in two ways:

Product exports (gasoline, diesel, etc.) have surged alongside crude, tightening domestic product inventories. Gasoline stocks, in particular, have drawn notably in recent EIA reports.

High refinery utilization (often above 90%), combined with strong overseas demand for US products, leaves less buffer for domestic summer driving season needs.

Producers win from elevated prices and export volumes. Shale operators, midstream companies, and exporters capture strong margins. Consumers and downstream businesses lose through higher driving, trucking, and logistics costs that feed into broader inflation.

The tipping point for more acute consumer pain is approaching or already here:Current stage (prices): Higher costs at the pump and in goods transport are real and measurable.

Near-term risk (inventories): If commercial product stocks (especially gasoline and distillates) continue drawing into summer, localized tightness or price spikes could intensify.

Strategic risk (SPR + exports): Sustained high exports without corresponding production growth or reserve replenishment could force difficult policy choices—such as debates over temporary export measures or accelerated SPR refills—if a genuine supply crisis hits US shores.

Analysts note that while the US benefits enormously from its net-exporter status (producers gain when prices rise), the pass-through to consumers via global pricing means Americans still feel the pain of international disruptions.

Limits to the “Filling Station” Model

The US cannot be an unlimited global oil supplier for several structural reasons:

Production response lags — Shale growth requires sustained high prices and drilling activity; it is not instantaneous.

Infrastructure and logistics ceilings — Port capacity, tanker availability, and pipeline constraints limit how much more can realistically be exported in the short term.

Reserve depletion — The SPR is a finite buffer, not a permanent production source.

Domestic political economy — Sustained high consumer fuel prices create pressure for policy responses.

As Blas correctly observed, the analogy to the Federal Reserve has limits. The US has provided critical relief to global markets, but this role has physical, economic, and political boundaries.

Bottom Line

The United States has demonstrated remarkable energy abundance and export capability in 2026, stepping up as the global oil filling station during a major supply crisis. Record exports and a willingness to draw on the SPR have helped moderate what could have been even worse price spikes worldwide.

However, this model is not infinitely sustainable. SPR levels are declining rapidly, commercial inventories are tightening, and American drivers and businesses are already paying noticeably higher prices at the pump. The longer Middle East disruptions persist, the sooner the US will confront harder choices between maximizing exports, protecting domestic supply buffers, and managing consumer costs.

US energy dominance remains a powerful strategic asset—but it requires prudent management of reserves, continued investment in production, and clear-eyed recognition that even the world’s most flexible oil supplier has limits.

How long can it continue? Probably through the current crisis cycle with manageable strain. Indefinitely at this intensity? Unlikely without trade-offs that will increasingly be felt by US consumers and reserve readiness.

- Bloomberg Opinion (Javier Blas): “Iran War: How Long Can US Oil Exports Keep Oil Prices Low?” (May 13, 2026) — https://www.bloomberg.com/opinion/articles/2026-05-13/iran-war-how-long-can-us-oil-exports-keep-oil-prices-low

- EIA Weekly Petroleum Status Report (data for week ending May 8, 2026, released May 13, 2026) — https://www.eia.gov/petroleum/supply/weekly/

- EIA Gasoline and Diesel Fuel Update (May 2026 readings) — https://www.eia.gov/petroleum/gasdiesel/

- US Department of Energy: Announcement on 172 million barrel SPR release (March 11, 2026) — https://www.energy.gov/articles/united-states-release-172-million-barrels-oil-strategic-petroleum-reserve

- Reuters reporting on exports, inventories, and market impacts (May 2026)

- EIA Short-Term Energy Outlook (May 2026 edition) — https://www.eia.gov/outlooks/steo/

- Additional context from tradingeconomics.com, Rigzone, and market analyses on SPR levels (~384 million barrels as of early May 2026) and commercial stock draws.

All data current as of mid-May 2026 reporting cycles. Prices and inventory levels fluctuate weekly; readers should consult latest EIA releases for updates.