With the world’s oil and gas market changing, energy security is now at the forefront of most countries’ priorities. There are two discussions going on: have we found all of the easy oil, and will oil demand go away with the renewable crowd pushing more money into wind and solar? You won’t want to miss this discussion with Dr. Tammy Nemeth, Irina Slav, David Blackmon, and Stu Turley.

It was an interesting discussion this morning.

1. The “End of Easy Oil” Debate

The hosts critically examine Shell CEO’s claim that “all cheap oil is now gone.” David Blackman argues this is a stale talking point that’s been recycled for 20+ years. He points out that shale oil in the U.S. Permian Basin is actually “easy oil” due to fully delineated fields and advanced technology. The discussion highlights how the definition of “easy oil” evolves with technological advancement.

2. International Energy Agency (IEA) Forecasts & Credibility

The IEA’s latest report predicts an oil market glut with demand rising 2 million barrels daily but supply surging 8 million barrels daily. The hosts are skeptical of the IEA’s projections, with one calling it “a fool’s game” to depend on their forecasts. They note the IEA has abandoned peak oil predictions but question their overall reliability.

3. Reserve Replacement Crisis

A critical issue: the industry has underinvested in replacement production since 2015 due to ESG pressures and the Paris Agreement. Companies are consuming reserves without adequately replacing them—like “eating seed you need to plant next year.” This threatens long-term supply security.

4. ESG & Investment Decline Impact

The hosts trace the sharp drop in oil & gas exploration capital expenditure directly to 2015 (Paris Agreement) and the rise of ESG mandates. Institutional investors discouraged new oil/gas projects, creating the current supply vulnerability.

5. Frontier & Arctic Development

Future oil must come from harder-to-access areas: West Africa, Guyana (low-cost at ~$20/barrel), the Arctic, and deeper waters. However, Western countries face contradictions—they restrict Arctic development while depending on imports. Russia and China are positioned to develop Arctic resources instead.

6. Geopolitical Chokepoints & Resource Wars

- Strait of Hormuz: Critical for global oil flow; Iran’s leverage is limited as alternatives are being developed

- Red Sea/Suez: Houthi disruptions creating workarounds

- Energy as military strategy: Historical wars (WWI, WWII) were fundamentally about energy security; modern conflicts follow the same pattern

7. U.S. Strategic Petroleum Reserve (SPR) Concerns

Cushing, Oklahoma storage is near critical lows (19 million barrels, below the 20 million structural limit). The hosts note this is why Strait of Hormuz traffic is vital—to replenish supplies before a crisis occurs.

8. Electrification Paradox

90% of businesses plan to electrify by 2035, but the discussion reveals the flaw: electricity must be generated by something. Wind and solar don’t provide 75-85% of current electricity; fossil fuels still do. The hosts criticize this as misdirected policy that ignores energy fundamentals.

9. Shale & Unconventional Oil as Long-Term Resources

U.S. shale formations (Permian, Eagle Ford, Bakken) are being treated as 100-year resources through repeated refracking cycles, recovering only ~10% per major frack job. These are becoming “manufacturing operations” with consolidation from 200 producers to ~30-40.

10. Energy Security & National Survival

The hosts emphasize that reliable, affordable energy is foundational to national security, military capability, and free societies. Without it, countries become dependent on adversaries like Russia and China.

Overall Theme: The podcast challenges mainstream narratives about peak oil and energy transition, arguing that while supply challenges are real, the solution requires continued investment in conventional energy sources—not abandoning them for unproven alternatives.

We covered Enhanced Recovery Techniques.

Enhanced Recovery Techniques in Oil and Gas: The Game Changer for a Global Energy Security Renaissance

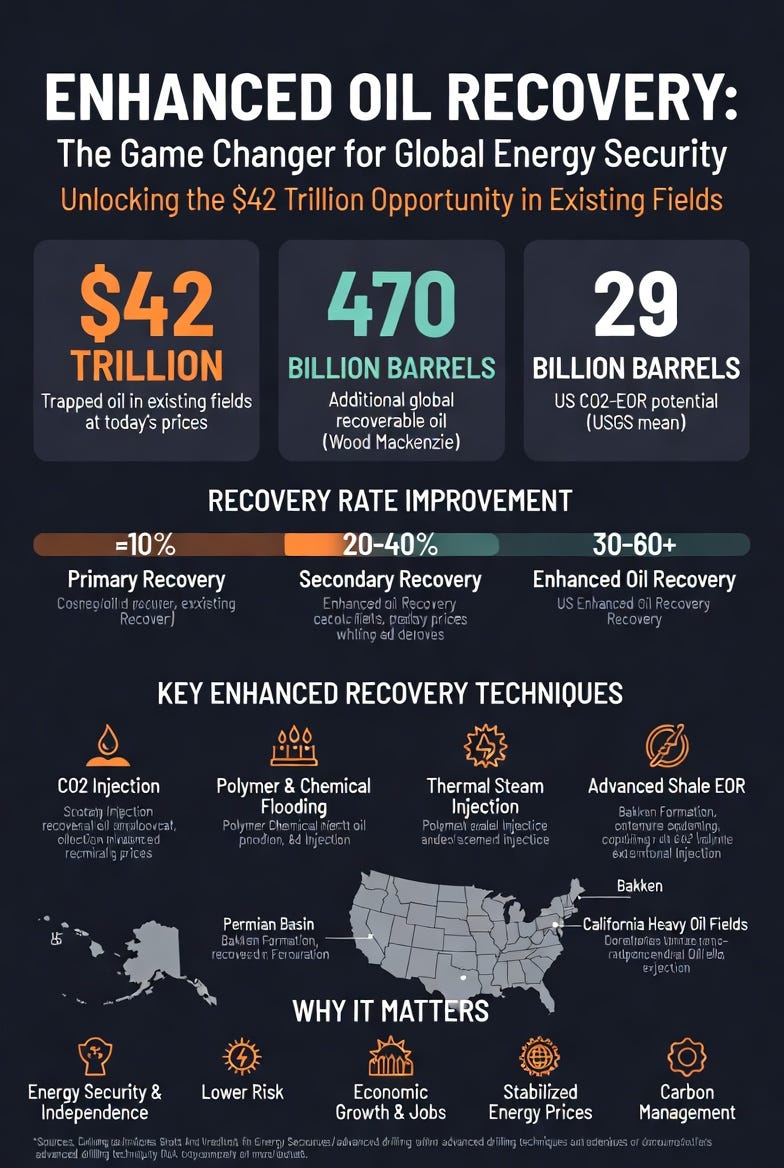

In an era of geopolitical uncertainty, maturing conventional fields, and rising global energy demand, the oil and gas industry stands at the threshold of a profound renaissance in energy security. The key? Enhanced recovery techniques—often called tertiary or enhanced oil recovery (EOR)—that unlock vast volumes of oil already discovered but left behind in existing reservoirs. These methods are not about chasing risky new frontiers; they are about maximizing what we already have, using proven technologies on mature infrastructure. As one recent analysis put it, without discovering another barrel, there is more than $42 trillion in crude oil trapped in existing fields at today’s prices, just waiting for advanced technology.

The Scale of the Opportunity

Traditional primary recovery (natural pressure and pumps) typically extracts only about 10% of the original oil in place (OOIP). Secondary methods like waterflooding or basic gas injection push that to 20–40%. EOR techniques can raise total recovery to 30–60% or more, depending on the reservoir and method.

Wood Mackenzie’s AI-powered analysis of global fields shows that improving recovery factors from the current industry average of ~29% to top-quartile performance could unlock an additional 470 billion barrels (with potential up to over 1 trillion barrels) from existing assets alone.

This is equivalent to decades of global supply without major new exploration. It directly addresses a looming production gap: 30 major oil and gas companies face a combined shortfall of ~22 million barrels of oil equivalent per day by 2040—roughly the output of two new Permian Basins.

Key Enhanced Recovery Techniques

Modern EOR goes far beyond basic waterflooding:

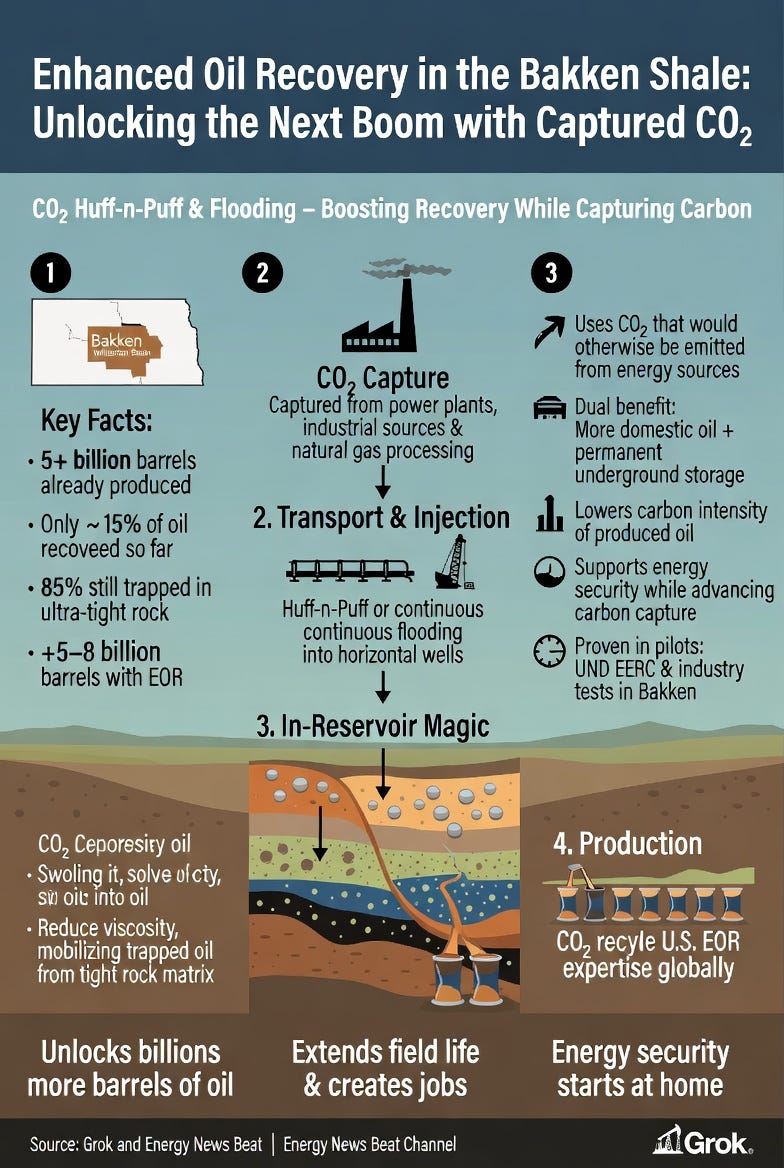

Gas Injection (especially CO₂-EOR): The dominant U.S. method (~60% of EOR production). CO₂ mixes with or swells the oil, reducing viscosity and mobilizing trapped hydrocarbons. It often pairs with carbon capture, utilization, and storage (CCUS), turning a climate solution into an economic driver.

Polymer Flooding & Chemical EOR: Polymers thicken injected water for better sweep efficiency; surfactants and other chemicals alter rock-fluid interactions.

Thermal Recovery (Steam Injection): Heats heavy, viscous oil to make it flow. Accounts for over 40% of U.S. EOR, especially in California.

Emerging Shale Applications: New approaches like surfactant-enhanced CO₂ “huff-and-puff” or advanced chemical methods target the low recovery rates (often 5–10%) typical of tight shale plays.

Hybrid & Digital-Enabled Methods: Real-time monitoring, AI-optimized injection, CHOPS (Cold Heavy Oil Production with Sand), and thermally enhanced polymers are boosting results in specific fields.

These techniques leverage existing wells, pipelines, and facilities—dramatically lowering capital intensity and timelines compared to greenfield exploration.U.S. Hotspots: Where the Renaissance Is Already UnderwayThe United States leads in many EOR applications thanks to mature fields, infrastructure, and supportive policies in key states.Permian Basin (Texas & New Mexico): The undisputed champion. CO₂-EOR has been commercial since the 1970s. The USGS 2022 national assessment estimates the technically recoverable CO₂-EOR potential across the U.S. at a mean of 29 billion barrels (range 25–32 billion), with the Permian (West Texas/Eastern New Mexico) holding ~38% of that potential.

ExxonMobil’s acquisition of Denbury brought the largest CO₂ pipeline network in the U.S. under one roof, supercharging future projects.

Bakken Formation (North Dakota): A prime emerging opportunity. Only ~15% of the resource has been tapped so far; state officials note that 85% remains trapped. North Dakota is aggressively pursuing CO₂-EOR pilots, with U.S. Department of Energy support. A second “Bakken boom” via enhanced recovery is explicitly on the table.

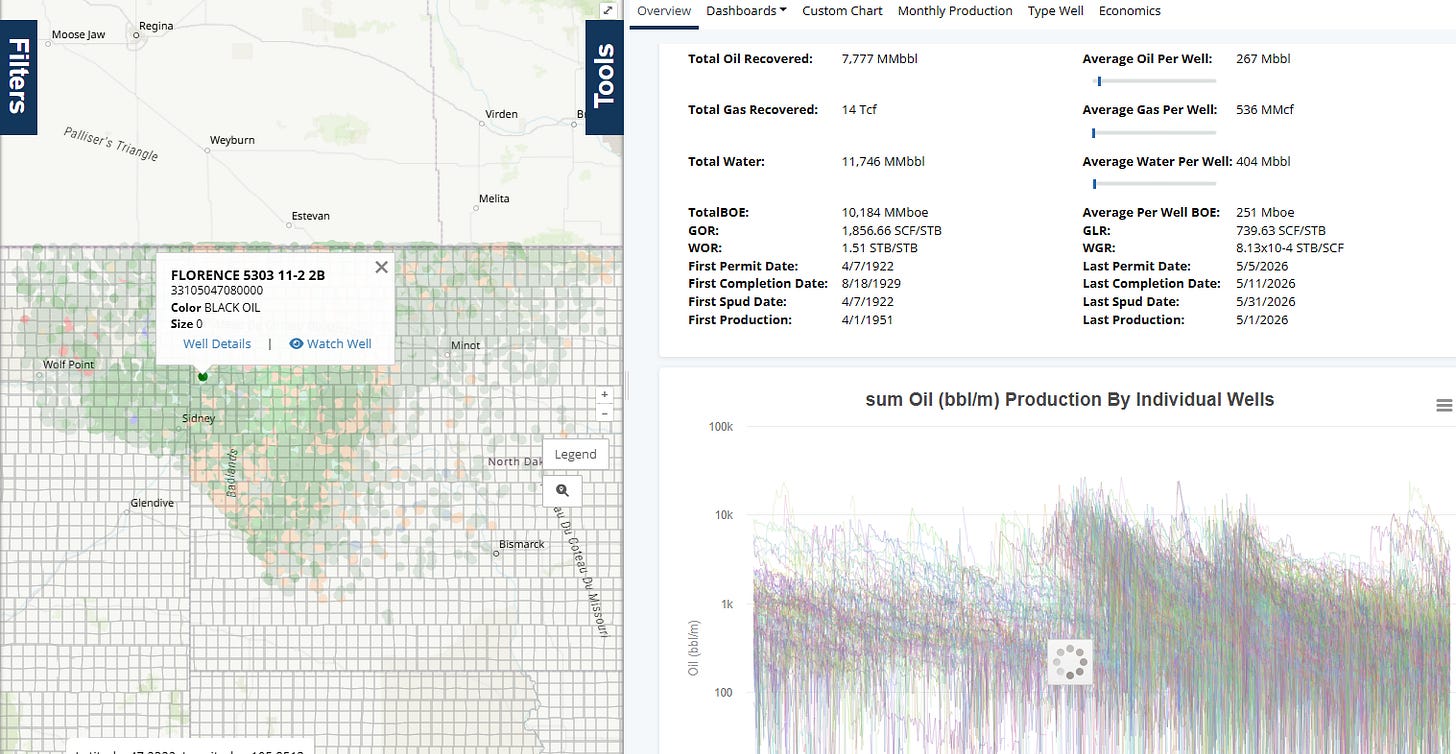

Interesting from the Bakken and welldatabase.com – 7,777 MMbbl recovered.

California: Long the leader in thermal EOR for heavy oil fields (e.g., San Joaquin Valley). Steam injection has been used commercially since the 1960s and still accounts for a huge share of national EOR output.

Other Significant Areas:

- Gulf Coast

- Midcontinent (Oklahoma, Kansas)

- Rocky Mountains and Northern Great Plains

The USGS assessment highlights these regions as having substantial CO₂-EOR upside, often in combination with carbon storage.

Investor Perspective

For investors, enhanced recovery represents lower-risk growth:

Majors and EOR specialists: Occidental Petroleum (major Permian CO₂ player), ExxonMobil (via Denbury and scale), and others with pipeline and injection expertise stand to benefit.

Service companies: Baker Hughes, Halliburton, and TechnipFMC see rising demand for polymers, digital monitoring, artificial lift, and well intervention technologies.

CCUS angle: 45Q tax credits and similar incentives make CO₂-EOR projects increasingly attractive, blending oil production with decarbonization goals.

Risks & opportunities: Oil price sensitivity remains, but existing infrastructure reduces breakeven points. Focus on companies with proven EOR track records, strong balance sheets, and exposure to federal incentives.

This is “the oil opportunity of the century”—a second boom built on assets already in the ground.

Consumer Perspective & Energy Security

For consumers, the implications are profound. Boosting domestic supply through EOR strengthens energy security by reducing reliance on imports from unstable or adversarial regions. It helps stabilize or moderate prices over time by increasing available barrels without the multi-year delays of new exploration and development.

In a world facing potential supply shortfalls, these techniques act as a powerful buffer.

Red States, Blue States, or National Imperative?

Enhanced recovery is already happening in both red and blue states, though activity is concentrated where geology, infrastructure, and policy align.Red states (Texas, North Dakota, Oklahoma, Wyoming, New Mexico) dominate current and near-term EOR growth due to pro-energy regulatory environments, existing CO₂ infrastructure, and political support. These states have led the shale revolution and are now positioned to lead the enhanced recovery renaissance.

Blue states like California already have decades of thermal EOR experience in heavy oil fields. While some blue states face stricter environmental reviews, the economic logic is powerful: higher domestic supply can ease energy costs and create jobs. CO₂-EOR’s CCUS co-benefit appeals to climate-conscious policymakers.

Will blue states “open up”? Many already have. Others may accelerate support if energy prices spike or security concerns intensify. Federal incentives (tax credits, DOE funding) and bipartisan interest in energy independence can bridge divides. Restrictive policies in some areas risk higher local energy costs and greater import dependence—the “roll down the road to higher prices” scenario.

In reality, this is not a partisan issue but a national one. Enhanced recovery benefits every American through greater supply security, economic activity in producing regions, and potential price moderation. States that embrace pragmatic, technology-driven approaches—regardless of political color—will capture the greatest advantages.

Conclusion: A Renaissance Built on What We Already Have

Enhanced drilling and recovery techniques are the quiet game changer the world needs. They transform mature fields into engines of renewed production, pair fossil energy with carbon management solutions, and deliver energy security without waiting for the next giant discovery.

The $42 trillion opportunity is hiding in plain sight—in the Permian, the Bakken, California’s heavy oil fields, and thousands of reservoirs worldwide. Investors who position themselves now, consumers who benefit from stable supply, and policymakers who prioritize pragmatism over ideology will shape the next chapter of global energy.

For David Blackmon

For Tammy Nemeth

For Irina Slav