Outright short positions in crude oil have hit record levels, according to fresh analysis from Goldman Sachs, raising the specter of a potential short squeeze if market conditions shift.

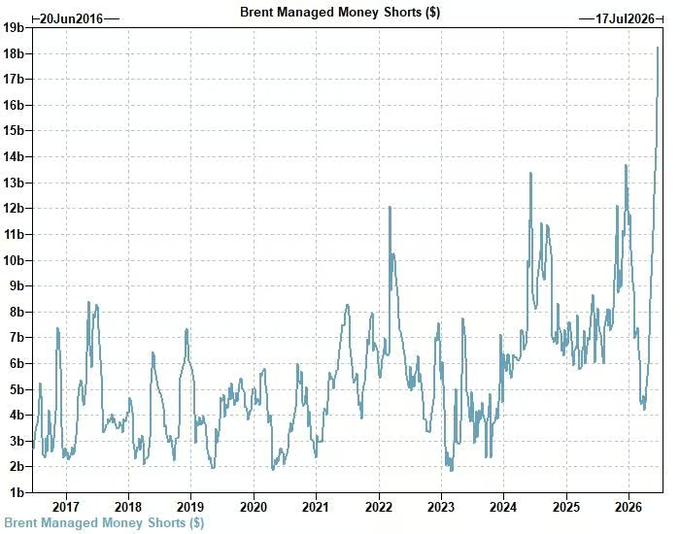

In a notable development highlighted by ZeroHedge and detailed in industry commentary, managed money accounts have aggressively built bearish exposure in Brent crude futures. Goldman Sachs’ top futures trader, Robert Quinn, reported that managed money sold roughly $7.5 billion of Brent exposure between June 9 and June 16, 2026. This extends a seven-week liquidation wave totaling approximately $24.8 billion. Critically, around 80% of the recent selling came from new outright short positions (rather than simply trimming existing longs). This has driven bearish Brent positioning to its highest level in a decade (ten-year high).

Who Is Shorting Oil?

The primary drivers are managed money participants — hedge funds, commodity trading advisors (CTAs), and other speculative investors. These players are piling into new short positions in Brent futures (primarily on ICE), betting on further price declines amid expectations of supply recovery and softer demand.

For context on WTI (NYMEX), the latest CFTC Commitments of Traders (COT) data for the week ending June 9, 2026, showed speculative traders holding a modest net long position of around 103,417 contracts, with only a slight reduction that week.

However, the most extreme short buildup appears concentrated in Brent, where positioning data (including from sources tracking ICE futures) confirms record bearish exposure among managed money.

These are not commercial hedgers (producers or consumers) but speculative/speculative-adjacent accounts taking directional bets.

Are Huge Short Sales Artificially Keeping Oil Prices Low?

This is a key question in the current environment. Brent crude has recently traded around $77–79 per barrel (as of June 22, 2026), with WTI near $73–74, down sharply from earlier 2026 peaks amid easing Middle East tensions (including developments around the US-Iran situation and Strait of Hormuz flows).

Heavy speculative short selling in futures markets can exert downward pressure on prices in the short term by increasing selling interest and influencing sentiment. When a large number of leveraged players are short, it can amplify declines or delay rebounds, as any upward move forces covering that adds buying pressure only after prices rise.

However, there is no clear evidence of artificial or manipulative suppression in the regulatory sense. Futures markets are transparent, with positions reported via CFTC (for US exchanges) and exchange data. Large short flows often reflect genuine collective bearish views on fundamentals — such as potential normalization of supply after geopolitical disruptions, inventory dynamics, or demand concerns.

Past instances of unusually large shorts timed near news events (e.g., reports of deals or de-escalation) have raised eyebrows in trading communities, but these are typically attributed to informed trading, leaks, or rapid positioning rather than proven collusion. Regulators like the CFTC monitor for manipulation, and no such findings have been reported here.

In short: The shorts are market-driven sentiment, not artificial rigging. That said, one-sided speculative positioning can create temporary distortions until fundamentals or catalysts reassert themselves.

Squeeze Risk Is Real

Goldman Sachs’ analysis flags the setup as increasingly asymmetric. While another 4–5% price drop could trigger further systematic selling (per their CTA framework), the crowded short side means any bullish catalyst — renewed geopolitical risk, stronger demand data, or persistent supply tightness — could spark rapid short covering and a sharp price spike.

Net length in crude has already fallen below pre-war (pre-2026 Middle East escalation) levels in some measures, with front-end options showing a bearish skew. History shows that extreme speculative short positioning often precedes rebounds when the crowd is too one-sided.

Bottom Line for Energy Markets

The record outright oil shorts reflect extreme bearish conviction among speculative money following recent de-escalation signals. This positioning is likely contributing to current price softness but also plants the seeds for heightened volatility ahead.

Traders and analysts should closely watch upcoming CFTC COT reports, ICE Brent positioning data, and any shifts in Middle East dynamics or inventory reports. A short squeeze remains a credible tail risk if fundamentals turn less bearish than the current crowded trade assumes.

Energy markets remain highly sensitive to geopolitics and positioning extremes — this latest development is a reminder that crowded trades often don’t end quietly.

Appendix: Sources and Links

- ZeroHedge article: “Squeeze Risk? Outright Oil Shorts Reach Record High” — https://www.zerohedge.com/energy/squeeze-risk-outright-oil-shorts-reach-record-high

- Detailed Goldman Sachs analysis summary (via Robert Quinn): “Goldman Sachs Confirms the Oil Short Is Now the Crowded Side of the Boat” — https://thedarksideoftheboom.substack.com/p/goldman-sachs-confirms-the-oil-short

- CFTC Commitments of Traders reports (latest petroleum data, week ending June 9, 2026): https://www.cftc.gov/MarketReports/CommitmentsofTraders/index.htm (Disaggregated Futures reports for Petroleum and Products)

- ICE Brent managed money positioning data reference: MacroMicro series on Brent Crude Futures & Options – Managed Money Short Position

- Current Brent and WTI price data: Trading Economics (Brent) and CME Group quotes (as of June 22, 2026)

- Broader context on positioning and energy markets: Various COT analyses from Barchart, Saxo Bank, and StoneX (historical comparisons)

All data is based on publicly available reports and market commentary as of June 22, 2026. Futures positioning can change rapidly; always verify with latest official releases.