A major shift is underway in global energy geopolitics. According to reports, ExxonMobil is close to finalizing contracts to produce oil in up to six fields across multiple regions in Venezuela, and may announce them as soon as this month.

This comes just four months after Exxon CEO Darren Woods described Venezuela as “uninvestable” under then-prevailing conditions during a January 2026 White House meeting with President Trump.

The contrast is stark — and telling. As energy analyst David Blackmon (@EnergyAbsurdity) noted on X: conditions on the ground have changed dramatically following the ouster of Nicolás Maduro, creating space for pragmatic investment in one of the world’s largest oil endowments.

From “Uninvestable” to Negotiating Table

In January 2026, Woods was clear: Exxon had suffered asset seizures twice before (notably in the 2007 Chávez-era nationalization). Re-entering required “significant changes” to legal/commercial frameworks, durable investment protections, and hydrocarbon law reforms. He emphasized the need for a technical assessment team on the ground with security guarantees.

By March 2026, Exxon was preparing to send that team. By early May, after regulatory and contractual adjustments under the new transitional government, the company was in advanced talks. The prize? Rights to develop up to six fields, likely centered on the vast Orinoco Heavy Oil Belt — home to extra-heavy crude that plays to Exxon’s technical strengths (similar to its oil sands and other complex projects).

Orinoco Heavy Oil Belt map (key area for potential Exxon activity). Venezuela holds the world’s largest proven reserves (~300 billion barrels).

No public details have emerged yet on exact equity stakes, fiscal terms, or initial production targets. However, analysts note that meaningful additions to national output could materialize within a couple of years if broader conditions hold, with Venezuela potentially adding hundreds of thousands of barrels per day (bpd) over the medium term under improved frameworks.

Chevron: The On-the-Ground Benchmark

Chevron offers the clearest real-world comparison. It is the only major U.S. company that maintained a continuous operational presence through joint ventures (JVs) with PDVSA under a special U.S. license.

Current Chevron JV output: ~260,000 bpd — roughly 25% of Venezuela’s total production.

Plans: CEO Mike Wirth has stated the company can increase its Venezuelan production by ~50% within 18–24 months using existing infrastructure.

U.S. linkage: Chevron imports the equivalent of ~250,000 bpd of Venezuelan crude on average, feeding refineries (e.g., Pascagoula) capable of processing heavy oil into diesel, gasoline, and jet fuel. Potential to scale to 350–400k bpd of throughput.

Venezuela reportedly owed Chevron about $1.5 billion as of the end of 2025. Chevron’s model — licensed JVs, on-the-ground knowledge, and direct flow of heavy crude to U.S. complex refineries — is widely viewed as the template Exxon is now pursuing.

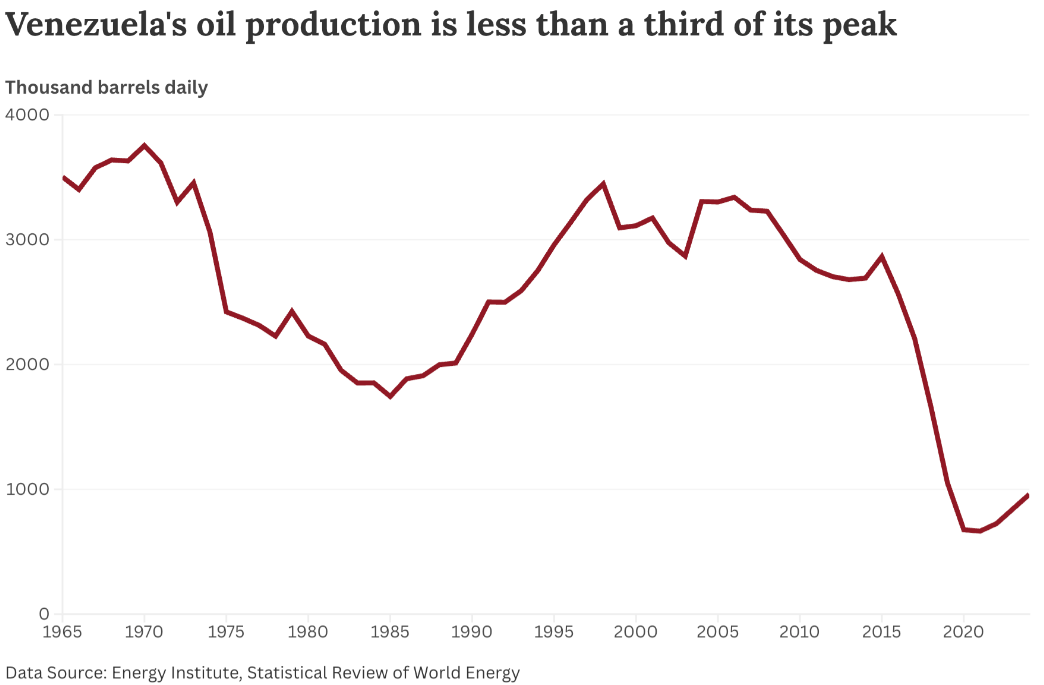

Venezuela Production: Last 5+ Years and the Recovery Trend

Venezuela’s output collapsed from peaks above 3 million bpd in the late 1990s/early 2000s due to underinvestment, mismanagement, and sanctions. The low point came around mid-2020 (~340,000–500,000 bpd).

Recent trajectory (approximate):2023: ~742,000–800,000 bpd

2024: ~890,000 bpd

2025: Approaching or exceeding 950,000–1,000,000 bpd

Early 2026 (monthly): 985,000 bpd (Mar) → 1.03–1.14 million bpd (Apr), with continued modest gains.

Venezuela’s oil production historical trend (long-term context showing the sharp post-2010s decline and early signs of stabilization/recovery). Data sources include the Energy Institute and others.

Production has been rising for several years, but the political transition since January 2026 has accelerated momentum through clearer signals on contracts, security, and foreign participation.

How Much “Better” After U.S. Involvement?

The January 2026 removal of Maduro and installation of a transitional government (with acting leadership references including Delcy Rodríguez) marked a decisive break. Key improvements cited: Opening to American companies and technical teams.

Reforms to energy regulations and contract terms.

Eased sanctions environment and push for rule-of-law/investment protections.

Explicit U.S. encouragement of major capital inflows (Trump administration referenced targets in the tens to $100+ billion range for sector revival).

Result: Exxon’s pivot from “uninvestable” in January to active deal-making by May. Production has continued its upward trend amid these shifts. Infrastructure remains degraded, and heavy-oil logistics (diluent, upgrading) are challenging, but the direction is clearly toward stabilization and foreign capital/tech deployment rather than isolation.

Implications for Investors

Positive case for Exxon (XOM): Access to world-class reserves in a heavy-oil province where Exxon has proven expertise.

Portfolio diversification and long-term growth optionality.

Potential catalyst for the stock as terms are clarified, and a footprint is re-established.

Alignment with U.S. energy dominance objectives.

Risk factors (still material):

History of expropriation — new frameworks must prove durable.

Significant upfront capex required for rehabilitation.

Execution risk on ramp-up timelines and costs.

Residual political and fiscal uncertainty in a transitional setting.

Legacy arbitration claims (Exxon has pursued ~$1.65 billion historically).

Bottom line for investors: This is pragmatic, conditions-based capitalism. Woods set a high bar in January; recent developments apparently met enough of it for Exxon to engage. Watch final contract terms closely — attractive fiscal regimes and enforceable protections will determine returns. Chevron’s experience provides a useful (cautiously optimistic) read-through.

Implications for Consumers

Near-term price impact is likely modest. Significant new volumes from Exxon’s fields will take time (likely years) to materialize at scale.

However, Supply diversification: Additional heavy crude helps balance global markets and supports complex U.S. refiners.

Energy security: Direct or indirect flows to U.S. Gulf and West Coast refineries (as Chevron demonstrates) enhance domestic product supply chains.

Longer-term price support: A successful revival reduces upside price pressure amid growing demand and geopolitical risks elsewhere. More reliable Venezuelan output is generally bullish for consumers.

Geopolitical bonus: Greater regional stability and reduced leverage for adversarial actors.

The Bottom Line

ExxonMobil’s move reflects a clear-eyed assessment: when political and legal conditions improve meaningfully, the prize in Venezuela is too large to ignore indefinitely. Chevron has already shown what a licensed, on-the-ground U.S. major can achieve. Exxon’s entry — potentially across six fields — could accelerate the recovery trajectory that began years ago but is now gaining political tailwinds.

For investors, it’s a calculated re-engagement with eyes wide open to both upside and history. For consumers, it’s incremental good news on supply diversity and long-term price stability — delivered through pragmatic energy realism rather than ideology.

The coming weeks and months will reveal the precise terms. Those details will determine just how transformative this chapter becomes.

- David Blackmon (

@EnergyAbsurdity

) X post (May 22, 2026): https://x.com/EnergyAbsurdity/status/2057802861786886263

- New York Times: “Exxon Is Nearing a Deal to Pump Oil in Venezuela” (May 21, 2026)

- Upstream Online: “ExxonMobil close to deal to return to Venezuela” (May 2026)

- ExxonMobil corporate statement (Jan 9, 2026): https://corporate.exxonmobil.com/news/news-releases/2026/our-perspective-regarding-the-situation-in-venezuela

- Reuters, CNBC, and Fortune coverage of Woods/Trump meetings and subsequent developments (Jan–May 2026)

Production Data

- CEIC Data, Trading Economics, EIA historicals, YCharts monthly series, CRS reports, and OPEC references (2020–2026 figures cited above).

- Chevron operational updates and earnings commentary (2025–2026).

Visuals & Context

- Orinoco Belt and industry maps from industry sources.

- Historical production charts compiled from the Energy Institute and public datasets.

Article prepared with real-time open-source intelligence for the Energy News Beat audience. Always verify the latest filings and contract announcements for investment decisions.