The United States is in the midst of a historic expansion of its liquefied natural gas (LNG) export infrastructure. After a decade of rapid growth that transformed the U.S. from a minor player into the world’s largest LNG exporter, a new wave of projects under construction and recently sanctioned is poised to add more than 6 Bcf/d of incremental export capacity in the near term—primarily by the end of 2026—with even larger additions planned through 2029. This buildout, concentrated along the Gulf Coast, is supported by abundant domestic natural gas supply, strong global demand, and favorable policy tailwinds.

Historical Growth: Last Five Years of US LNG Exports

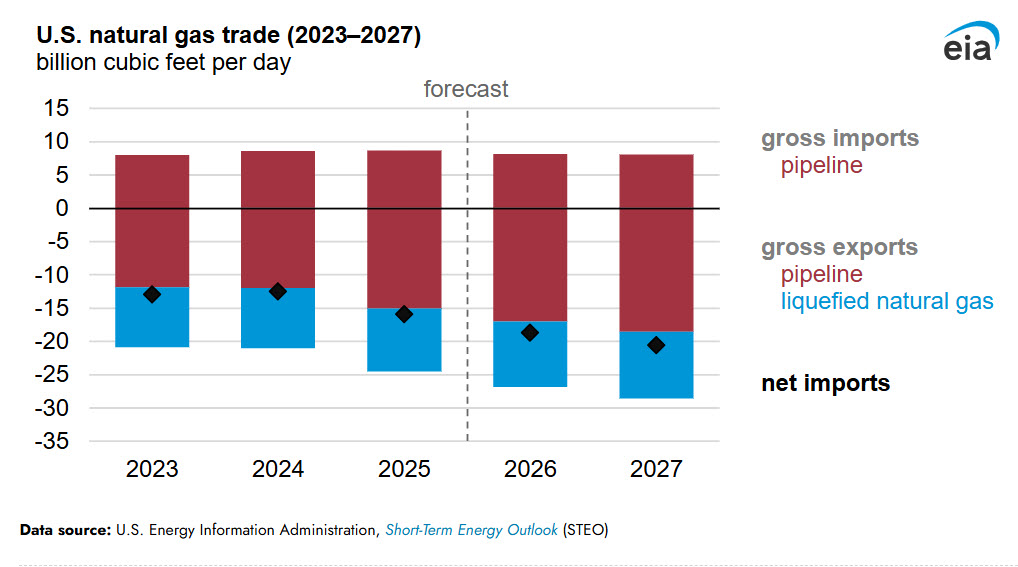

U.S. LNG exports have surged dramatically over the past five years. According to U.S. Energy Information Administration (EIA) data, average daily LNG exports grew from approximately 9.7 Bcf/d in 2021 (roughly 3.56 Tcf annually) to a record 15.0 Bcf/d in 2025 (about 5.51 Tcf). This represents compound annual growth of roughly 11-12% during the period, driven by the ramp-up of existing terminals like Cheniere’s Sabine Pass and Corpus Christi, plus new facilities such as Venture Global’s Calcasieu Pass and Plaquemines LNG Phase 1.

Key milestones in the trend: 2021: ~9.7 Bcf/d (post-initial buildout of Sabine Pass Trains 1-6 and early Corpus Christi).

2022-2023: Steady climb to ~11-12 Bcf/d amid European demand surge following Russia’s invasion of Ukraine.

2024: ~12 Bcf/d as utilization improved.

2025: Record 15.0 Bcf/d, fueled by Plaquemines Phase 1 (online late 2024) and Corpus Christi Stage 3 partial operations.

(The EIA’s historical export charts show a clear upward trajectory, with monthly volumes consistently exceeding prior-year peaks after 2021. Full data and interactive charts are available on the EIA website.)This growth has been underpinned by nameplate liquefaction capacity expanding from ~11.4 Bcf/d at the start of 2024 to roughly 15-17 Bcf/d by the end of 2025, with high utilization rates across operating facilities.

Who Is Building the New Upgrades? Key Players and Projects

The next wave is led by a mix of public and private developers, with major Gulf Coast projects reaching final investment decision (FID) or advancing construction in 2025. EIA data and industry trackers indicate approximately 9-10 Bcf/d of new capacity reached FID in 2025 alone—the highest since 2019—with several projects already contributing volumes in 2025-2026.

Major projects adding capacity (nominal Bcf/d, approximate; focused on those contributing to the >6 Bcf/d near-term wave): Venture Global LNG (private): Plaquemines LNG (Phases 1-2; 3.8 Bcf/d total design; Phase 1 full ramp in 2025, Phase 2 advancing).

Also, CP2 Phase 1 (2.0 Bcf/d, under construction) and Phase 2 FID in early 2026. Strong ramp at Plaquemines drove much of 2025’s record exports.

Cheniere Energy (NYSE: LNG): Corpus Christi Stage 3 (additional ~1.0+ Bcf/d equivalent via Trains 5-7; partial operations in 2025, full completion expected 2026). Sabine Pass expansions ongoing.

ExxonMobil (NYSE: XOM) / QatarEnergy JV: Golden Pass LNG (2.1 Bcf/d total; Train 1 achieved first LNG production March 30, 2026, with global exports starting Q2 2026).

Sempra Infrastructure (NYSE: SRE): Port Arthur LNG Phase 1 (1.6 Bcf/d, under construction; advancing with pipeline support). Phase 2 FID announced as part of 2026 value creation initiatives.

NextDecade (NASDAQ: NEXT): Rio Grande LNG (Phase 1 ~2.1-2.2 Bcf/d; Trains 1-3 under construction, first LNG expected H1 2027; Phases 4-5 advancing).

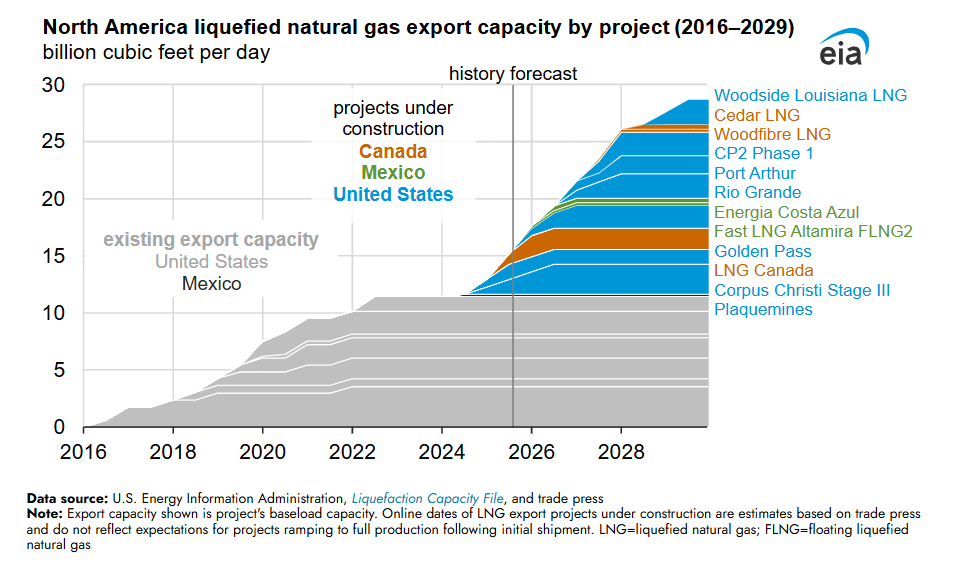

Woodside Energy: Louisiana LNG (~2.2 Bcf/d, FID 2025, under construction; online ~2029).

Additional pipeline capacity (e.g., ~6.3 Bcf/d added in 2025, with more in 2026) is being built to support feedgas delivery, targeting hubs like Gillis, LA.

Future Exports: Next Five Years Outlook

Capacity is on track to more than double. EIA projections show U.S. liquefaction capacity rising from ~15.4 Bcf/d currently to ~28.7 Bcf/d by 2029 if projects under construction proceed as planned—adding ~13.9 Bcf/d between 2025 and 2029. North American capacity (including Canada/Mexico) could reach a similar scale.

Near-term (2026): Exports forecast at 17.0 Bcf/d average (up from 15.0 in 2025), with ~2.4-6+ Bcf/d incremental from ramp-ups and new trains (Plaquemines full, Corpus Christi Stage 3 completion, Golden Pass Train 1). By end-2026, total capacity could exceed 19 Bcf/d.

Longer-term (2027-2030): Further growth to 18+ Bcf/d exports by 2027, with capacity topping 30 Bcf/d early next decade as more projects (e.g., CP2 expansions, Port Arthur Phase 2) come online. Pipeline buildout (18-20 Bcf/d potential in 2026) will be critical to avoid bottlenecks.

Global context: U.S. LNG is expected to account for over 50% of worldwide capacity additions through 2029, cementing its dominance.

Forward Statements from Publicly Traded Companies (Latest Earnings)Cheniere Energy (Q4/FY 2025 Earnings, Feb 2026): “We are introducing our financial guidance ranges for 2026 of $6.75–$7.25 billion of Consolidated Adjusted EBITDA and $4.35–$4.85 billion of Distributable Cash Flow, which reflect our previously announced LNG production forecast and include our expectation for the completion of the remaining three trains at Corpus Christi Stage 3 this year.” Production guidance: 51-53 million tons (up ~5 Mt YoY), with <1 Mt unsold open capacity. Over 95% of capacity contracted for the next decade.

ExxonMobil (Q1 2026 update, April 2026): Highlighted Golden Pass LNG milestone: “Golden Pass LNG… achieved first production of Liquefied Natural Gas (LNG) from Train 1 at its Sabine Pass terminal on March 30, 2026. This marks a significant milestone in our partnership with QatarEnergy… and increased global supply.”

Sempra (FY 2025 Results, Feb 2026): Affirmed 2026 adjusted EPS guidance of $4.80–$5.30 (and 2027 $5.10–$5.70; 2030 outlook $6.70–$7.50). Raised five-year capital plan to $65B. FID on Port Arthur LNG Phase 2 as part of value creation initiatives; simplifying business and strengthening balance sheet.

NextDecade (Q1 2026 update context): Advancing Rio Grande LNG (48 MTPA total target across phases); Q1 2026 investor call (May 1) to detail construction progress, Train 1-5 timelines, and cash flow projections from uncontracted volumes.

Conclusion

The new wave of U.S. LNG projects—adding over 6 Bcf/d in the immediate pipeline and setting the stage for capacity to nearly double by 2029—positions the U.S. for sustained export leadership. With record 2025 exports, robust contractor-backed projects, and supportive infrastructure, future volumes are poised to drive domestic gas demand, economic growth, and global energy security. Challenges like pipeline timing and market volatility remain, but the trajectory is clear: U.S. LNG is here to stay as a cornerstone of the energy transition.

All data drawn from official and reputable industry sources (as of April 2026):

- EIA Today in Energy reports and data (e.g., https://www.eia.gov/todayinenergy/detail.php?id=66384; https://www.eia.gov/todayinenergy/detail.php?id=67224; Liquefaction Capacity File).

- FERC U.S. LNG Export Terminals list (https://www.ferc.gov/media/us-lng-export-terminals-existing-approved-not-yet-built-and-proposed).

- Company earnings releases/transcripts: Cheniere (lngir.cheniere.com), ExxonMobil (investor.exxonmobil.com), Sempra (investor.sempra.com), NextDecade (investors.next-decade.com).

- Industry analysis: Natural Gas Intelligence, Reuters, ETF Trends, Incorrys, IEEFA (various 2025-2026 reports linked in search results).

- Historical export data: EIA (https://www.eia.gov/dnav/ng/hist/n9133us2m.htm; YCharts summaries).

Full links and PDFs available via the cited web sources. Data subject to ongoing project updates.