The Net Zero movement, long heralded as the inevitable path to a fossil-free future, has encountered a profound reality check. The 2026 Iran war—marked by the effective closure of the Strait of Hormuz—has triggered one of the most severe global energy crises in decades, disrupting roughly 20% of the world’s oil and significant liquefied natural gas (LNG) flows.

This geopolitical shock has exposed the fundamental weaknesses of relying heavily on intermittent wind and solar power, paired with still-limited energy storage, to maintain grid stability without reliable baseload sources like natural gas, coal, or nuclear.

Renewables excel in favorable conditions but falter when backup fuel supply chains are strained or when weather variability (such as European wind droughts) coincides with demand spikes. The crisis has driven LNG prices skyward and forced nations to confront hard truths: energy security cannot be sacrificed on the altar of rapid decarbonization. As a result, coal—affordable, dispatchable, and abundant—is experiencing a global resurgence, proving once again its role as a critical bridge and backup fuel.

Global Coal Demand: Records and Resilience

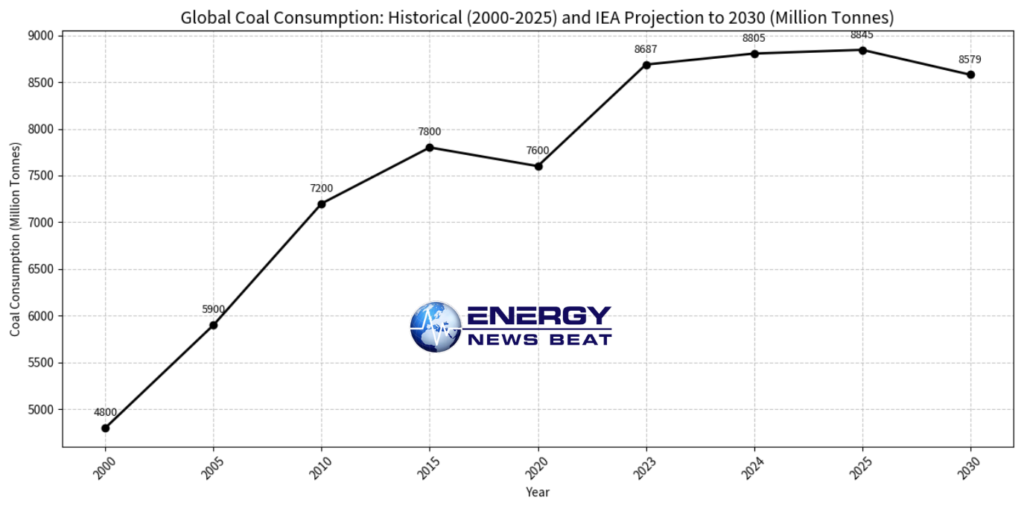

Despite years of policy pushes for phase-outs in the West, global coal consumption has continued its upward trajectory, driven overwhelmingly by Asia. According to the International Energy Agency’s (IEA) Coal 2025 report, global coal demand reached an estimated 8,805 million tonnes (Mt) in 2024 and is projected to hit a new record of 8,845 Mt in 2025. Demand is then forecast to plateau before a modest decline to approximately 8,579 Mt by 2030—still near recent highs and underscoring coal’s enduring role.

Non-power uses (e.g., chemicals, steel) are providing additional resilience even as power-sector demand stabilizes amid renewables growth.

Global Coal Consumption: Historical (2000–2025) and IEA Projection to 2030 (Million Tonnes). Data compiled from

IEA Coal 2025 report and historical trends; chart generated for illustrative purposes.

Asia Pacific dominates, accounting for the vast majority of consumption and growth. China (roughly half of global use) remains steady, while India and ASEAN nations are adding significant demand. In contrast, OECD countries continue structural declines, though even there the crisis is prompting short-term reversals.

Country Responses: Pragmatism Over Ideology

Nations are responding with urgency, prioritizing reliable power over strict timelines.

Japan is a prime example of pragmatic recalibration. Facing LNG import risks from the Middle East turmoil, Japan’s Ministry of Economy, Trade and Industry (METI) announced in March 2026 that it will temporarily suspend the 50% capacity utilization cap on older, less-efficient coal-fired plants for the fiscal year starting April 2026. This emergency measure aims to conserve LNG and ensure a stable electricity supply without new builds.

While not “opening mothballed” plants per se, the policy effectively extends the operational life and output of existing coal infrastructure that had been curtailed for climate reasons.

Germany, long a Net Zero standard-bearer, illustrates the tension between ambition and reality. The country remains committed to its coal phase-out by 2038 (with some regions targeting earlier dates) and continues post-mining reclamation efforts. A notable case is the flooding of former opencast lignite mines, such as the creation of Cottbuser Ostsee (an artificial lake from a flooded pit) and planned flooding at sites like Hambach—the latter set to begin around 2030, permanently rendering over a billion tonnes of lignite inaccessible by turning the pit into a deep lake fed by Rhine water.

Yet, even Germany is reportedly considering firing up idle coal and lignite units held in reserve to avert blackouts and curb soaring electricity prices amid the broader energy shock.

Across Asia, similar moves abound: South Korea is lifting coal caps and delaying plant retirements; Thailand is reactivating mothballed units; India is mandating full-capacity operation of coal plants through peak summer months. These actions underscore a broader trend—developing, and import-dependent economies are turning to coal for its proven reliability when gas supplies falter.

The Broader Lesson for Net Zero

The Iran war has illuminated what energy experts have long warned: modern grids require a mix of intermittent renewables and firm, dispatchable capacity. Battery storage remains too expensive and limited at scale for multi-day shortfalls, while over-reliance on imported gas exposes economies to geopolitical volatility. Coal, alongside nuclear in some cases, fills that gap affordably and immediately.

While long-term projections still envision gradual declines in coal use as renewables scale and efficiency improve, the current crisis has brought the fuel a renewed lease on life. Net Zero advocates may view this as a setback; energy realists see it as validation that pragmatic, all-of-the-above strategies are essential for both security and affordability.

Coal is not just surviving—it is back in play. One thing is certain: the world’s unrest has highlighted the Energy Security over Net Zero narrative. We are watching this play out in real time. Countries will change leadership if energy costs are too high.

- IEA Coal 2025 report (December 2025): https://www.iea.org/reports/coal-2025 and PDF at https://iea.blob.core.windows.net/assets/113a8274-500c-4684-951f-947d25bef3c9/Coal2025.pdf (global demand figures, projections, and trends).

- IEA global coal consumption chart (historical context): https://www.iea.org/data-and-statistics/charts/global-coal-consumption-2000-2025.

- Reuters on Japan’s coal policy relaxation (March 27, 2026): https://www.reuters.com/business/energy/japan-considers-increasing-coal-fired-power-war-disrupts-lng-imports-2026-03-27/.

- Politico on Germany considering coal ramp-up and lignite context (March 2026): https://www.politico.eu/article/germany-considers-ramping-up-coal-power-to-avert-energy-crisis/.

- overage of Iran war energy impacts (e.g., Strait of Hormuz, Asia responses): Atlantic Council and related reporting.

- Additional context from the Enerdata yearbook and the Our World in Data coal consumption trackers.

Energy News Beat will continue monitoring these developments as the energy security debate evolves.