Everyone was happy, sort of, except the public that bought the misbegotten shares and got wiped out?

By Wolf Richter for WOLF STREET.

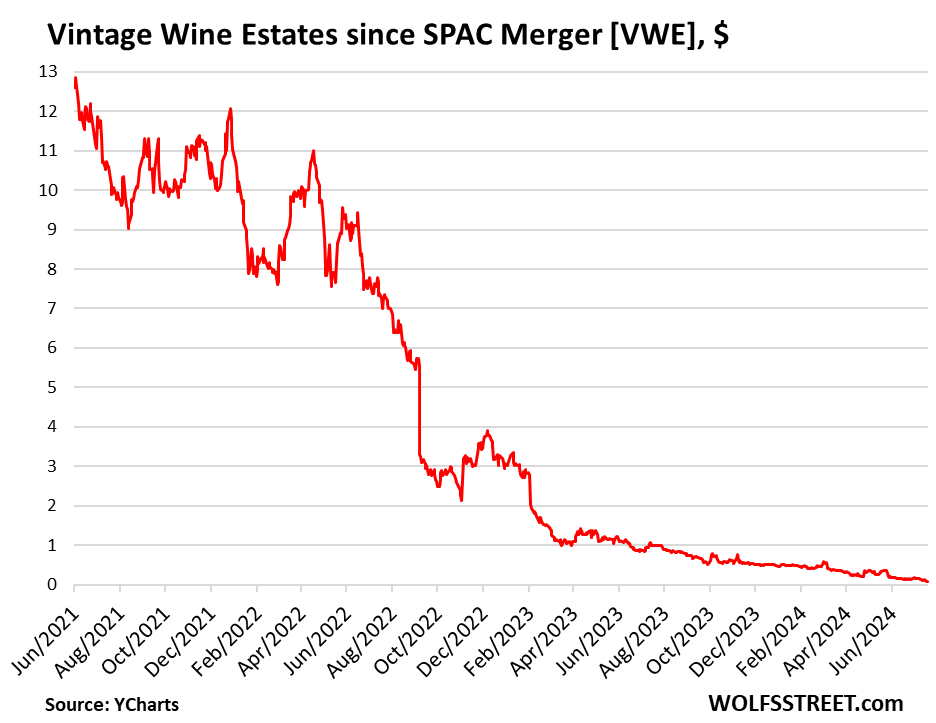

Vintage Wine Estates along with its subsidiaries – once a PE-firm-backed roll-up with about 34 brands and estates that had gone public via merger with a SPAC in June 2021 at a $690 million valuation, and a market capitalization on its third day of trading of $776 million – has now filed for Chapter 11 bankruptcy. It took three years and one month from the SPAC merger.

The company is said to be the 15th largest wine producer in the US with 2 million cases a year spread across its brands. At its peak year, in 2022, the company had $294 million in revenues. The wine brands will come out of this bankruptcy process under different ownership. The public shareholders are just out of luck.

In September 2022, by which time the shares had already lost over half their value, just 15 months after the SPAC merger, the company reported a surprise $27-million operating loss for the quarter, including a $19-million inventory adjustment, topped off by a skimpy forecast. Its shares [VWE] kathoomphed 40% on the spot.

Layoffs started in 2023. By June 2023, just two years after the SPAC merger, shares traded below $1. Today, they’re at $0.07.

SPACs have been falling like flies since 2022, as one of the greatest Wall Street scams – the SPAC bubble – imploded. They’re now densely crowded on the cheap floor of our pantheon of Imploded Stocks. It was an easy way during the crazy times of free money to dump shares into the lap of the public at ridiculous valuations without the disclosure requirements of a classic IPO.

The way it worked: An already publicly traded Special Purpose Acquisition Company (SPAC), a blank-check company with a cash balance and nothing else, merged with a target company, such as Vintage Wine Estates, which thereby became publicly traded. And what the public got with Vintage Wine Estates was this (data via YCharts):

As of its last quarterly financial statement through March 31, 2024, the company had $352 million in short and long-term debt, the result of the debt-funded roll-up of other wineries. Revenues in the quarter collapsed by 35% year-over-year. Why do companies go bankrupt? Because they have too much debt. Something goes wrong, and then the debt can kill them.

The company could no longer service its debt. In early May 2024, it was able to extend the forbearance period on its debt to June 4. The lender group also agreed to defer the $10 million principal payment that was due on May 15, to June 17. And then it ran out of wriggle room.

As part of the bankruptcy proceedings of Vintage Wine and its subsidiaries, the company will attempt to sell its assets to “address its debt obligations,” the press release said. During that process, it “expects its commercial operations to continue largely business-as-usual and is committed to serving a diverse range of customers during the Chapter 11 Cases.”

For funding to get it through the bankruptcy process, Vintage is seeking court approval for $60.5 million Debtor in Possession (DIP) financing.

Vintage Wine Estates was founded in 2008 when Pat Roney, owner of Girard Winery in Napa Valley, acquired, as it said, the “wine industry’s first direct-to-consumer brand,” Windsor Vineyards in Sonoma – both in the Bay Area’s Wine Country – and then went on an acquisition spree of brands and estates.

In 2018, PE firm AGR Partners led a $75 million investment in Vintage to expand the roll-up of wineries. “We are excited to partner with Pat Roney and the Vintage Wine Estates team to support their growth plans,” AGR Partners said at the time. “We look to make long-term investments to support best in class businesses with great partners; our investment in Vintage Wine Estates aligns closely with this goal.”

AGR exited the company as part of the SPAC merger in 2021, at peak valuation, likely with a massive profit. So kudos. Insiders likely also made a bunch of money as part of the SPAC merger and afterwards selling the shares. Wall Street investment banks and law firms certainly made a ton on fees. The founders of Bespoke Capital Acquisition Corp., the SPAC that merged with Vintage, also made a bunch of money. Everyone was happy, sort of, except the public that bought the misbegotten shares?

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the beer and iced-tea mug to find out how:

Would you like to be notified via email when WOLF STREET publishes a new article? Sign up here.

Take the Survey at https://survey.energynewsbeat.com/

Crude Oil, LNG, Jet Fuel price quote

ENB Top News

ENB

Energy Dashboard

ENB Podcast

ENB Substack