In a clear signal of renewed optimism for the upstream sector, Baker Hughes CEO Lorenzo Simonelli stated that investment in oil and gas production is set to rise. Disruptions from the Iran war are spurring a global push for energy security, according to the head of one of the world’s largest oilfield service providers.

Simonelli, speaking in a Bloomberg Television interview on April 24, 2026, highlighted that Baker Hughes anticipates a rebound in upstream investment in the second half of 2026 and into 2027. “Think of Latin America, also North America, Southeast Asia, Africa — the diversity of supply is there,” he noted, pointing to broad geographic opportunities as markets respond to geopolitical tensions and the drive for reliable energy supplies. He added that the Middle East activity is expected to recover post-conflict with increased remediation and intervention work once the Strait of Hormuz reopens fully.

This outlook aligns with Baker Hughes’ Q1 2026 earnings commentary, where Simonelli emphasized that while near-term challenges persist in certain regions, the conflict is reinforcing energy security as a priority—supporting “structural growth in upstream and global energy infrastructure spending.”How This Plays Out in the United States

The U.S. stands to benefit significantly from this anticipated pickup, given its position as a leading producer with vast shale resources, offshore potential, and a mature oilfield services ecosystem. The rebound could manifest in two primary investment avenues for investors: publicly traded stocks and privately owned drilling programs, each offering distinct risk-reward profiles and tax considerations.

Publicly Traded Stocks: Liquid Exposure with Shareholder Discipline

Public markets provide straightforward access to the upstream recovery through oilfield service providers and exploration & production (E&P) companies. Baker Hughes (BKR) itself is a direct beneficiary as a leading provider of drilling and production technology. Peers like Halliburton (HAL) and SLB are similarly positioned to see increased demand for services.

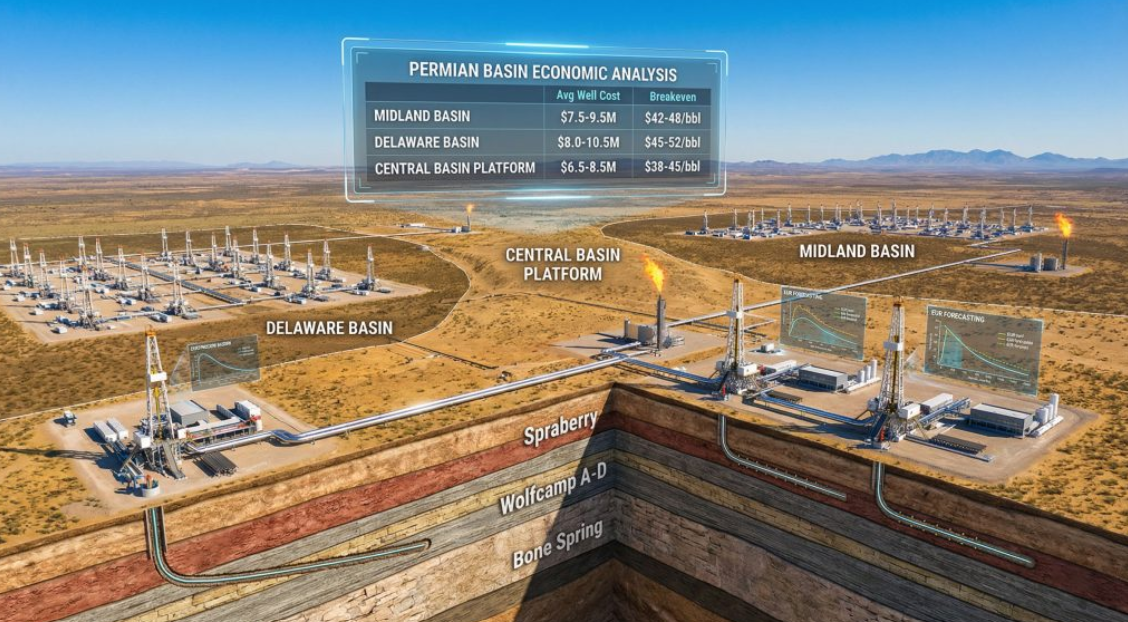

On the upstream side, majors such as ExxonMobil (XOM) and Chevron (CVX) are well-placed with diversified portfolios, including North American shale and international exposure. Smaller shale-focused players in the Permian Basin (e.g., SM Energy) could also gain as higher prices encourage selective drilling. Recent surveys show Permian producers rethinking 2026 plans, with some adding wells amid firmer oil prices, though overall U.S. rig counts remain disciplined.

Crucially, U.S. oil companies are expected to maintain their fiscal responsibility path. For years, they have prioritized shareholder returns over aggressive volume growth. In 2025, ExxonMobil returned $32.4 billion to shareholders via dividends and buybacks on $36 billion in earnings and authorized another $20 billion in buybacks for 2026. Chevron has pursued massive repurchase programs, while many E&Ps target 40-50% of free cash flow for returns. This capital discipline—flat-to-modest capex guidance, high-return projects only, and strong balance sheets—means any upstream pickup will likely translate into sustained dividends, buybacks, and efficient production optimization rather than the boom-bust cycles of the past. North American upstream spending (ex-Middle East impacts) is currently projected as relatively flat year-over-year, setting the stage for measured growth.

Privately Owned Oil and Gas Drillers: Tax-Advantaged Direct Participation

For accredited investors seeking higher potential returns and immediate tax benefits, direct investments in privately owned drilling programs offer a compelling alternative. These working-interest participations in U.S. wells (often in the Permian, Eagle Ford, or other basins) allow for substantial upfront deductions unavailable in public equities.

Key tax advantages under current U.S. rules include: Intangible Drilling Costs (IDCs):

Typically, 60-90% (or more) of drilling costs can be deducted 100% in the year incurred against ordinary income.

Tangible Drilling Costs: The remainder is depreciated over 7 years.

Percentage Depletion Allowance: Up to 15% of gross revenue can be deducted tax-free, often even after the initial investment is recovered.

These incentives, designed to promote domestic energy production, can deliver significant first-year tax savings—potentially recouping 40-50% of the investment for high-income investors—while generating ongoing monthly cash flow from production. Risks are higher (project-specific geology and operations), but successful programs provide inflation-hedged, tangible assets with low correlation to broader markets. Investors should consult tax advisors, as eligibility depends on accredited investor status and active participation rules.

Together, these paths allow U.S. investors to capitalize on the global energy security-driven rebound while aligning with the industry’s focus on fiscal prudence.

Global Context: Where New Drilling Is Announced

The Baker Hughes outlook reflects a broader resurgence in exploration and development worldwide. High-impact exploration wells planned for 2026 are concentrated in frontier and deepwater plays, with Africa expected to lead (roughly 40% of the 37-65 planned wells), driven by the Orange Basin (Southern Africa) and Gulf of Guinea (West Africa). Latin America remains a hotspot, alongside Southeast Asia and other regions, Simonelli highlighted. Deepwater projects will dominate, targeting untapped resources to replenish declining reserves amid maturing fields.

In the U.S., activity centers on the Permian Basin (where ExxonMobil leads modest supply growth) and on new offshore opportunities in the Gulf of Mexico, including recent ultra-deepwater approvals such as BP’s Kaskida project. Announcements also include expanded permitting in areas like Kern County, California, and selective shale programs.

Overall, the combination of geopolitical drivers, disciplined capital allocation, and diverse supply sources positions the upstream sector for a measured but meaningful upturn—offering opportunities for investors attuned to both public markets and private tax-advantaged plays.

- Bloomberg Article: “Baker Hughes CEO Sees Upstream Oil and Gas Investment Picking Up” (April 24, 2026) – https://www.bloomberg.com/news/articles/2026-04-24/baker-hughes-ceo-sees-upstream-oil-and-gas-investment-picking-up

- Baker Hughes Q1 2026 Earnings Release and Conference Call Materials (April 23, 2026) – https://www.bakerhughes.com and related transcripts via Yahoo Finance/Investing.com.

- Rystad Energy & Westwood: Reports on 2026 High-Impact Exploration Wells (Africa-led activity) – worldoil.com, upstreamonline.com (January-February 2026).

- U.S. Fiscal Responsibility & Shareholder Returns: Energy News Beat analysis and company releases (ExxonMobil, Chevron 2025-2026 data).

- Tax Benefits of Oil & Gas Investments: DW Energy Group, Kingdom Exploration, and IRS Section 263(c) references (2026 updates).

- U.S. Drilling Activity: East Daley, Midland Reporter-Telegram (Permian updates, April 2026); DOI announcements on offshore leasing.

- Additional Context: Reuters CERAWeek coverage (exploration rebound), S&P Global, and Wood Mackenzie reports on 2026 wells.

- Picture from Discovery Alert https://discoveryalert.com.au/permian-basin-drilling-locations-2026-trends/

Energy News Beat provides this analysis for informational purposes only. It is not investment advice. Consult qualified financial and tax professionals before making investment decisions. All data as of April 24, 2026.