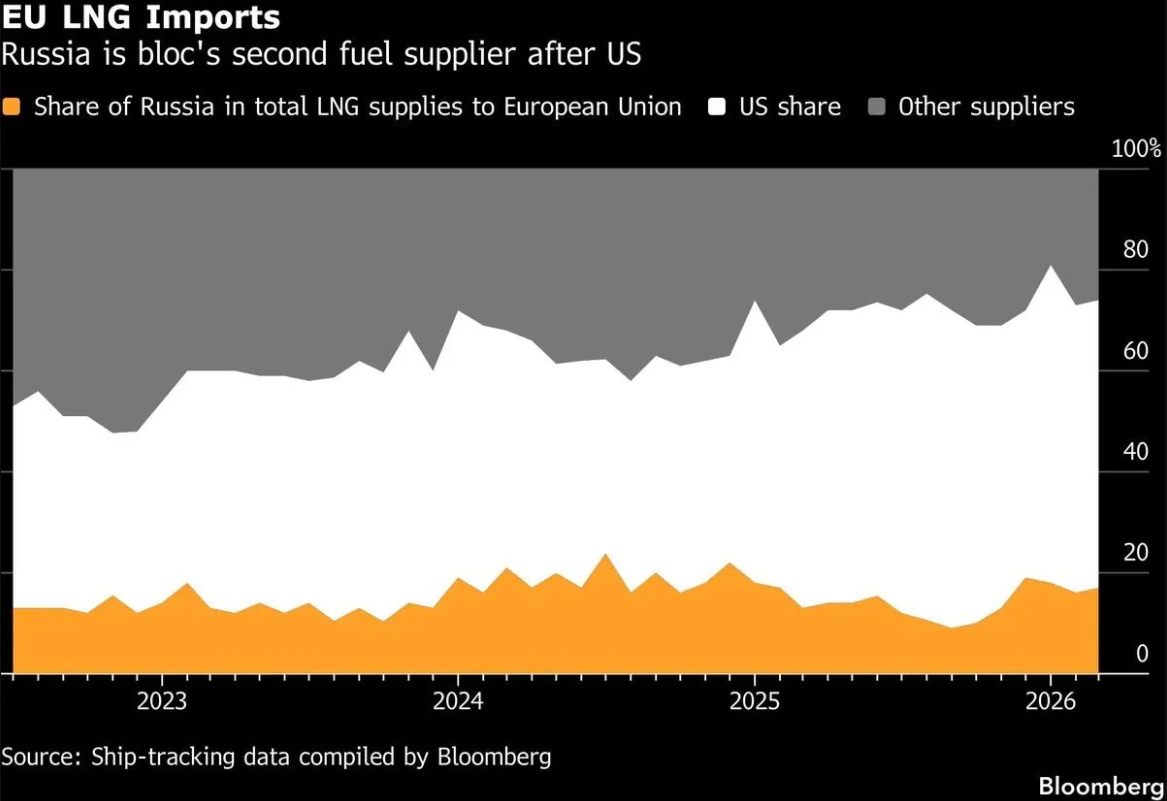

The European Union’s energy policymakers have spent years touting their “REPowerEU” strategy as a masterstroke of independence from Russian fossil fuels. Yet in March 2026—mere weeks after the EU began rolling out its formal ban on short-term Russian LNG purchases—the bloc imported more Russian liquefied natural gas than in any month on record. According to Bruegel data, EU buyers took in 2.46 billion cubic meters (about 1.78 million metric tons) of Russian LNG in March alone, a 38% jump from March 2025 and the highest monthly volume ever logged.

This isn’t a glitch. It’s the direct result of another self-inflicted wound colliding with geopolitical reality. Qatar, one of the world’s largest LNG exporters, effectively went offline in early March 2026 after Iranian attacks damaged facilities at Ras Laffan, knocking out roughly 17% of its LNG capacity (12.8 million tons per year) for three to five years. QatarEnergy declared force majeure, halting production and associated products. Global LNG markets tightened instantly, European benchmark prices surged, and the EU—already staring down storage shortfalls and winter demand—turned straight to the one flexible supplier still willing to deliver: Russia.

The Ban That Isn’t (Yet) a Ban

Brussels has legally committed to phasing out all Russian pipeline gas and LNG. The regulation adopted in January 2026 prohibits new contracts and phases out existing ones: short-term LNG spot deals are banned as of late April 2026, long-term LNG by end-2026, and pipeline gas by autumn 2027. Russian gas dependency has already dropped from 45% of EU imports pre-war to about 12% in 2025. But the transition was never going to be painless—and the Iran conflict just made it brutal.

First-quarter 2026 Russian LNG imports to the EU jumped 17% year-on-year to 5 million tons from the Yamal project alone, with the bloc snapping up 97% of all Yamal cargoes. France, Spain, and the Netherlands remain the biggest buyers. The EU spent roughly €2.9 billion ($3.1 billion) on Russian LNG in Q1 while simultaneously preaching diversification.

Qatar’s Absence Changes Everything

Qatar’s outage removes a structural chunk of global LNG supply at the worst possible moment. Europe had ramped LNG imports to record levels in 2025 (over 175 bcm) to offset the end of Russian pipeline transit via Ukraine. 2026 was supposed to see another record around 185 bcm. Instead, the market faces a deficit. U.S. LNG is filling some of the gap, but it is more expensive, involves longer shipping routes, and cannot instantly replace the lost volumes from Qatar or the chemical byproducts that come with traditional gas supply chains.

Renewables Can’t Fertilize Fields or Replace Feedstocks

Here is where EU energy dogma meets harsh chemistry. Natural gas is not just a heating or power fuel. It is the primary feedstock for ammonia production via the Haber-Bosch process—the backbone of nitrogen fertilizers that feed Europe and much of the world. Natural gas accounts for 70-90% of ammonia production costs. European fertilizer plants have already curtailed output or shut down during previous price spikes; the latest surge in TTF gas prices has triggered fresh calls for government support to keep domestic production alive.

Renewables generate electricity. They do not produce the hydrogen or the CO₂ byproduct essential to fertilizer manufacturing, methanol, plastics, or other petrochemicals. Green hydrogen via electrolysis remains expensive, energy-intensive, and nowhere near scaled for industrial replacement. The result? Higher fertilizer prices feeding into food inflation, further pressure on European agriculture and chemical industries, and accelerated “demand destruction”—a polite term for factories closing or relocating to places with cheaper, reliable energy.

What’s in Store for the EU, UK, and Broader Europe?

Short term (2026–2027): Elevated gas and electricity prices through at least the next two winters. Storage levels are already under pressure.

Industrial slowdowns and potential blackouts or forced curtailments in energy-intensive sectors.

Fertilizer shortages and higher food costs.

Billions more spent on imported LNG—much of it from the United States—while Russian volumes are still being absorbed under legacy contracts.

Medium term (2027–2030):

The EU’s AccelerateEU package calls for faster renewables rollout, grid upgrades, and demand-side measures. But the transition cannot replace the chemical role of natural gas overnight.

Deindustrialization risks are real: Germany and Italy, heavy LNG and gas users, face the sharpest exposure. The UK, outside the EU but fully integrated into European gas markets, is shifting heavily toward U.S. LNG (already over 15% of supply and projected to dominate by 2035) alongside Norwegian and declining North Sea output. London will feel the same global price pain.

Europe’s policymakers insist the answer is more solar, wind, nuclear, and efficiency. Those are necessary long-term tools. But pretending they magically solve feedstock chemistry, baseload reliability, or winter heating is the same wishful thinking that left the continent scrambling for Russian LNG in the first place.

The EU’s energy management decisions are not just costing households and factories today—they are reshaping the continent’s industrial map for a generation. When the next supply shock hits, the question won’t be whether renewables are “clean.” It will be whether they can keep the lights on, the fields fertilized, and the chemical plants running.

- High North News: “EU Buys More Arctic Russian LNG in March Than Any Month on Record” (April 2026) – https://en.highnorthnews.com/politics/eu-buys-more-arctic-russian-lng-in-march-than-any-month-on-record/1109813

- European Commission: REPowerEU – phase out of Russian energy imports – https://energy.ec.europa.eu/strategy/repowereu-phase-out-russian-energy-imports_en

- Reuters: “Iran attack damage wipes out 17% of Qatar’s LNG capacity” (March 2026) – https://www.reuters.com/business/energy/iran-attack-damage-wipes-out-17-qatars-lng-capacity-three-five-years-qatarenergy-2026-03-19/

- Financial Times reporting via multiple outlets on Q1 2026 Russian LNG surge and costs.

- Bruegel European Natural Gas Imports dataset (primary data source for volumes).

- International Food Policy Research Institute (IFPRI): “The Iran war’s impacts on global fertilizer markets” (April 2026) – https://www.ifpri.org/blog/the-iran-wars-impacts-on-global-fertilizer-markets-and-food-production/

- UK gas supply data via Sunsave Energy and National Gas Transmission updates (2026).

- Additional context from Council of the EU press releases on the Russian gas ban regulation (EU/261/2026) and European Commission “AccelerateEU” package (April 2026).

All data and analysis drawn from publicly available reporting as of April 28, 2026. Energy markets remain volatile; developments in the Middle East or winter weather could shift the picture rapidly.