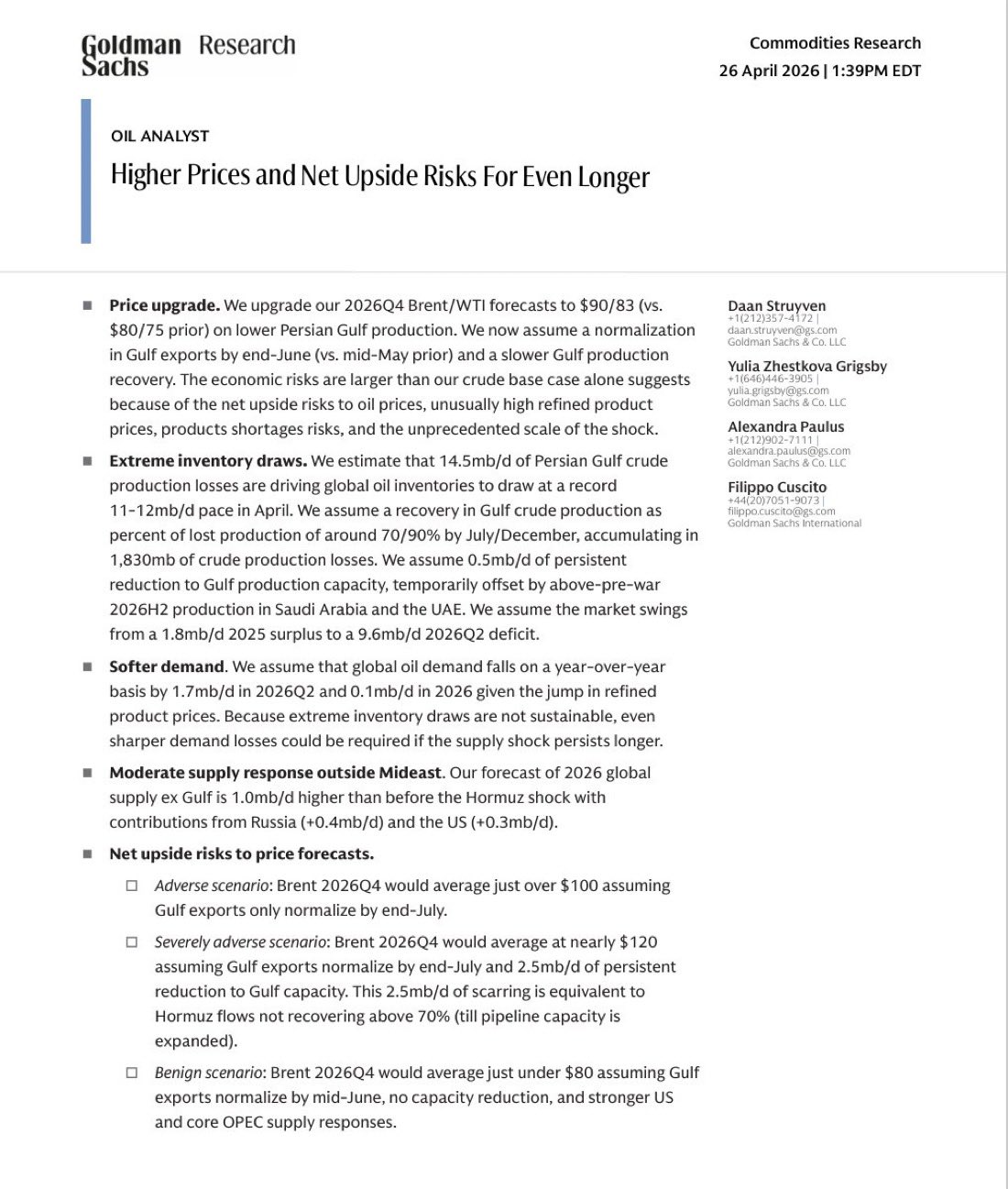

In a stark update released on April 26, 2026, Goldman Sachs has significantly raised its oil price forecasts, citing unprecedented supply disruptions in the Persian Gulf. The investment bank now expects Brent crude to average $90 per barrel and West Texas Intermediate (WTI) to hit $83 per barrel in Q4 2026—up sharply from its prior $80/$75 outlook. At the heart of the revision: a projected swing in the global oil market from a 1.8 million barrels per day (mbd) surplus in 2025 to a massive 9.6 mbd deficit in Q2 2026.

The report, authored by commodities research co-head Daan Struyven and team, highlights 14.5 mbd of Persian Gulf crude production currently offline due to ongoing geopolitical tensions and disruptions around the Strait of Hormuz. This has triggered record inventory draws of 11–12 mbd in April alone—the fastest pace since satellite tracking began.

Goldman assumes Gulf exports will normalize by the end of June (delayed from a prior mid-May view) with a slower production recovery, accumulating roughly 1.83 mbd of net crude losses by year-end after partial offsets from higher Saudi and UAE output.

Demand is also softening in response: global oil demand is forecast to fall 1.7 mbd year-over-year in Q2 2026 and by 0.1 mbd for the full year, driven by sharply higher refined product prices. Non-Mideast supply is expected to provide only a moderate response (+1.0 mbd globally ex-Gulf in 2026, including +0.4 mbd from Russia and +0.3 mbd from the U.S.).

Scenarios and Net Upside Risks

Goldman outlines clear scenarios that underscore the fragility of the current balance:

Base case ($90 Brent / $83 WTI in Q4 2026): Gulf exports normalize by the end of June with the assumed production path.

Adverse scenario: Brent averages just over $100 in Q4 if normalization slips to end-July.

Severely adverse scenario: Nearly $120 Brent if exports normalize by the end of July and there is a persistent 2.5 mbd reduction in Gulf capacity (equivalent to Hormuz flows remaining below 70% until pipeline capacity expands).

Benign scenario: Brent is just under $80 if exports normalize by mid-June, with no capacity losses and stronger-than-expected U.S. and core OPEC supply responses.

The analysts emphasize that “the economic risks are larger than our crude base case alone suggests” due to upside price risks, elevated refined product prices, shortage risks, and the unprecedented scale of the shock. Extreme inventory draws are unsustainable; prolonged disruption could force even sharper demand destruction.

What Consumers Should Look For and Look At

Rising oil prices flow straight to the pump and the household budget.

Consumers should monitor:

Gasoline and diesel prices: Expect continued upward pressure on retail fuel costs, especially as summer driving season overlaps with the Q2 deficit peak. Track local EIA or AAA weekly gasoline price reports.

Broader energy bills: Heating oil, natural gas, and electricity prices (particularly in regions reliant on oil-fired generation) could rise. Watch for knock-on effects in grocery and goods transportation costs.

Inflation signals: Energy components in CPI and PPI reports will be key. April’s energy surge (already up 10.9% month-over-month in recent prints) is just the beginning if the shock persists.

Personal hedging steps: Consider fuel-efficient vehicles, public transit, or locking in fixed-rate energy contracts where available. Budget for higher summer travel and freight-inflated goods.

What Investors Should Look At

Energy investors have a clear roadmap:

Upstream producers and oilfield services: Companies with U.S. shale, Canadian oil sands, or non-Mideast exposure stand to benefit from sustained higher prices. Watch rig counts, Permian and Bakken production data, and earnings from majors.

Refiners and midstream: Product shortages could support crack spreads, but volatility remains high.

Broader portfolio impacts: Higher oil feeds inflation, potentially delaying Federal Reserve rate cuts. Monitor Fed meeting outcomes, Treasury yields, and the dollar. Energy stocks (XLE, XOP) and commodities ETFs could outperform, while oil-sensitive sectors (airlines, consumer discretionary) face headwinds.

Key data releases: Weekly EIA inventory reports, OPEC+ monthly updates, Strait of Hormuz tanker tracking, and U.S. rig counts. Geopolitical developments around Iran and the Gulf remain the dominant wildcard.

Risk management: Position sizing matters. Goldman’s severely adverse scenario implies prices that could trigger recessionary demand destruction—watch for signs of economic slowdown that cap the upside.

Analysis: The Fallout of Higher Prices

A 9.6 mbd Q2 deficit represents a historically extreme supply shock. Short-term fallout includes accelerated inflation, particularly in energy and transport-dependent goods, which could push headline CPI higher and complicate the Fed’s path to easing. Consumers feeling the pinch at the pump may pull back on discretionary spending, risking a feedback loop into slower GDP growth.

For the energy sector itself, the shock creates opportunity: higher prices incentivize non-OPEC supply growth (U.S. shale, Brazil, Guyana) and could accelerate capital spending cycles. However, persistent disruption risks permanent capacity scarring in the Gulf, tightening the market further and raising the odds of price spikes that ultimately destroy demand.

In the long term, this underscores global energy security vulnerabilities. It may hasten diversification away from Mideast supply—favoring North American and other stable producers—while also spotlighting the fragility of chokepoints like Hormuz. If the benign scenario materializes (rapid normalization and strong supply response), prices could ease toward $80, relieving pressure. But Goldman’s net upside risks tilt the probabilities toward higher-for-longer oil, with profound implications for inflation, monetary policy, and investment flows into the energy complex.

Energy markets are pricing in this volatility in real time. The coming weeks of inventory data, geopolitical headlines, and demand indicators will determine whether this becomes a contained event or a multi-quarter regime shift.

Appendix: Sources and Links

- Goldman Sachs Commodities Research Note (26 April 2026): Summarized in the X post by

@NoLimitGains(includes full page image of the report). https://x.com/NoLimitGains/status/2048764917449208025

- TradingView / Invezz: “Goldman raises price forecasts as oil market faces 9.6M bpd deficit” (detailed summary). https://www.tradingview.com/news/invezz:871dbce64094b:0-goldman-raises-price-forecasts-as-oil-market-faces-9-6m-bpd-deficit/

- BOE Report: “Goldman Sachs raises oil price forecasts on tight supply.” https://boereport.com/2026/04/26/goldman-sachs-raises-oil-price-forecasts-on-tight-supply/

- Additional coverage: Marketscreener, Reuters-sourced reports, and related analyses confirming the 9.6 mbd Q2 deficit, price upgrades, and scenarios (April 26–28, 2026).

All data and forecasts are from Goldman Sachs’ April 26, 2026 research as reported in credible financial media. This article is for informational purposes only and does not constitute investment advice.