As Europe races to eliminate its remaining dependence on Russian natural gas by late 2027, a long-dormant project is suddenly back in the spotlight. The proposed Trans-Caspian Pipeline (TCP) — a roughly 300-kilometer subsea link across the Caspian Sea from Turkmenistan to Azerbaijan — could deliver a significant new source of non-Russian pipeline gas to the EU. With an estimated price tag of around $12 billion and renewed high-level calls for action from Turkey, the project is emerging as more than just an energy infrastructure play: it could reshape geopolitical leverage in the Caspian region and provide a critical workaround for Europe’s gas needs.

The idea is straightforward yet strategically profound. Turkmen natural gas would flow from Turkmenbaşy directly to Baku, Azerbaijan, then feed into the existing Southern Gas Corridor (SGC) — comprising the South Caucasus Pipeline (SCP), Trans-Anatolian Pipeline (TANAP) through Turkey, and Trans-Adriatic Pipeline (TAP) into Europe. This route would completely bypass both Russia and Iran, creating a new east-west energy artery that sidesteps traditional chokepoints.

How Much Gas Could It Move?

Capacity estimates for the TCP have varied over the years, but the project is typically envisioned in phases. Initial operations could transport 10–16 billion cubic meters (bcm) per year, with potential expansion to 30 bcm annually. For context, this would represent a meaningful addition to Europe’s supply — potentially covering a sizable portion of the volumes Europe is phasing out from Russia (currently down to about 12% of imports but still totaling tens of bcm). Turkmenistan sits on some of the world’s largest proven gas reserves (fourth-largest globally), much of it in the massive Galkynysh field, and already exports over 30 bcm annually — primarily to China. The TCP would allow Ashgabat to diversify its markets without relying on LNG or contested swap deals.

Azerbaijan’s own SGC is currently operating at roughly 50% capacity, and plans exist to expand TANAP and TAP further. Turkmen gas could slot in seamlessly, helping Europe avoid the price volatility and higher costs of LNG imports while providing a more secure, long-term pipeline alternative.

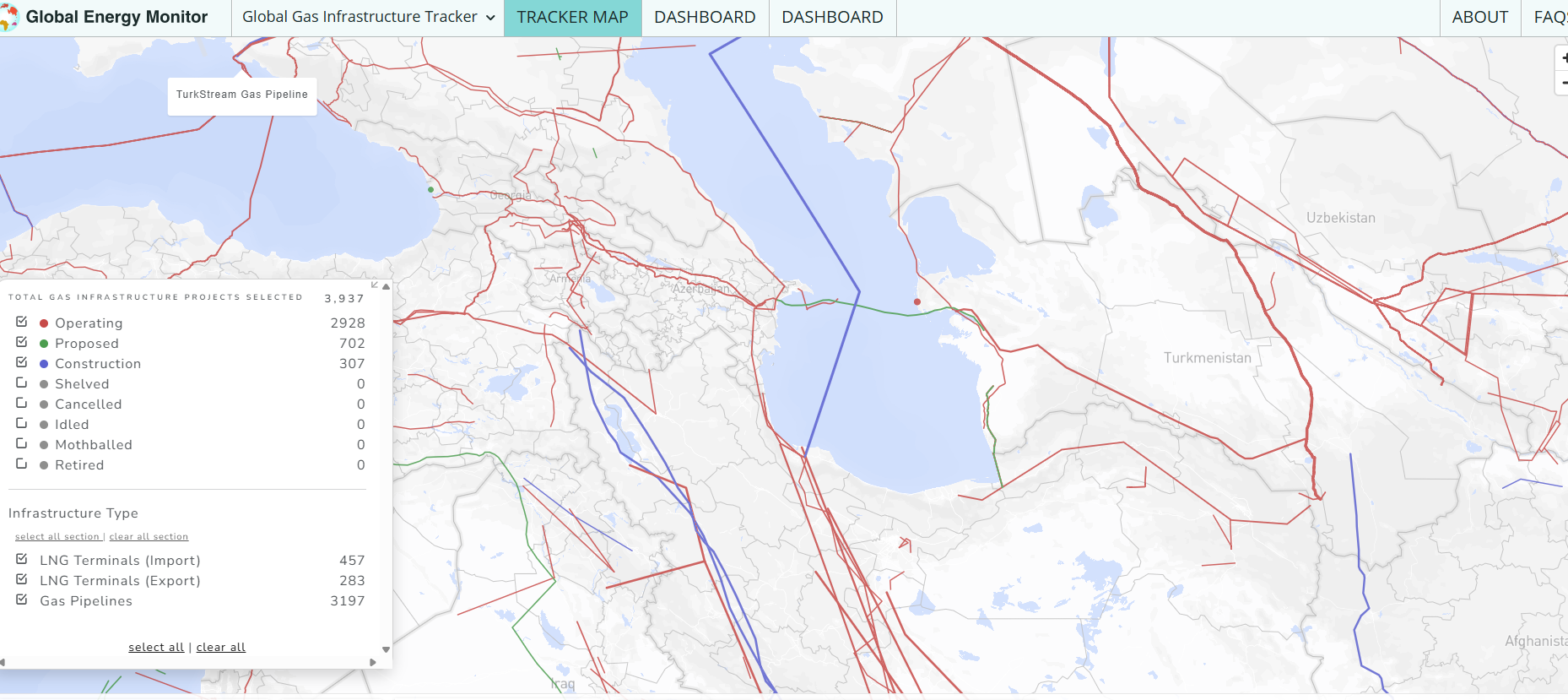

(Map showing the proposed Trans-Caspian Pipeline (green line center across the Caspian Sea) integrating with the Southern Gas Corridor to deliver gas to Europe. Source: GIS Reports)

A Workaround for Europe’s Russian Gas Dilemma

The timing could hardly be better. The EU has enacted legally binding measures to phase out Russian pipeline gas and LNG imports, with the final volumes expected to exit the market within the next two years. Azerbaijan already supplies around 12–20 bcm to Europe via the SGC, but production ramp-up has faced delays. Turkmenistan’s vast resources offer a ready supplement — one that doesn’t require new LNG terminals or reliance on volatile global shipping routes.

For Turkey, the project is equally compelling. Ankara has lost access to Iranian gas supplies amid regional instability and is actively seeking alternatives to Russian volumes (which still make up a significant share of its imports). Turkish Energy Minister Alparslan Bayraktar recently emphasized the urgency: “We believe it is absolutely necessary to realize a pipeline that will transport Turkmen natural gas from the Caspian Sea to Türkiye and from Türkiye to Europe.”

The Geopolitical Twist: A New Influencer Emerges

Beyond the numbers, the TCP represents a fascinating shift in energy geopolitics. For decades, Russia and Iran have dominated Caspian energy narratives through transit leverage and market control.

A successful pipeline would:

Empower Turkmenistan to reduce its heavy reliance on China (its primary buyer for over 20 years) and gain direct access to premium European markets.

Elevate Azerbaijan and especially Turkey as pivotal energy hubs, strengthening their strategic positions.

Give the EU a diversified, non-Russian pipeline option that enhances energy security without heavy dependence on LNG or Middle Eastern routes vulnerable to disruptions like those in the Strait of Hormuz.

Create a new “Middle Corridor” dynamic that bypasses both Russia and Iran entirely — a rare feat in Eurasian energy infrastructure.

This could dilute Russia’s traditional influence over Central Asian exporters and force a recalibration of power in the region. Turkey’s role as a gas hub would grow, potentially reducing its own exposure to Moscow. In short, the TCP isn’t just pipes in the sea — it’s a potential new geopolitical influencer tilting leverage toward a Central Asia–Caucasus–Europe axis.

Who Might Want to Stop It?

Not everyone is enthusiastic. Russia and Iran have opposed the project for nearly three decades, citing environmental risks to the Caspian Sea — a concern they have raised consistently despite existing pipelines in the region and the 2018 Caspian Convention, which allows adjacent states to proceed by agreement.

Russia sees the pipeline as direct competition for its European gas customers and a loss of leverage over Turkmenistan.

Iran views it as undermining its potential as a transit route and challenging its regional influence; past swap deals with Turkmenistan collapsed partly due to sanctions.

Financing remains a major hurdle — $12 billion is a steep ask in a geopolitically risky environment, and Turkmenistan has historically been cautious, prioritizing its longstanding ties with China. Azerbaijan has signaled willingness to allow transit but not to shoulder new infrastructure costs itself. Environmental and legal questions, while sometimes used as pretexts, add layers of complexity for investors.

Outlook

The TCP has been discussed since the late 1990s without concrete progress — until now. With Europe’s Russian gas cutoff looming, Turkey’s urgent push, and shifting regional dynamics, momentum is building. A lighter, faster-to-build version delivering 10–12 bcm could even be feasible at far lower cost.

If realized, the Trans-Caspian Pipeline would deliver more than just molecules of methane: it would bring a new balance of power to Eurasian energy markets. But it would only take an oil tanker passing through, dragging an anchor, to ruin the pipeline. So a more expensive design might be recommended.

- “The $12 Billion Pipeline That Could Help Ease Europe’s Gas Crisis” – OilPrice.com / Eurasianet (April 30, 2026)

https://oilprice.com/Energy/Energy-General/The-12-Billion-Pipeline-That-Could-Help-Ease-Europes-Gas-Crisis.html - Global Energy Monitor – Trans-Caspian Gas Pipeline (capacity and project details)

https://www.gem.wiki/Trans-Caspian_Gas_Pipeline - “Trans-Caspian Pipeline plan gaining critical momentum” – GIS Reports (March 2026)

https://www.gisreportsonline.com/r/trans-caspian-pipeline-momentum/ - “Now Is The Time To Build Trans-Caspian Pipelines” – Eurasia Review (April 2026)

https://www.eurasiareview.com/25042026-now-is-the-time-to-build-trans-caspian-pipelines-analysis/ - Yorktown Institute – “Trans-Caspian Pipeline: Turkmenistan’s Last Hope for Major Gas Exports” (October 2025, updated context)

https://yorktowninstitute.org/trans-caspian-pipeline-turkmenistans-last-hope-for-major-gas-exports/ - Wikipedia – Trans-Caspian Gas Pipeline (historical overview)

https://en.wikipedia.org/wiki/Trans-Caspian_Gas_Pipeline - European Commission – REPowerEU and Russian gas phase-out updates (2026)

https://energy.ec.europa.eu/strategy/repowereu-phase-out-russian-energy-imports_en

Additional maps and analysis available via Caspian Policy Center and related 2025–2026 reports.