In a move signaling a renewed focus on its core oil and gas operations, BP announced on May 7, 2026, that it plans to sell portions of its equity stakes in two flagship UK carbon capture and storage (CCS) projects in Northern England. The decision comes as both projects—Net Zero Teesside (NZT) Power and the Northern Endurance Partnership (NEP)—have achieved major milestones, including financial close and the start of construction.

BP described the timing as strategic in an emailed statement: “As the NZT Power and NEP projects have reached major milestones, including financial close and the start of construction, BP considers this the right time to sell a portion of its equity in both projects.” The company did not disclose the size of the stakes for sale or potential buyers.

The NZT Power project, a joint venture between BP and Equinor, is set to become the world’s first gas-fired power plant equipped with carbon capture technology. Once operational in 2028, it is expected to deliver low-carbon power to approximately one million homes in the UK. The NEP, which includes partners Equinor and TotalEnergies (with Shell having exited in 2023), aims to provide permanent storage for up to 4 million tonnes of CO₂ per year initially.

This divestment aligns with BP’s broader “back to basics” strategy, as the company looks to simplify its portfolio, recycle capital into higher-return traditional energy assets, and navigate a challenging transition environment where CCS projects face high capital costs and uncertain economics despite policy support.

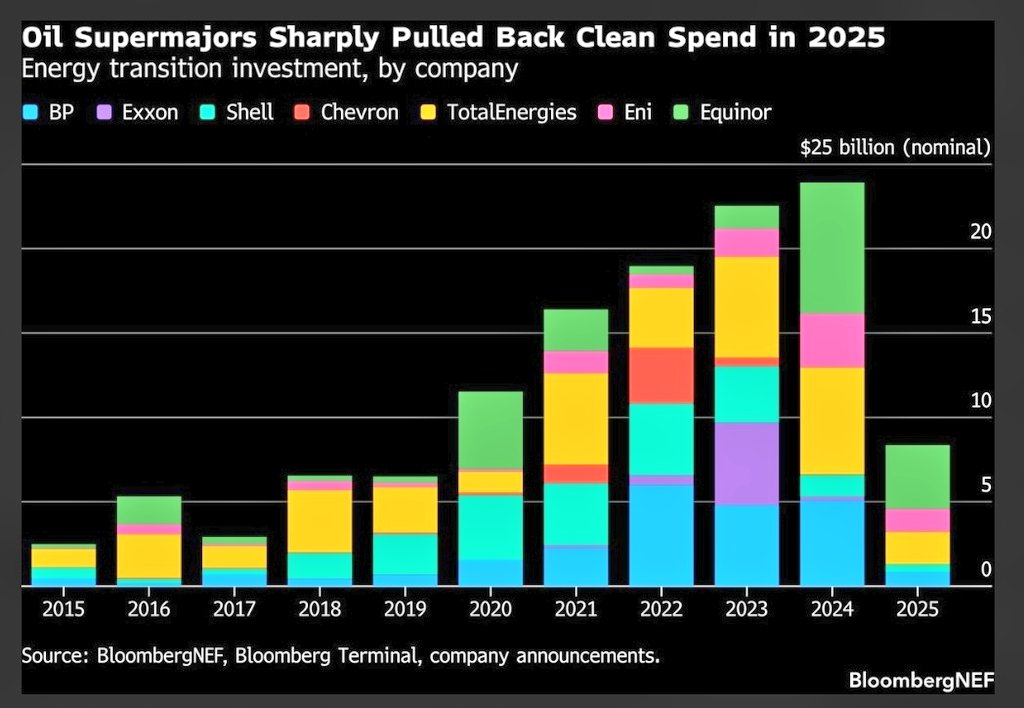

Note that spending by oil majors on green energy is falling.

Contrast with Occidental Petroleum’s Aggressive Push in the US

While BP trims its CCS exposure in the UK, US major Occidental Petroleum (Oxy) continues to double down on carbon management, particularly through direct air capture (DAC) technology. Oxy’s subsidiary 1PointFive is advancing the Stratos DAC facility in Ector County, Texas—the world’s largest planned DAC plant. As of early 2026, Stratos is in final commissioning and startup phases, with Phase 1 targeting commercial operations in Q2 2026 and full ramp-up to 500,000 metric tonnes of CO₂ capture per year by the end of 2026.

Oxy has already pre-sold millions of carbon removal credits from Stratos to major corporations, including Microsoft and Amazon. The US Department of Energy has also retained funding for related DAC hubs in Texas and Louisiana that were initially targeted for review.

Oxy positions itself as a “dual-engine” player—maintaining strong Permian Basin oil production while building a carbon management business that could generate independent high-margin revenue streams. Earlier legacy CCS projects like the Century plant were sold off, but the focus has shifted decisively to scalable DAC and enhanced oil recovery (EOR) applications supported by the 45Q tax credit.

Is the Future Value of Carbon Capture Projects Fading?

Not yet—and major governments show little sign of backing off. The value proposition for CCS and DAC remains challenged by high upfront costs (often $1 billion+ per facility) and lengthy payback periods, but policy momentum in the UK, EU, and Democrat-led US states continues to provide subsidies, tax credits, and regulatory tailwinds.

UK: The government has committed substantial subsidies (including up to £23 billion cited for certain gas-CCS projects) and maintains ambitious targets for industrial clusters and storage capacity. Track 1 and Track 2 sequencing policies continue to support revenue mechanisms like contracts for difference.

EU: The Net Zero Industry Act and revised CCS Directive target 50 million tonnes of annual injection capacity by 2030. Cross-border storage hubs in the North Sea and integration with the EU ETS (with carbon prices stabilizing around €65–€75/tonne) keep projects bankable despite cost pressures.

US Democrat States and Federal Policy: Blue states such as California continue aggressive net-zero mandates that include CCS/DAC as compliance tools. Federally, the 45Q tax credit remains intact (with recent modifications maintaining parity for EOR and geologic storage), and the DOE has preserved funding for key DAC hubs. Corporate offtake and power-sector demand driven by data centers further bolsters the economy.

Analysts note that while some oil majors are pruning marginal CCS bets to prioritize shareholder returns amid strong oil prices, overall global CCUS investment is projected to grow, with the market expanding from roughly $5 billion in 2026 toward $13 billion+ by 2036.

High costs and subsidy dependence remain headwinds, but first-mover projects like Stratos and UK clusters are moving from planning to construction.

Impact on Consumers and Investors

Consumers: Subsidies for early CCS projects are often recovered through electricity bills or public budgets, potentially adding to near-term energy costs (as seen in UK examples). However, successful deployment could enable continued use of reliable, dispatchable power and industrial heat with lower emissions, helping moderate long-term price volatility compared to full fossil-phaseout scenarios. Studies suggest CCS can even lower the effective price of fossil-based products up to certain capture thresholds when combined with tax incentives.

Investors: BP’s sale represents classic capital recycling—freeing balance-sheet capacity for core upstream opportunities while de-risking projects for new entrants (likely infrastructure funds or other energy players). Oxy’s approach has been rewarded with stock outperformance tied to its carbon leadership narrative. Broader investor appetite exists for offtake-backed credits and storage infrastructure, but risks include policy shifts, cost overruns, and competition from cheaper renewables in some applications. Long-term, scaled CCS/DAC could create new revenue streams decoupled from oil prices.

In summary, BP’s move highlights the maturing phase of CCS, where pioneers divest post-FID to focus on strengths, while leaders like Oxy bet big on commercialization. Governments in the UK, EU, and Democrat-led US states are tripling down rather than fading, keeping carbon capture central to industrial decarbonization—albeit at a measured, subsidy-supported pace. As an investor, I would not invest in an oil company that is as focused on Carbon Capture and selling carbon credits as part of its bottom line. While it may be great in the short run, it is clear that the world’s funding for Carbon Capture and subsidies may be tightening. And fortunately, we don’t give investment advice.

Appendix: Sources and Links

- Reuters: “BP to sell stakes in flagship UK carbon capture projects in Northern England” (May 7, 2026) – https://www.reuters.com/sustainability/climate-energy/bp-sell-stakes-flagship-uk-carbon-capture-projects-northern-england-2026-05-07/

reuters.com

- Multiple updates on Occidental Petroleum Stratos DAC project (2026 commissioning): RBN Energy, Oil & Gas Journal, 1PointFive official site, and financial analyses (March–April 2026 reports).

- US DOE funding retention for DAC hubs (April 17, 2026) – Reuters.

- Market outlooks: Future Market Insights (CCUS market to 2036), IEA/ING analyses on European CCS progress (2026), IEEFA and Carbon Pulse reports on UK/EU policy.

- Consumer/investor impact studies: ScienceDirect papers on CCS energy price effects (2026) and industry reports from Wood Mackenzie and BCG.

All information drawn from publicly available news, company statements, and market analyses as of May 8, 2026.