Guyana’s offshore Stabroek block continues to deliver exceptional results for two of the world’s largest energy companies. In 2025, ExxonMobil reported approximately $4.67 billion in profit from its Guyana operations, while Chevron (through its acquisition of Hess) reported $2.89 billion. The combined $7.56 billion underscores the block’s status as one of the most profitable and lowest-cost oil developments globally.

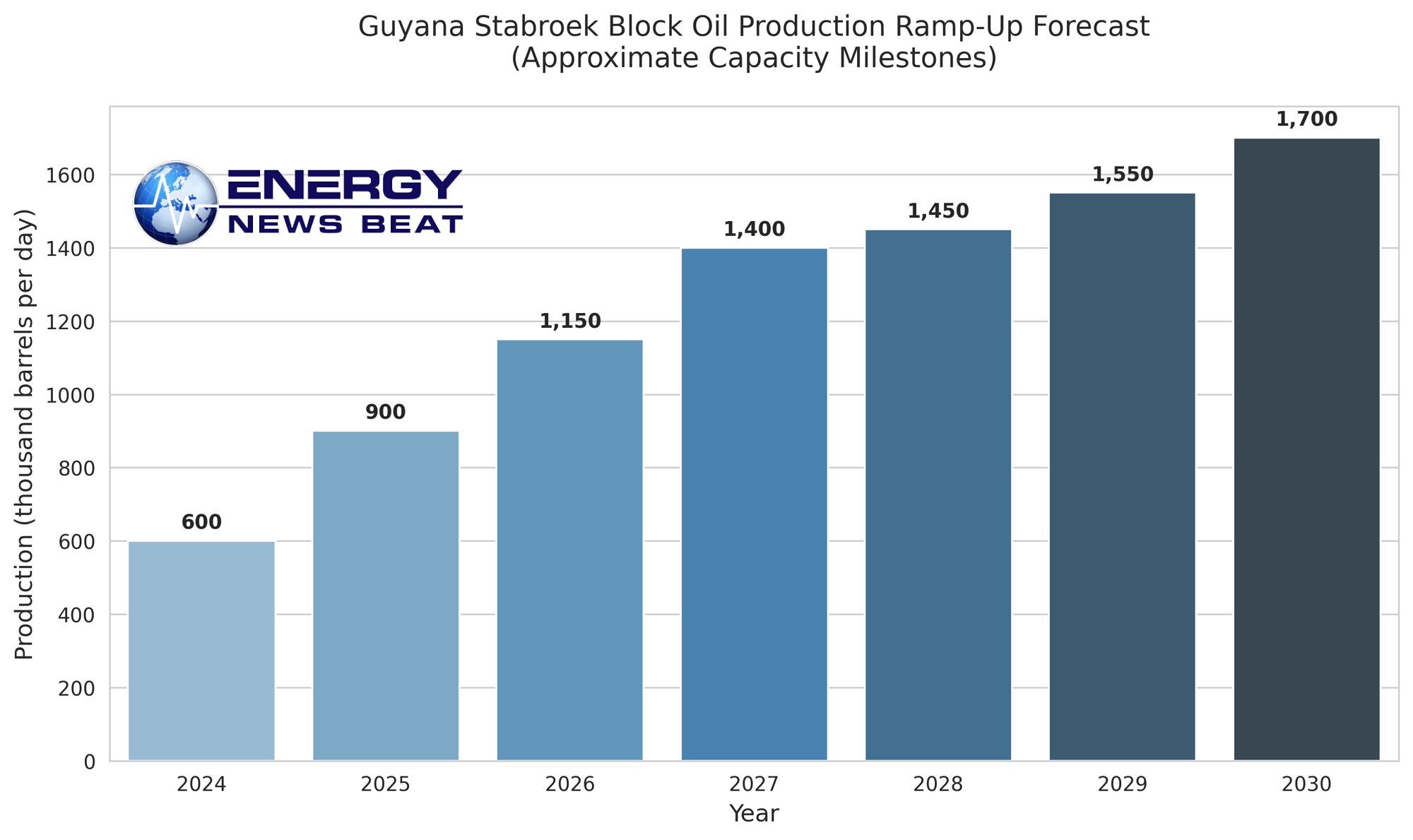

This performance comes as production from the Stabroek block reached 900,000 barrels per day (bpd) in November 2025, with four floating production storage and offloading (FPSO) vessels online. The resource base exceeds 11 billion barrels of recoverable oil, making it the largest crude discovery of the past decade.

Rapid Development Pipeline

ExxonMobil (45% working interest, operator), Chevron (30% via Hess), and CNOOC (25%) have sanctioned multiple phases with total planned investment exceeding $60 billion on the block alone.

Key upcoming projects include:

Uaru (5th development) — Expected startup in 2026, adding ~250,000 bpd capacity.

Whiptail (6th) — Startup targeted for 2027, another ~250,000 bpd.

Hammerhead (7th) — Sanctioned in 2025, first oil expected 2029, ~150,000 bpd.

Longtail (8th) — Under regulatory review; if approved, it would contribute to the total installed capacity of 1.7 million bpd by 2030.

Breakeven costs for several projects (including Yellowtail) are as low as ~$25 per barrel, roughly half the breakeven of many U.S. shale plays. EBITDA margins for ExxonMobil Guyana Limited reached 58% in recent periods.

Chevron’s 2026 capital expenditure guidance of $18–19 billion includes significant offshore spending (~$7 billion globally), with Guyana as a core growth driver alongside U.S. assets.

Part of a Global Shift Toward Secure, Non-Chokepoint SupplyGuyana’s rise fits into a larger strategic realignment by energy companies and importing nations. Recent geopolitical tensions around traditional chokepoints — particularly the Strait of Hormuz — have accelerated efforts to secure diversified supplies outside vulnerable maritime routes.

Global oil chokepoints map highlighting the Strait of Hormuz and alternative routes. Diversification efforts are intensifying as nations seek reliable supply chains. (Illustrative)Guyana offers proximity to major refining centers in the Americas, reducing reliance on long-haul shipments through contested waterways. Political stabilization in Venezuela (following the ouster of the previous regime and easing of certain restrictions) further strengthens Western Hemisphere energy security, potentially unlocking additional investment and production in the region.This aligns with broader industry trends: major operators are ramping up high-impact exploration and development spending in 2026–2027 and beyond in frontier and established basins outside traditional Middle East dependencies. Examples include:

Continued strong activity and rig additions in the U.S. Permian Basin.

High-impact wells planned in Brazil (e.g., Petrobras’ Morpho-1 in the Foz do Amazonas basin and Equinor activity in the Santos pre-salt).

Ongoing evaluation of other Atlantic-margin opportunities.

These moves reflect a deliberate strategy to build resilient supply chains amid evolving global dynamics.

What This Means for Investors

For ExxonMobil (XOM) and Chevron (CVX) shareholders, Guyana represents a high-quality, long-duration growth engine:

Earnings and cash flow accretion — Low-cost barrels flow directly to the bottom line with minimal capital intensity going forward.

Dividend strength — Both companies maintain industry-leading track records of consecutive annual dividend increases (Exxon: 43+ years; Chevron: 39+ years). Guyana’s cash generation supports shareholder returns alongside share buybacks.

Portfolio resilience — These assets perform well across a wide range of oil price scenarios and form a growing share of future production (targeted ~65% of Exxon’s advantaged volumes by 2030 alongside Permian and LNG).

Key metrics to watch — Quarterly production updates from Stabroek, FPSO startup milestones (especially Uaru in 2026), capex discipline, and any Longtail approval. Both balance sheets remain strong and investor-friendly.

Guyana is no longer a speculative story — it is a proven, cash-flowing core asset that enhances the investment case for these supermajors.

Implications for Consumers and Global Energy Markets

For consumers, additional low-cost supply from Guyana helps moderate price volatility. Reliable output from a politically stable jurisdiction in the Americas reduces exposure to disruptions in distant chokepoints, supporting more predictable energy costs over time.

The combination of Guyana’s ramp-up, Venezuelan stabilization, U.S. shale discipline, and Brazilian developments contributes to a more diversified and secure global supply picture heading into the late 2020s.

- The Globe and Mail / Motley Fool article on combined profits (June 2026): https://www.theglobeandmail.com/investing/markets/stocks/NVDA/pressreleases/2408545/exxonmobil-and-chevron-reported-a-combined-76-billion-profit-in-guyana-last-year-what-energy-investors-need-to-know/ (note: actual combined figure ~$7.6B)

- Reuters: Exxon 2025 Guyana profit $4.67B (June 9, 2026): https://www.reuters.com/business/energy/exxon-2025-profit-guyana-totaled-467-billion-2026-06-09/

- OilNOW.gy coverage of Guyana developments and 2026 outlook.

- ExxonMobil corporate releases on Stabroek production milestones and project sanctions.

- Chevron 2026 Capex guidance (Dec 2025 / Q4 updates).

- EIA and industry reports on global production forecasts and chokepoint dynamics.

Key Data Summary (2025–2030)

- 2025 Production: ~900,000 bpd (Nov peak)

- 2026 Target: >1.0–1.15 million bpd (Uaru startup)

- 2027+: Further ramp with Whiptail

- 2030 Capacity Target: 1.7 million bpd

- Recoverable Resources: >11 billion barrels

- Breakeven: As low as ~$25/bbl on select developments

Recommended Visuals for Channel

- FPSO imagery (ONE GUYANA, Prosperity, etc.)

- Production ramp timeline graphic

- Global chokepoints map (for diversification context)

- Company production contribution charts (Guyana vs. total portfolio)

Guyana’s success story is far from over. For investors seeking stable, high-return energy exposure with strong dividend characteristics, ExxonMobil and Chevron remain compelling names as this world-class asset continues scaling. The broader industry shift toward secure, diversified supply outside traditional chokepoints only enhances the strategic importance of these developments.