Dallas Fed Energy Survey and Market Impact

The U.S. oil and gas sector is showing clear signs of accelerating activity in the second quarter of 2026, according to the latest Dallas Fed Energy Survey. Executives report stronger business conditions, improved outlooks, and rising capital spending, even as input costs and operating expenses climb. This momentum comes amid easing geopolitical tensions and resilient domestic production, though broader market forecasts point to moderating price pressures ahead.

And I do not believe the US oil companies are gouging consumers at the pump, as President Trump made the allegations. More on that later in the article.

Dallas Fed Energy Survey Highlights (Q2 2026)

The survey, based on responses from 127 firms (82 exploration & production and 45 oilfield services companies in the Eleventh Federal Reserve District) collected June 9–17, 2026, paints a picture of robust expansion.

The business activity index surged to 46.1 (from 21.0 in Q1), the strongest reading since Q2 2022. Over half of firms (54%) reported increases.

E&P activity index reached 48.2; oilfield services hit 42.3.

The oil production index rose to 15.0 (from 0.0), with 35% of E&P firms noting gains. Natural gas production edged up modestly (3.7).

Capital expenditures strengthened significantly, with the index climbing to 40.9 (from 21.2). E&P capex index stood at 42.7.

Supplier delivery times lengthened (31.7), signaling supply chain strains.

Employment ticked higher overall (index 4.7), though E&P employment was flat. Wages and benefits continued rising.

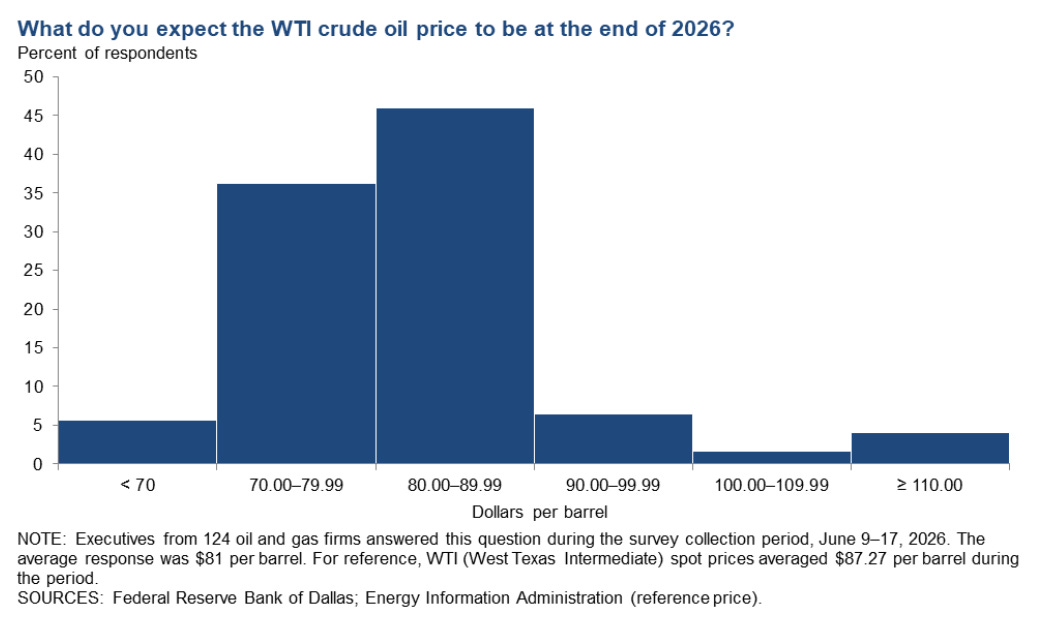

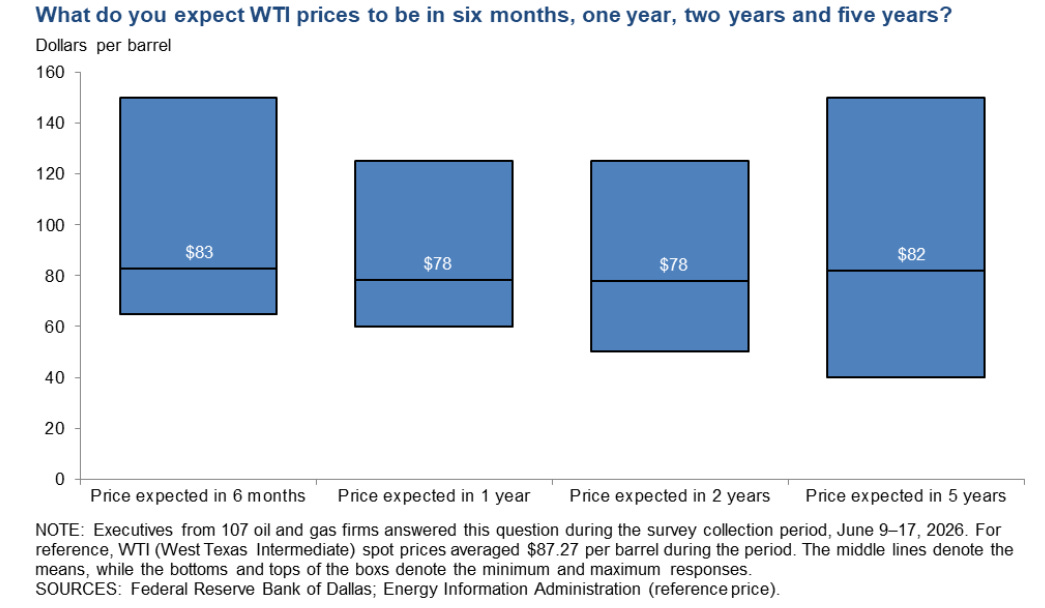

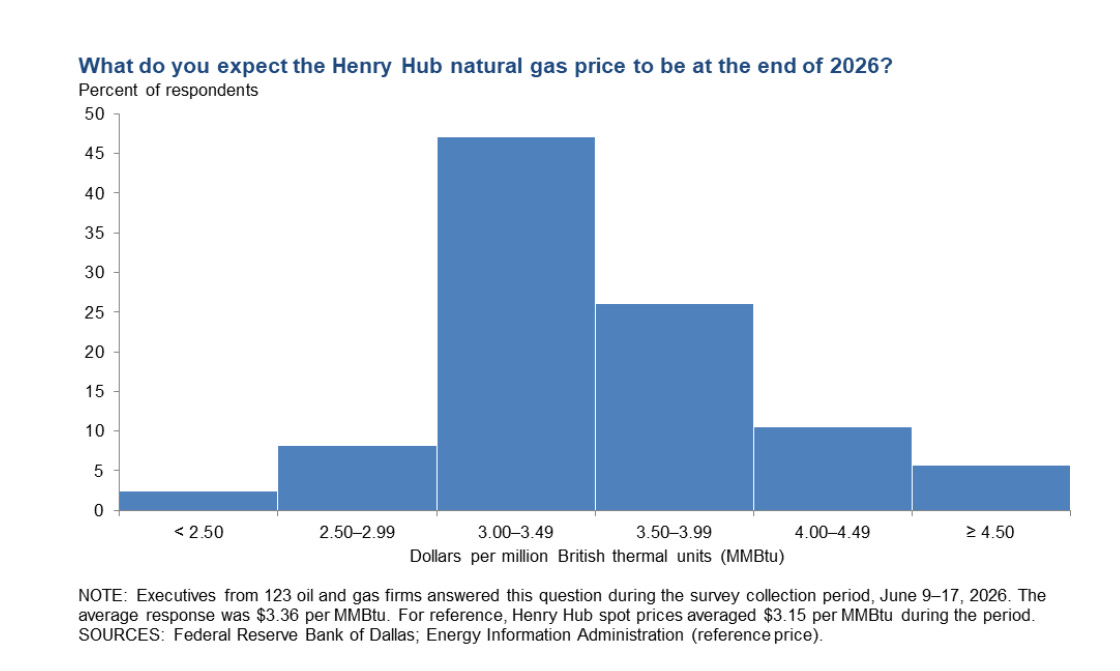

Outlooks brightened: The company outlook index remained positive at 29.3. E&P firms were notably optimistic (48.2), while services firms stayed cautious (-4.4). Uncertainty declined sharply (index fell to 29.9 from 53.7).Price expectations (survey-period WTI averaged ~$87): Respondents expect WTI at $81/bbl by year-end 2026 (range $60–$150), $78/bbl in two years, and $82/bbl in five years. Henry Hub natural gas: $3.36/MMBtu year-end 2026.

Cost pressures intensified: Services input costs index jumped to 64.4 (no firms reported decreases).

E&P finding & development costs rose to 40.0; lease operating expenses to 43.7.

Services firms saw improving operating margins (52.2, first positive in quarters) and higher prices received (24.5).

Special questions highlighted the Permian Basin (key focus area): Natural gas takeaway constraints are expected to resolve fully by Q1 2027 for many firms. Drilling hurdles include gas takeaway capacity and regulatory/policy issues inside the Permian; outside, constraints are minimal. Geopolitical risks (e.g., Iran-related) and cost inflation (fuel, labor) were top concerns.

Drilling activity in the Permian Basin, a focal point of U.S. oil and gas expansion.

Dallas Fed Survey Results:

I found this one interesting. Looking at the numbers more to the $70 to $90 range than higher. Today, with Cushing below operational minimums, we are seeing WTI oil at $71.30. When Cushing was full, we had the negative $32 crash that surprised many people.

Make no mistake, there is oil flowing from the Strait of Hormuz, but it is months from impacting delivery prices. The separation from paper to physical delivery is still a problem. Demand destruction and China’s not buying have helped keep the price down. When China starts buying again, and the other countries start buying to refill their SPRs, it will be interesting to see the Dallas Survey next quarter.

Where do you expect WTI to be in six months, one year, two years, and five years?

Stability is what is on every CEO’s mind right now.

Where do you see natural gas prices?

As we discussed on the podcast with Steve Reese, Kirk Edwards, and Kimberly Page, we see upside for Natural Gas producers and continued growth in LNG.

Broader Market Context and Cross-Checks

The Dallas Fed findings align with increased U.S. drilling and completion momentum but contrast with some longer-term forecasts anticipating slower growth due to abundant supply.

The EIA’s June 2026 Short-Term Energy Outlook projects U.S. crude oil production at 13.7 million barrels per day (mb/d) in 2026, rising to 14.2 mb/d in 2027. Brent crude is forecast to average $95/bbl in 2026 (elevated due to assumed Middle East disruptions) before moderating to $79/bbl in 2027. Henry Hub natural gas averages $3.60/MMBtu in 2026.

However, real-time market prices have eased significantly. As of late June 2026, WTI crude futures traded around $70–76/bbl, down from earlier 2026 spikes above $100 amid Iran-related tensions. Recent diplomatic progress toward easing Strait of Hormuz disruptions contributed to the decline.

Other industry outlooks (Deloitte, Enverus) emphasize capital discipline, rising costs from tariffs/supply chains, and opportunities in LNG exports amid data center-driven power demand. U.S. natural gas production is expected to grow steadily (EIA sees +3.3% in 2026), supported by associated gas from oil wells.

Impact on Consumers

For everyday Americans, the recent decline in crude oil prices is providing relief at the pump. National average regular gasoline prices have fallen toward the $3.20–$3.90/gallon range in recent weeks, with prediction markets forecasting further drops toward ~$3.00/gallon by year-end.

U.S. gasoline prices at the pump have eased alongside declining crude oil benchmarks.

Lower energy costs help tame broader inflation. Recent data shows 1-year inflation expectations dropping to multi-month lows amid falling oil prices. However, the EIA’s higher 2026 gasoline price forecast ($3.90/gallon) assumes persistent supply disruptions—if geopolitical risks re-escalate or inventories tighten further, consumers could face renewed upward pressure on fuel and related goods (transportation, groceries). Overall, the current trajectory points to modest relief for household budgets in the near term.

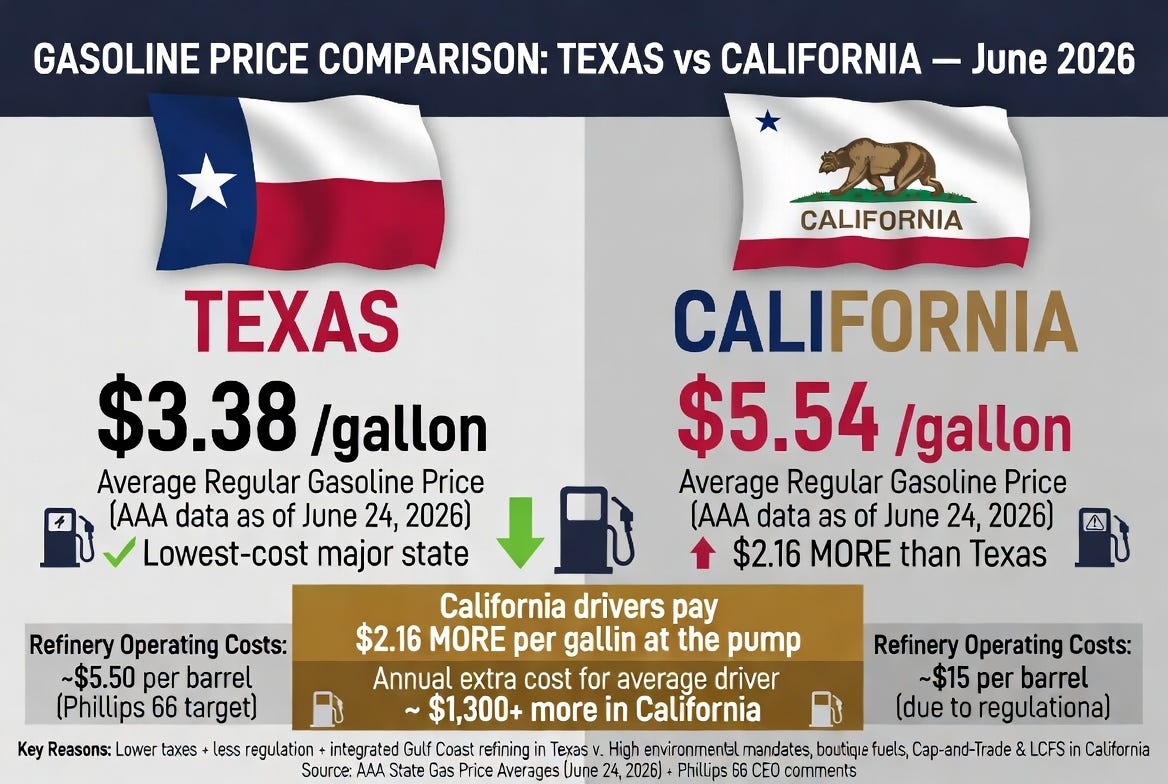

Make no mistake – When President Trump makes accusations against the oil companies for price gouging, I will bet he does not find any. What he will find is that in Texas, you see the cost of refining a barrel of oil at $5, and in California, that same barrel that they have to import from the Strait of Hormuz costs $15. Then throw on the taxes and fees for Net Zero and Climate fearmongering from the Blue States, and you get higher gasoline prices.

There is a real reason for higher gasoline prices, and look no further than the government, ethanol, regulations, and politics.

Impact on Investors

The sector’s renewed activity momentum is generally positive for energy equities, particularly upstream E&P companies and oilfield services providers benefiting from higher capex and drilling. Energy stocks have shown resilience, with segments like midstream and E&P posting solid year-to-date gains in some indices, though recent oil price pullbacks triggered short-term selling.

Energy sector performance (XLE ETF) relative to WTI crude prices illustrates investor sensitivity to commodity movements.

Key investor considerations:

Positive drivers: Rising activity indexes, improving outlooks (especially E&P), and services margin recovery signal potential revenue growth and utilization gains.

Headwinds: Accelerating cost inflation (labor, materials, inputs) could squeeze margins if oil/gas prices remain range-bound or decline further. Permian-specific bottlenecks (gas takeaway) add regional risk until 2027.

Opportunities: LNG export growth, efficiency gains, and undervalued names highlighted by analysts. Many firms continue returning capital via dividends and buybacks.

Risks: Geopolitical volatility, regulatory shifts, and global supply/demand balance (OPEC+ actions, non-OPEC growth).

Investors should monitor Dallas Fed quarterly updates, EIA data, and actual WTI/Henry Hub realizations. The combination of higher activity and cost discipline favors well-capitalized operators with strong balance sheets.

Outlook

The Dallas Fed survey confirms that oil and gas expansion is gaining real momentum in mid-2026, with brighter executive sentiment and stepped-up investment. Outlooks have improved even as cost pressures mount—a classic signal of a tightening supply chain in a recovering cycle. Cross-checked against EIA forecasts and market prices, the picture is one of resilient U.S. production growth tempered by easing near-term price spikes and ongoing efficiency focus.

For consumers, recent price moderation offers breathing room. For investors, the sector presents selective opportunities amid volatility. Continued monitoring of costs, geopolitics, and takeaway infrastructure will be essential as the year progresses.

Again, thanks to all of our great subscribers, patrons, paid subscribers, and sponsors! We appreciate you all.

Appendix: Sources and Links

- Dallas Fed Energy Survey, Q2 2026 (primary source): https://www.dallasfed.org/research/surveys/des/2026/2602

- EIA Short-Term Energy Outlook, June 2026: https://www.eia.gov/outlooks/steo/

- CME Group / Market Quotes for WTI futures (June 2026): https://www.cmegroup.com/markets/energy/crude-oil/light-sweet-crude.quotes.html

- Additional context from Enverus, Deloitte, and market analyses (via web search aggregates).

- Gasoline price and inflation context from recent market reports and AAA-linked data.

All information is current as of late June 2026. This article is for informational purposes and does not constitute investment advice.