The escalating conflict between the United States, Israel, and Iran has sent shockwaves through global energy markets, particularly affecting refined oil products like diesel, gasoline, and jet fuel. As of March 2, 2026, the war—now in its third day—has led to sharp price surges, disruptions in tanker traffic through the Strait of Hormuz, and heightened insurance risks for shipping. This article examines the current market dynamics, the state of the conflict, and the broader implications, including potential long-term scenarios for Iran’s reconstruction under U.S. influence.

The Escalating Iran Conflict: A Brief Overview

The conflict erupted on February 28, 2026, with coordinated U.S. and Israeli strikes targeting Iranian military, nuclear, and leadership sites. Iranian Supreme Leader Ayatollah Ali Khamenei was killed in the initial assault, prompting Iran to retaliate with missile and drone attacks on Israel and U.S. assets in the Gulf region, including bases in Bahrain, Saudi Arabia, Qatar, the UAE, and Iraq.

The war has since expanded, with Israel and Hezbollah exchanging fire in Lebanon, opening a new front.

Over 200 civilians have been reported killed in Iran, and three U.S. service members have died, with President Trump warning of potential further casualties.

Iranian forces have struggled to coordinate large-scale responses, with U.S.-Israeli airstrikes achieving air superiority over Tehran and targeting internal security apparatus to facilitate regime change.

The U.S. has framed the operation as an effort to dismantle Iran’s military capabilities and end its support for proxy groups, with Trump urging Iranians to “take over your government.”

As of now, the conflict shows no signs of immediate de-escalation, with ongoing strikes and retaliations threatening to engulf the wider Middle East.

Current Markets for Key Refined Products

The conflict has triggered immediate volatility in oil and refined product prices. Brent crude surged 13% to over $80 per barrel in early trading on March 2, reflecting fears of prolonged supply disruptions.

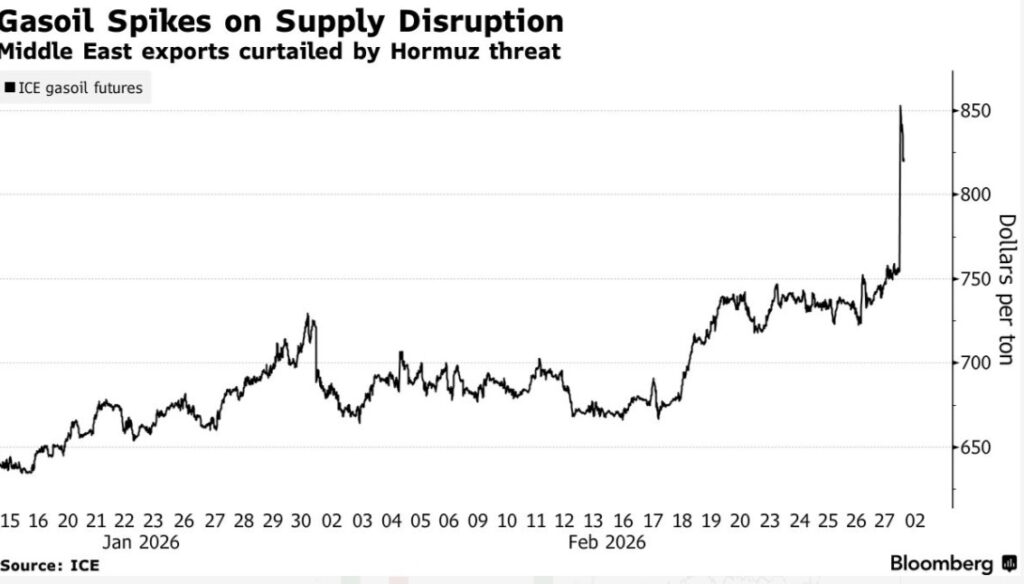

Diesel (gasoil) futures jumped even higher, by 17%, reaching a two-year high due to its critical role in military logistics and limited global alternatives.

Jet fuel and gasoline/naphtha also saw double-digit increases, with 19.4% and 16% of their global seaborne trade respectively passing through the Strait of Hormuz.

According to the latest EIA data (as of late February 2026), pre-conflict spot prices were:

|

Product

|

Price (USD)

|

Unit

|

|---|---|---|

|

WTI Crude Oil

|

~60

|

per barrel

|

|

Conventional Gasoline (New York Harbor)

|

~2.06

|

per gallon

|

|

Ultra-Low-Sulfur Diesel (New York Harbor)

|

~2.26

|

per gallon

|

|

Kerosene-Type Jet Fuel (U.S. Gulf Coast)

|

~2.03

|

per gallon

|

Post-conflict, prices have spiked: Heating oil (a diesel proxy) rose to $2.96 per gallon, up 14% in a day.

The disproportionate rise in diesel prices stems from regional supply concentration and the Strait’s role in 10.3% of global gasoil trade.

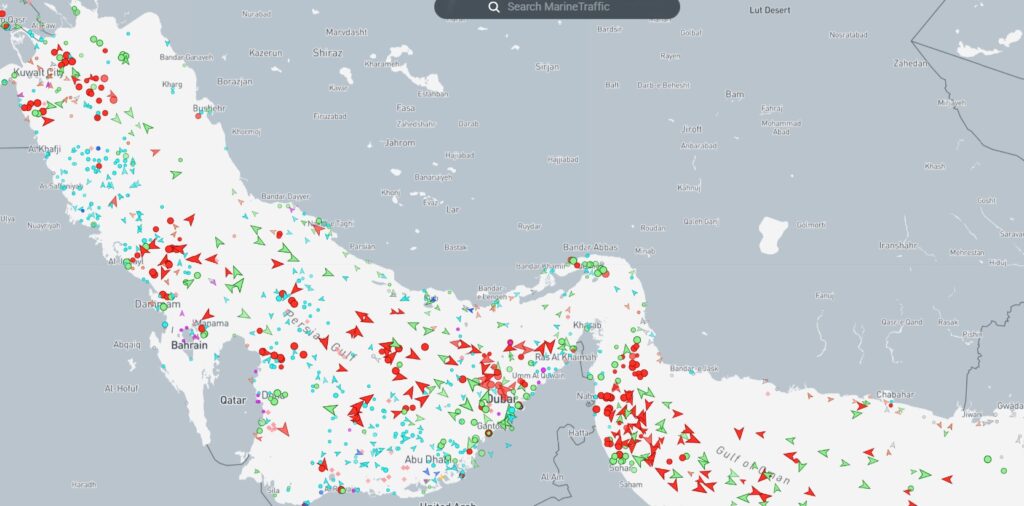

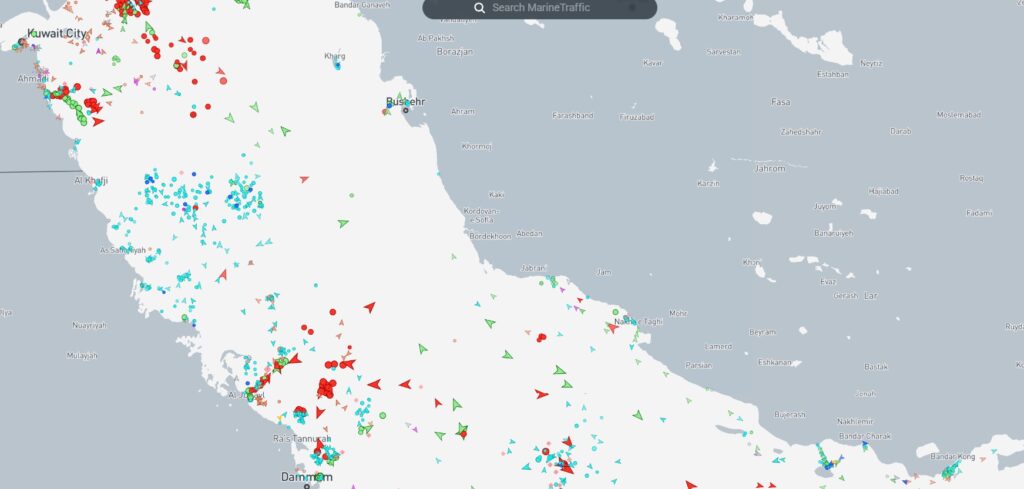

Tanker Traffic Disruptions in the Strait of Hormuz

The Strait of Hormuz, a chokepoint for nearly 20% of global oil flows, is effectively closed due to Iranian threats and retaliatory strikes. Ship-tracking data shows a 70% drop in traffic, with over 200 vessels—including 40 very-large crude carriers (VLCCs) each holding about 2 million barrels—anchored on either side.

Loading continues at Iranian sites like Kharg Island, but exports are halted, risking well shutdowns if empty tankers can’t enter.

Insurance issues exacerbate the bottleneck. War-risk insurers have canceled policies or hiked premiums by 25-50%, with some rates jumping to 0.5-1% of vessel value.

This has led shipping companies to slow arrivals or divert routes, echoing the 1980s Tanker War but with a sudden onset leaving firms scrambling.

Iranian missile capabilities could sink dozens of ships quickly, but insurance denials are already enforcing a de facto blockade.

The provided MarineTraffic screenshot from March 1, 2026, illustrates clusters of red icons (tankers) at anchorages east and west of the Strait, with minimal movement through the chokepoint.

Insights from Key SourcesMaritime analyst Sal Mercogliano’s X post from March 1 recaps the situation: The Strait is “fairly empty,” with tankers arriving at anchorages in ballast (empty) from the east and loaded from the west. He notes canceled war-risk policies forcing new coverage at 0.5-1%, ongoing loading in the Gulf, and global floating storage of 100-200 million barrels, mitigating short-term shortages.

Mercogliano predicts resumed traffic once insurance is secured, but warns of escalation risks compared to the 1980s Tanker War.

An OilPrice.com article highlights diesel’s 17% jump, outpacing crude’s 13%, attributing it to supply risks and military demand. Jet fuel and gasoline face high impacts, with sharp price cracks expected this week.

Speculative Outlook: A Short War and U.S.-Led Reconstruction

If the conflict remains short—potentially lasting weeks as Trump suggested—analysts see prices pulling back to $70 per barrel upon de-escalation.

A post-war Iran could mirror U.S. policies in Venezuela, where Treasury Secretary Scott Bessent and Energy Secretary Chris Wright have overseen sanction relief to facilitate oil sales and economic rebuilding.

In Venezuela, the U.S. controls proceeds, lifts sanctions gradually, and mobilizes frozen assets like $5 billion in IMF reserves for recovery.

Applied to Iran, such “Venezuelan-type controls” could establish a stable monetary system for a new government, channeling oil revenues toward reconstruction rather than proxy wars. This would benefit ordinary Iranians by improving living standards and reducing funding for groups like Hezbollah or the Houthis. However, large U.S. oil firms remain wary, preferring smaller companies to invest amid security concerns.

Trump aims for $100 billion in investments to revive production, but success hinges on regime change and stability.

Conclusion

The Iran conflict has thrust refined products into turmoil, with diesel leading the charge due to logistical vulnerabilities. While tanker disruptions and insurance hikes amplify short-term risks, a swift resolution could stabilize markets. Looking ahead, U.S.-style interventions might foster a more prosperous Iran, redirecting its oil wealth inward. As events unfold rapidly, energy stakeholders must brace for continued flux.

Sources: Marinetraffic.com, argusmedia.com, reuters.com, kpler.com, oilprice.com, eia.gov, bloomberg.com

Get your CEO on the #1 Energy Podcast in the United States: https://sandstoneassetmgmt.com/media/

Is oil and gas right for your portfolio? https://energynewsbeat.co/invest/