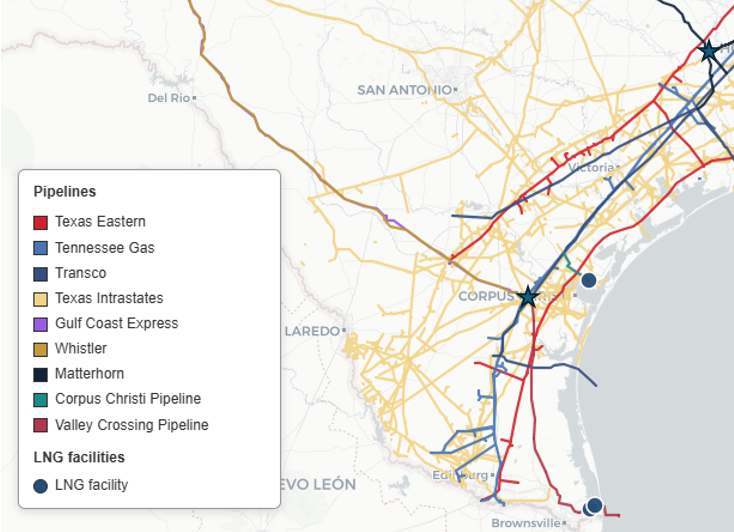

As of early June 2026, Kinder Morgan’s long-awaited Gulf Coast Express (GCX) pipeline expansion is entering service, marking a major step forward for natural gas takeaway from the Permian Basin. The fully contracted, $455 million project (Kinder Morgan’s share approximately $161 million) adds 570 MMcf/d of incremental capacity through new compression along the existing 500-mile GCX system. Once fully ramped, the pipeline will transport roughly 2.55–2.57 Bcf/d total from the Waha hub in the Permian to South Texas markets, including the critical Agua Dulce trading and storage hub.

The expansion, which involves only compression additions rather than new pipe, is a brownfield project that was fully subscribed with long-term, binding transportation agreements. Construction began in 2025, with a targeted in-service window of mid-2026 (Q2). Recent market reports confirm initial interstate deliveries ramping up around late May 2026, with Kinder Morgan CEO Kimberly Dang noting the project remains on track.

Relief for Permian Takeaway Constraints

The Permian Basin continues to see rapid associated gas growth exceeding 1.4 Bcf/d year-over-year, but takeaway capacity has struggled to keep pace. This has repeatedly driven Waha hub prices negative or deeply discounted to the national benchmark Henry Hub. In recent months, Waha fixed prices have traded as low as –$5.69/MMBtu (with basis differentials reaching –$8.25/MMBtu while Henry Hub hovered around $2.78/MMBtu in early June 2026).

The GCX expansion directly addresses this bottleneck by providing additional eastbound egress from Waha to South Texas. Market observers noted an immediate positive reaction in Permian cash prices, which climbed to a 15-week high around May 29 as initial flows began, improving from deeply negative levels to around –$0.37/MMBtu by early June.

This added capacity is part of a broader wave of roughly 4.5 Bcf/d in new Permian outbound pipelines scheduled for 2026, which analysts expect will eventually tighten the Waha–Henry Hub basis differential and support more stable pricing. Forward curves already reflect growing confidence that Waha pricing will converge closer to Henry Hub later in the decade.

Turning Waste into Revenue for Texas Producers

For Permian producers—particularly in the Delaware and Midland sub-basins—this expansion is more than a pricing story; it’s an economic lifeline. Chronic takeaway constraints have forced operators to flare gas or implement economic shut-ins when local prices fall below variable costs or pipeline commitments. Recent estimates from midstream players like Kinetik and Targa have pegged spring 2026 shut-ins in the hundreds of MMcf/d, with gas-focused producers hit hardest while crude-focused operators continue to benefit from strong oil prices.

By unlocking reliable, firm transportation to premium Gulf Coast markets, the GCX expansion allows producers to monetize associated gas rather than flare or curtail it. This directly boosts netback realizations, improves well economics, and reduces reliance on spot sales at distressed Waha prices. Producers have already been aggressively hedging Waha exposure for 2026, reflecting both the near-term relief this project provides and the long-term value of moving gas to the Gulf Coast.

Where the Gas Will Go: LNG Exports and Power Generation

The gas won’t just sit in storage—it will flow into high-demand South Texas markets. Agua Dulce serves as a key hub feeding multiple LNG export terminals along the Texas Gulf Coast (Corpus Christi, Port Arthur, and Brownsville corridors). With U.S. LNG export capacity continuing to expand rapidly, the incremental Permian supply via GCX is expected to support LNG-driven demand growth and help meet global calls for cleaner-burning natural gas.

At the same time, the gas will help satisfy rising domestic power-generation needs in Texas and the broader Southeast. Natural gas-fired plants remain the backbone of ERCOT and neighboring grids, especially during summer peaks and as intermittent renewables grow. The added firm supply enhances reliability for power producers and local distribution companies while contributing to Kinder Morgan’s broader strategy of strengthening the Permian-to-Gulf-Coast corridor (including related projects on the Trident Intrastate Pipeline and new storage capacity).

Broader Impacts Beyond Pricing

While the expansion will help moderate basis discounts and support more balanced national pricing, its real significance lies in the ripple effects: reduced flaring and shut-ins (with environmental and regulatory benefits), stronger producer cash flows in Texas, enhanced LNG export competitiveness, and greater grid reliability for power markets. It underscores the Permian’s role as one of North America’s fastest-growing gas supply regions and the critical need for midstream infrastructure to match production growth.As the GCX expansion ramps up in the coming weeks, it represents not just another pipeline milestone but a structural shift that lets Texas producers turn previously stranded gas into revenue—while feeding both export and domestic demand centers that keep U.S. energy leadership intact.

Appendix: Sources and Links

- Kinder Morgan Official Project Page: Gulf Coast Express Expansion Project – https://www.kindermorgan.com/Operations/Projects/GCX-Expansion-Project (details on capacity, cost, status, and markets)

kindermorgan.com

- Energies Media (Mar 21, 2026): “Kinder Morgan advances expansion work on the Gulf Coast Express natural gas pipeline” – https://energiesmedia.com/kinder-morgan-expansion-work-on-the-gulf-coast/ (timeline, total capacity, LNG implications, and Permian supply dynamics)

energiesmedia.com

- AEGIS Hedging Basis Brief – Waha Gas (June 5, 2026 update): https://aegis-hedging.com/insights/basis-brief-waha-gas (price impacts, entry-into-service confirmation, Waha vs. Henry Hub differentials, and producer shut-in context)

aegis-hedging.com

- Additional context drawn from East Daley Capital, Natural Gas Intelligence, and EIA Henry Hub price data referenced in public market reports (June 2026).

All information is based on publicly available company disclosures and independent energy market analysis as of June 10, 2026.