Powell to Congress: Higher rates are “the absolute best thing we can do for the housing market…” – “…particularly for younger people who are not yet in the housing market.”

By Wolf Richter for WOLF STREET.

However we want to interpret this, it’s fascinating. Powell told Congress on Tuesday: “There’s no question that higher interest rates are making it harder to buy homes in the short term. But in the longer term, this is the best thing, particularly for younger people who are not yet in the housing market.”

Did he mean that younger people would benefit from lower home prices, or at least an end of the home-price increases, and that higher rates are going to accomplish that? I don’t know. To speak that truth would be, sacrilege?

“Higher interest rates” means higher than they used to be, so even if the Fed cuts its rates a few times in the future, they’d still be much higher than before the pandemic, and mortgage rates would still be much higher as well.

The purpose of the higher rates is to “get back to 2% inflation for the whole economy,” he said, according to MarketWatch, “so that the housing market can be on a better foundation.”

These higher rates are “the absolute best thing we can do for the housing market and for the economy [so as] to sustainably bring inflation back down, so that people aren’t talking about it anymore,” he said.

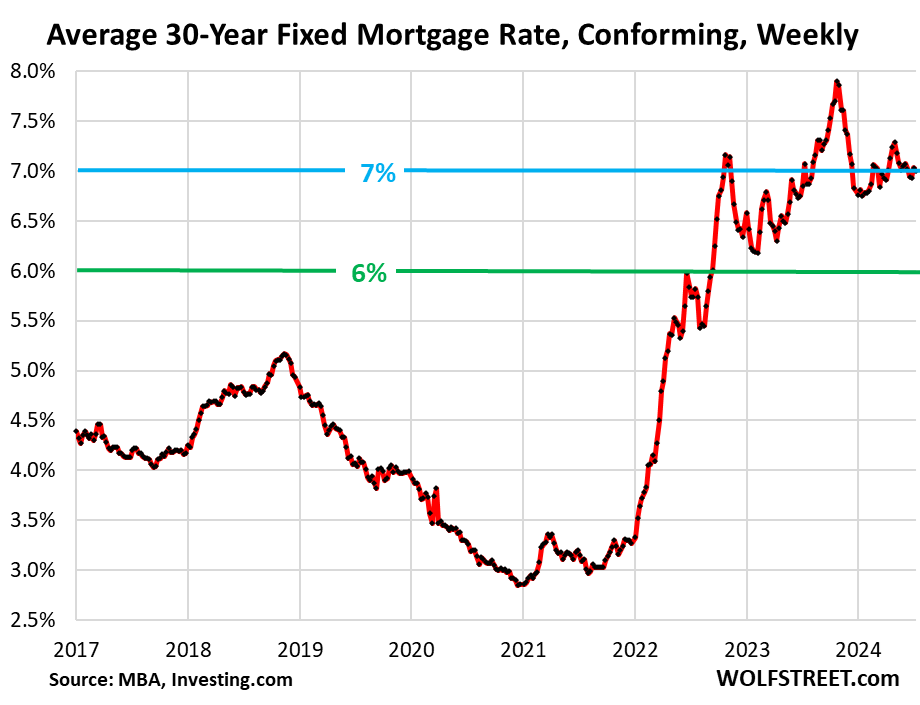

Higher for Longer: 7% mortgages a year so far.

According to the Mortgage Bankers Association today, the average conforming 30-year fixed mortgage rate was 7.0% in the latest reporting week.

The 7% mortgage has been a fixture in the housing market for a year. This measure of the average mortgage rate has hovered around 7% since July 2023, ranging from 6.75% at peak-Rate-Cut Mania in January 2024 to 7.9% in October 2023. It has been above 6% since September 2022.

People who financed a home purchase with mortgage rates at 6% or 7% or over 7% since September 2022, hoping that they would be able to refinance that mortgage quickly into a 4% mortgage, have gotten stuck with their mortgage payments.

These new homeowners with 7% mortgages and big mortgage payments may be forced to cut back spending on other goods and services, thereby lowering demand for those goods and services. The Fed is counting on them to do that. They’re one of the official transmission channels of Fed policy rates to the overall economy, to lower demand, and thereby lower inflationary pressures.

Potential homebuyers today have to do the same calculus: When will mortgage rates drop far enough to make it worthwhile refinancing a 7% mortgage, given the points and expenses involved in a refi? This is a tough call – especially since renting an equivalent house is now a lot less costly on a monthly basis.

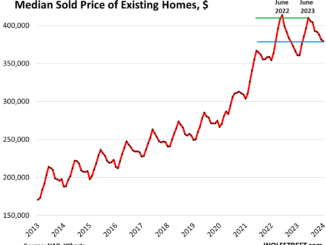

Compared to the pre-QE era, a 7% mortgage rate is not breaking new ground: From 1970 through 2001, mortgage rates ranged from 7% to 18%. Lower home prices made those higher mortgage rates work.

But ultra-low mortgage rates fuel housing bubbles. When mortgage rates dropped as low as 5.5% in 2005, they fueled Housing Bubble 1, which led to the Housing Bust from 2006-2012. The pandemic-era below-3% mortgages did a wonderful job inflating housing prices in a historic manner.

But now, these 7% mortgages conflict with the too-high prices. And something has to give.

With prices too high, buyers’ strike continues.

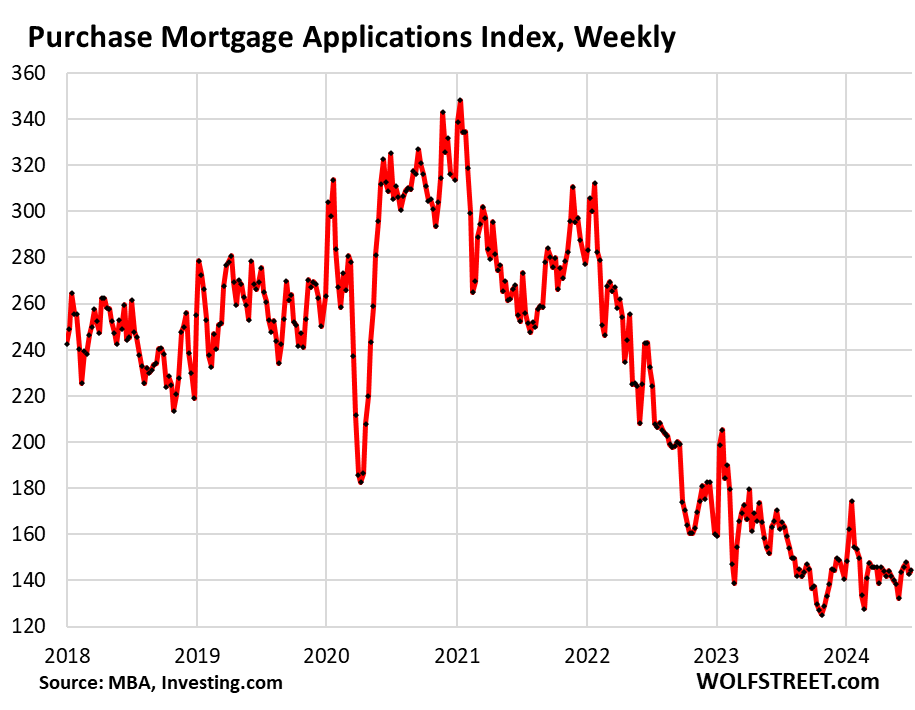

Mortgage applications to purchase a home in the latest reporting week remained near the historic lows in the data going back to 1995, and have been there over the past 12 months. The record lows in the data were set in November 2023 and February 2024. Note the mini-spike in January 2024 at the peak of Rate-Cut Mania.

Mortgage applications to purchase a home in the latest week plunged by almost half from the same period in 2021 and 2019:

From 2023: -13%

From 2022: -36%

From 2021: -47%

From 2019: -48%

Mortgage applications are an early indication of home sales volume – an early indication that buyers who need mortgages remain on strike because prices are too high with those rates:

Inventory has been rising, as sales plunged amid rising new listings, and so active listings exploded in some metros on a year-over-year basis in June, and for the US overall, they jumped by 37% year-over-year. And there’s now plenty to choose from, but prices are too high.

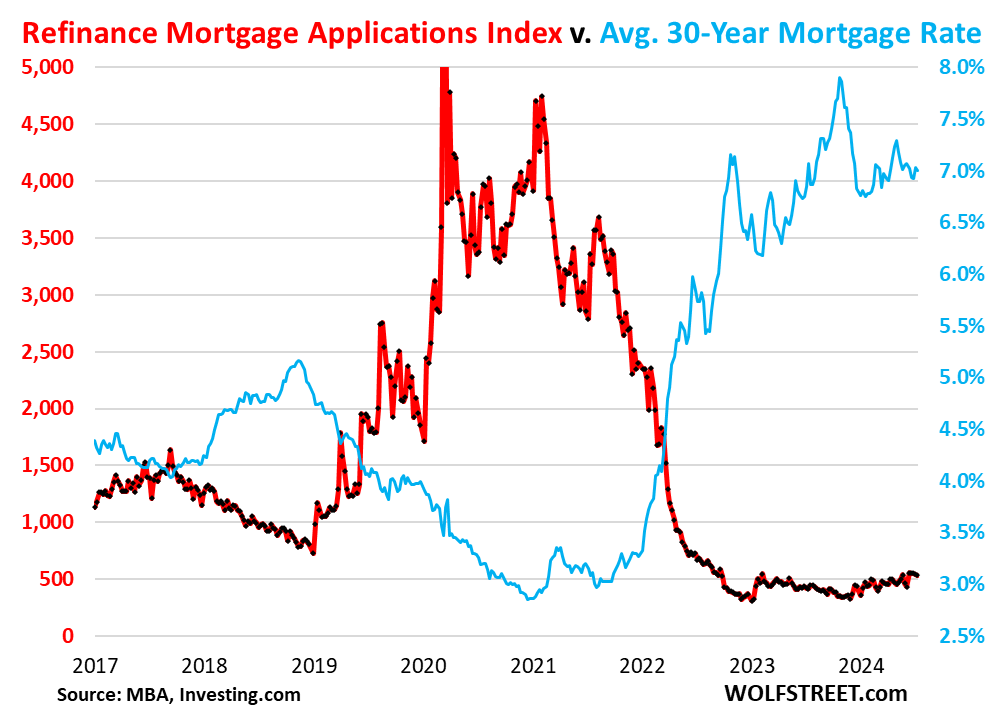

Mortgage applications to refinance a home collapsed in 2022 when mortgage rates surged, and have remained steadfastly at these collapsed levels. Refis without cash-out have nearly vanished. Most of the few refis that are still taking place are cash-out refis.

In the latest reporting week, applications for refinance mortgages edged down further and were down by 84% from the same week in 2021 and by 70% from the same week in 2019.

Refis are a function of mortgage rates. They had experienced a historic boom when mortgage rates plunged to the 2.5%-3.0% range. And they collapsed when mortgage rates began to surge starting in early 2022.

The chart shows the inverse relationship between refi applications (red) and mortgage rates (blue).

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the beer and iced-tea mug to find out how:

Would you like to be notified via email when WOLF STREET publishes a new article? Sign up here.

Take the Survey at https://survey.energynewsbeat.com/