By Wolf Richter for WOLF STREET.

Longer-term Treasury yields spiked this morning, on top of the surge since the September rate cut. Spiking yields means plunging prices, and it has been a bloodbath for bondholders.

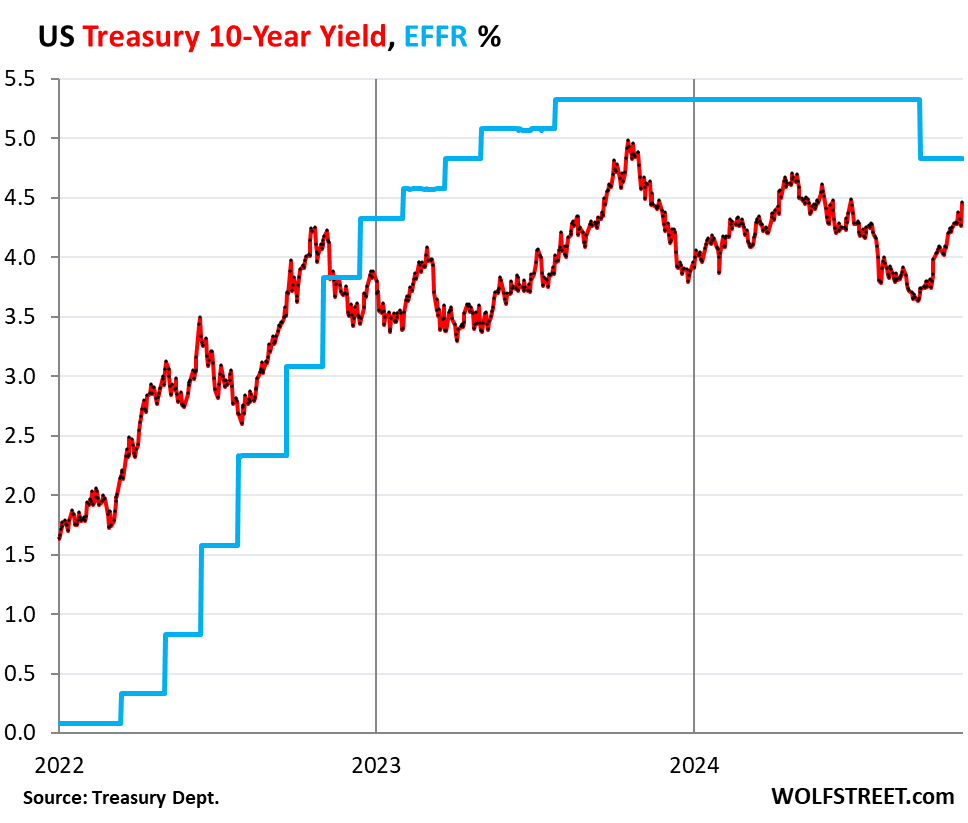

The 10-year Treasury yield spiked by 20 basis points this morning, to 4.46% at the moment, the highest since June 10. Since the Fed’s September 18 rate cut, the 10-year yield has shot up by 81 basis points. 5% here we come?

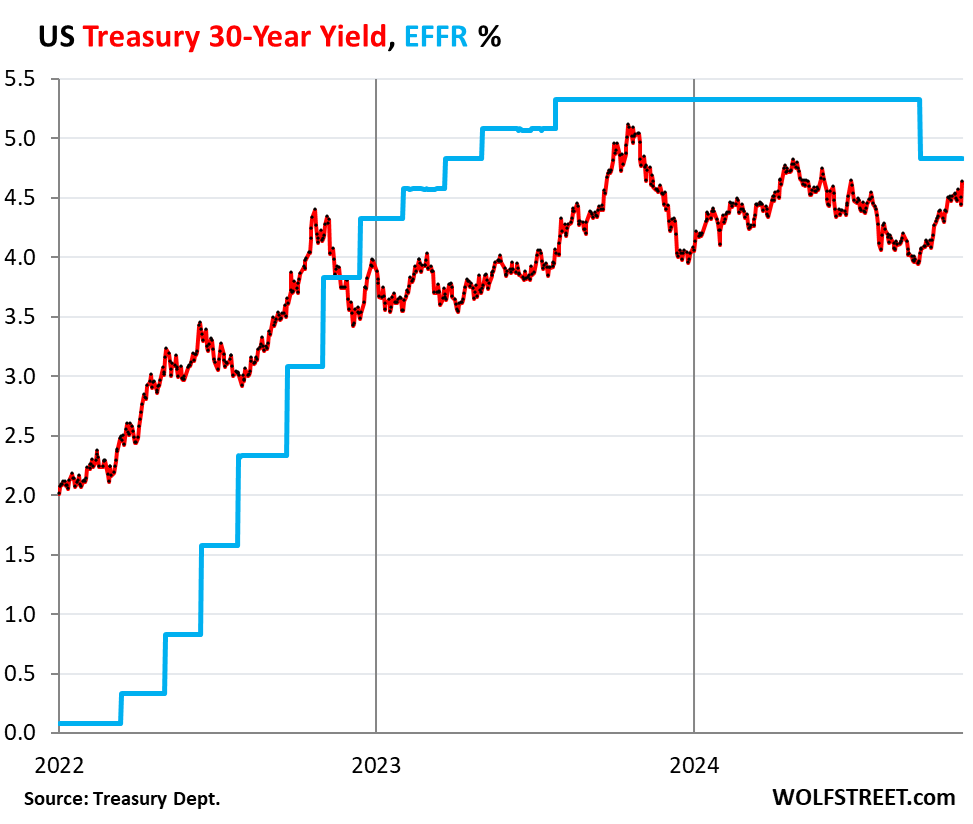

The 30-year Treasury yield spiked by 20 basis points this morning, to 4.64%, the highest since May 31 May 30. Since the Fed’s rate cut on September 18, it has shot up by 68 basis points.

So all the bond market needs to get spooked further are more rate cuts?

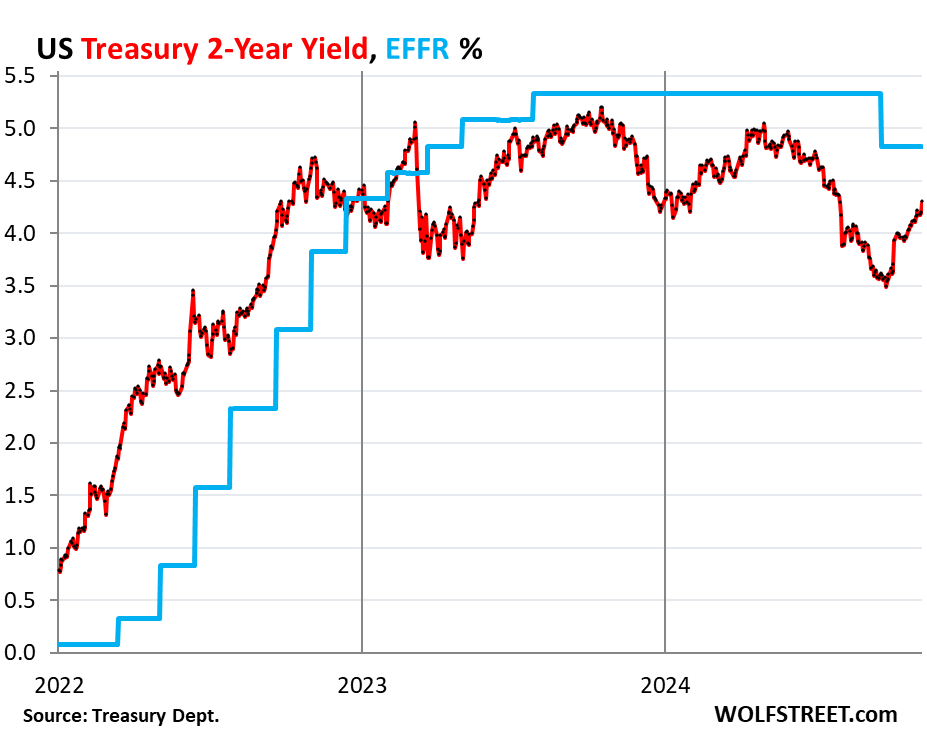

The 2-year Treasury yield shot up by 10 basis points this morning, to 4.29%, the highest since July 31. Since the rate cut, it has shot up by 69 basis points.

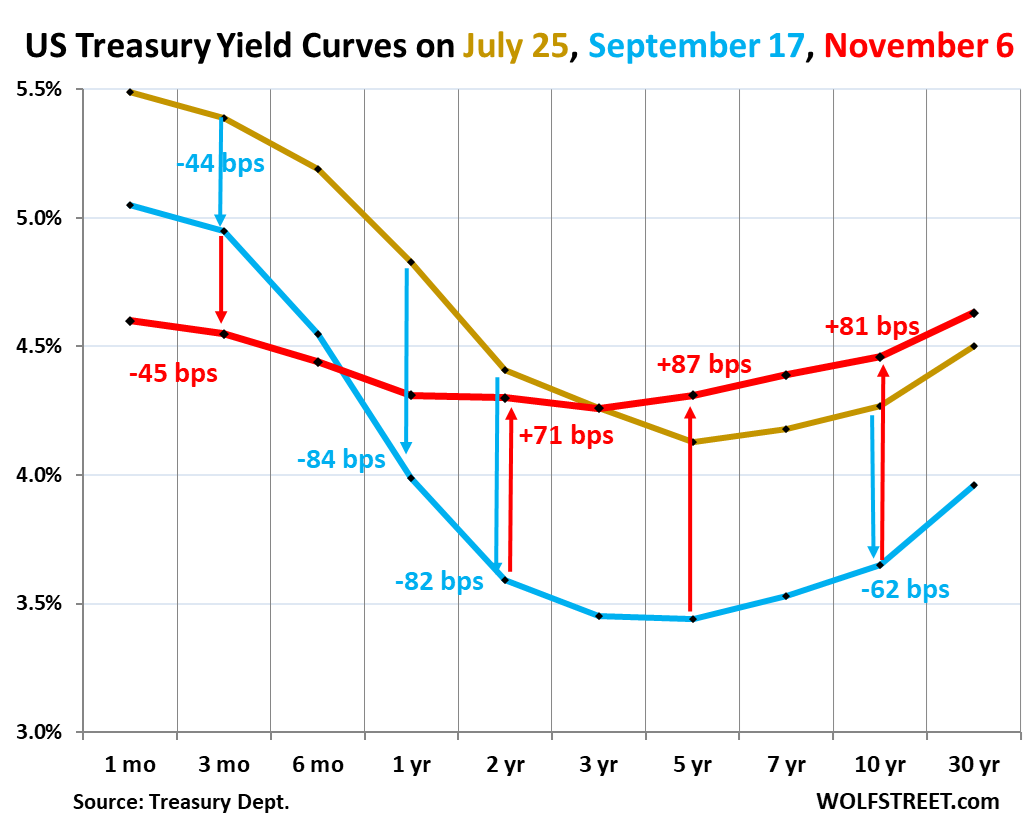

The “yield curve” un-inverted further in another massive leap today, continuing the process of un-inverting, driven by the surge in longer-term yields and the decline in short-term yields.

The normal condition of the yield curve is that longer-term Treasury yields are higher than short-term yields. The yield curve is considered “inverted” when longer-term yields are below short-term yields, which began in July 2022 as the Fed jacked up its policy rates, pushing up short-term Treasury yields, while longer-term yields also rose but more slowly, and thereby fell behind. The yield curve is now in the process of normalizing, with longer-term yields surging and surpassing short-term yields.

The chart below shows the “yield curve” with Treasury yields across the maturity spectrum, from 1 month to 30 years, on three key dates:

- Gold: July 25, 2024, before the labor market data went into a tailspin that has now been revised away.

- Blue: September 17, 2024, the day before the Fed’s mega-rate cut.

- Red: This morning, November 6, 2024 after the election results.

The 30-year yield is now higher than all other yields, and it has un-inverted completely. The 10-year yield is just a few basis points from un-inverting completely.

Note by how far those longer-term yields have risen since the September rate cut (blue line). The yields from 3-years through 10-years have shot up by over 80 basis points since the September rate cut, a screeching-tire U-turn, going down in two months, going back up faster and further in seven weeks, amid huge volatility in the Treasury market.

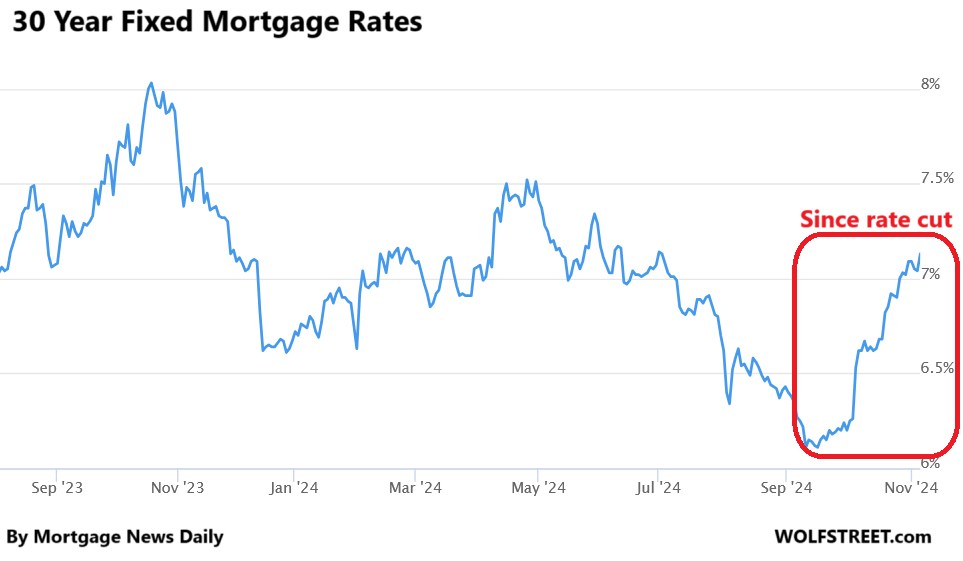

Mortgage rates too. They roughly parallel the 10-year yield, and they spiked today 7.13%, according to the daily measure from Mortgage News Daily.

Mortgage applications through the latest reporting week, which doesn’t capture the last two days, already dropped further from the frozen levels before, pushing down further the demand for existing homes, which is on track to plunge to the lowest levels since 1995 this year.

For the housing industry, and for home sellers, this U-turn was a painful slap in the face. At this pace, the yield curve will enter the normal range soon – but in the opposite way of what the real estate industry had hoped. It had hoped that the Fed would cause short-term yields to plunge to super-low levels in no time, which would drag down longer-term yields, and mortgage rates would follow.

But mortgage rates had already plunged from nearly 8% in November last year to 6.1% by mid-September this year, without any rate cuts, on just a wing and a prayer, thereby pricing in all kinds rate cuts and whatnot. And since the rate cut, much of the wing-and-a-prayer plunge in longer-term yields has reversed, that’s all that has really happened.

The real estate industry was expecting 5.x% mortgages by about right now, and they were already close in mid-September with 6.1% mortgages, and some were talking about 4.x% mortgages just in time for spring selling season, and today they’re looking at 7.13% mortgages.

We give you energy news and help invest in energy projects too, click here to learn more

Crude Oil, LNG, Jet Fuel price quote

ENB Top News

ENB

Energy Dashboard

ENB Podcast

ENB Substack

![]()