Nvidia -7% today, -23% since July 10. But afterhours, it rose when Microsoft outlined what it’s spending on AI infrastructure.

By Wolf Richter for WOLF STREET.

Microsoft reported earnings today afterhours for its fiscal Q4, and as you’d expect, overall revenues beat expectations by a hair; they rose 15% in the quarter, to $64.7 billion. And its net income beat by a hair, rising by 10% to $22 billion, or $2.95 a share.

But there were some details that didn’t go over well. Intelligent Cloud revenues rose by 19% to $28.5 billion, missing expectations by a hair. Within it, revenues from its intently-watched Azure (AI and machine learning) soared by 30% on a constant-currency basis, but that was down from 31% in fiscal Q3, and it missed expectations of 31% growth. And it said during the earnings call that it sees Azure revenue growth slowing to 28% to 29% on a constant-dollar basis.

Revenues from “Productivity and Business Processes” rose 11%; revenues from Windows rose 7%; and revenues from “Consumer Products and Cloud Services” rose 3%. Device revenues fell.

Meanwhile, over at the AI-cash-burn machine, capital expenditures jumped by 55% to $13.9 billion, reflecting the money being thrown at data centers and hardware. During the earnings call, the company said that spending would increase further, that it would “scale” its infrastructure investments “to meet the growing demand signal for our AI and cloud products.”

Over the past 12 months, Microsoft added 7,000 employees, most of them in R&D, bringing the total to 228,000 employees, according to its annual report for the fiscal year, also released today afterhours.

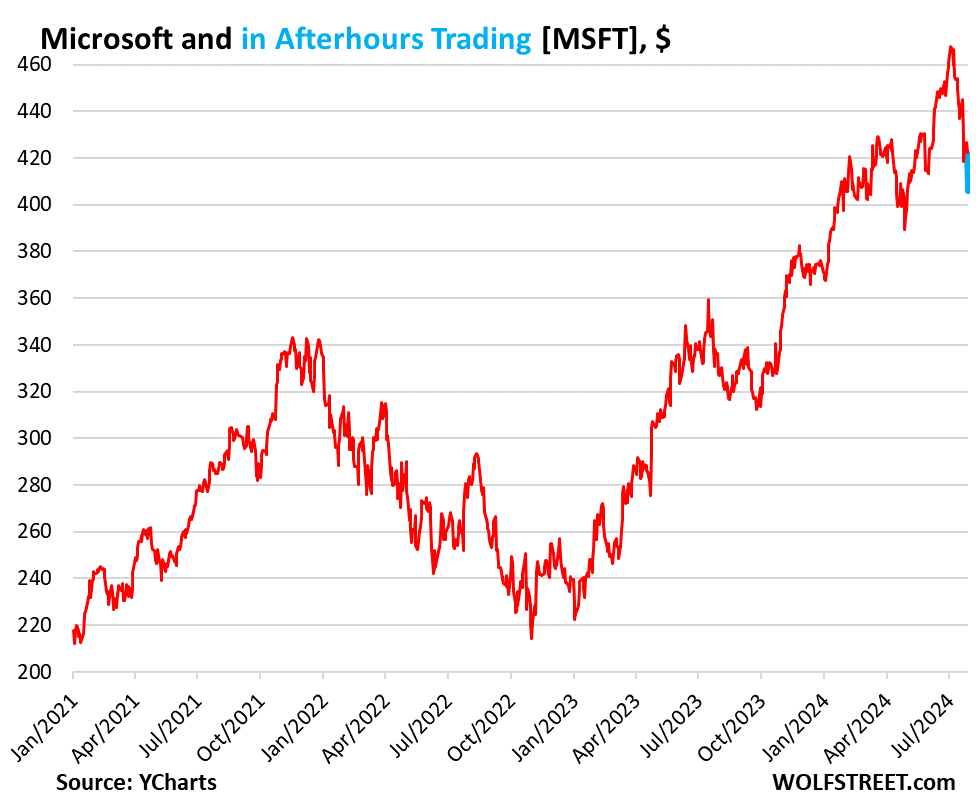

Upon the news, Microsoft shares [MSFT] initially tanked 7% afterhours, then recovered some, and are now down 4%, after having fallen 0.9% during regular hours. Including afterhours, the stock has dropped 12.5% from the peak on July 10:

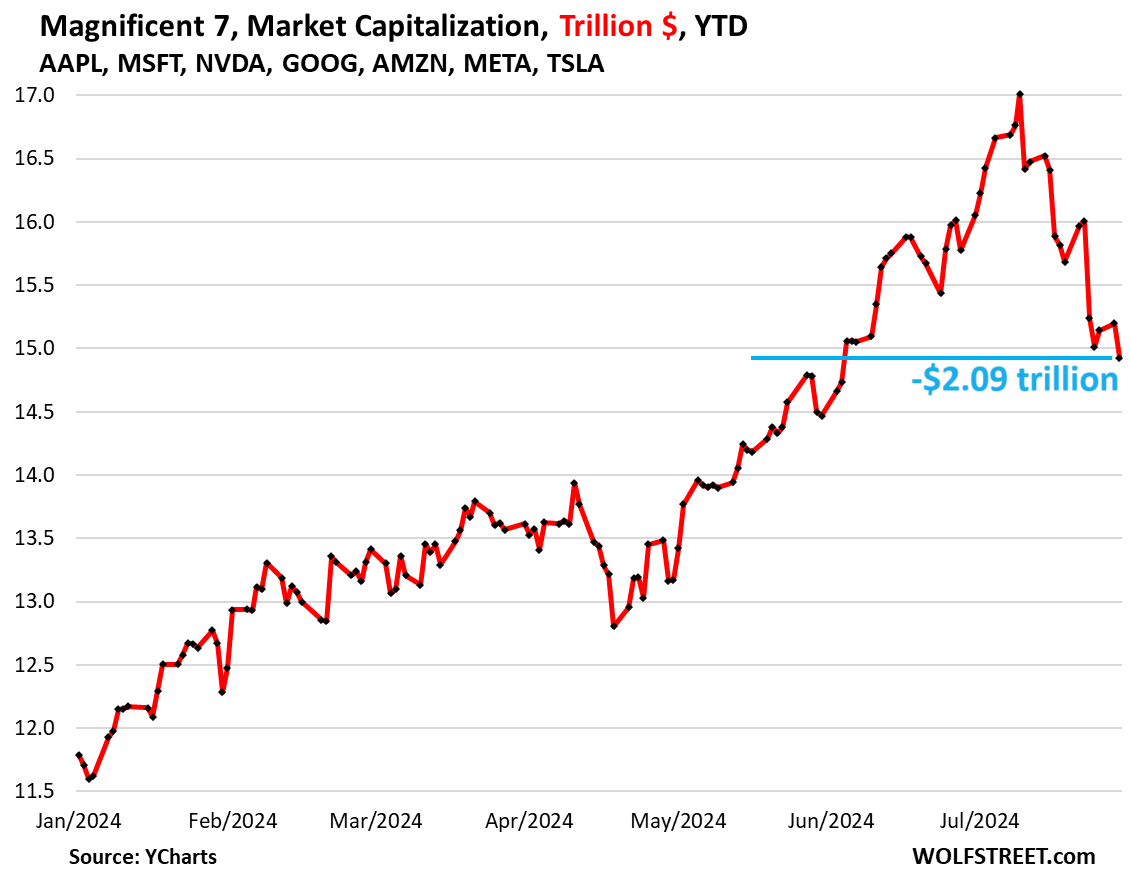

Another crummy day for the Mag 7: -$2.09 trillion from peak.

By the close of regular-hours trading, shares of the Magnificent 7 – Apple, Microsoft, Nvidia, Alphabet, Amazon, Meta, and Tesla – dropped another 1.8%, or by $274 billion in market capitalization.

Since the peak on July 10, they have dropped by 12.3%, or by $2.09 trillion in dollar terms. The combined market cap has now fallen to $14.9 trillion, about where it had been on June 4, down from $17.0 trillion on July 10.

A 12.3% drop would normally be no big deal if the dollar amounts weren’t so huge. But apparently, the huge dollar amounts weren’t a big deal either on the way up, it was just the normal thing to happen, for seven stocks to gain trillions of dollars in value in a matter of months. Easy come, easy go:

Nvidia was the primary driver today, falling 7.0% in regular trading hours, giving up $198 billion in market cap for the day. The stock was down by 23.1% from the peak on July 10, having given up $771 billion in market cap.

But afterhours, it jumped 4.6%, perhaps on Microsoft’s disclosure about the billions it’s spending on AI infrastructure, and that this spending would accelerate further.

Microsoft and Tesla were also responsible for the decline during regular hours. Microsoft fell 0.9% (-$33 billion in market cap), and Tesla fell 4.1% (-$32 billion in market cap). Tesla is down 46% from its all-time high in November 2021. The other four of the Mag 7 were relatively little changed for the day.

The stocks in the Mag 7, from the July 10 peak, in order of the percentage decline:

Nvidia [NVDA]: -23.2% (-$512 billion)

Tesla [TSLA]: -15.5% (-$130 billion)

Meta [META]: -13.3% (-$180 billion)

Microsoft [MSFT]: -9.4% (-$327 billion), not counting the drop afterhours

Alphabet [GOOG]: -11.1% (-$265 billion)

Amazon [AMZN]: -9.0% (-$188 billion)

Apple [AAPL]: -6.3% (-$225 billion)

On a side note: Fed day.

Wednesday is Fed day. The market expects a September rate cut with 100% certainty. There is no longer any room for doubt. And the Fed might confirm that that’s realistic, and that’s what is already priced in. The market doesn’t need that confirmation anymore; it’s already set for a rate cut in September.

But as the Fed has done earlier this year when the market went way overboard with its rate cut mania, it might try to walk back those expectations. The statement might not say anything that would confirm a rate cut in September. And Powell might mention how his “confidence” about inflation heading to 2% was rising but needs a few more good data points to rise enough to make a decision to cut, etc., etc., thereby throwing doubts on a September rate cut. And that could be interesting.

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the beer and iced-tea mug to find out how:

Would you like to be notified via email when WOLF STREET publishes a new article? Sign up here.

Take the Survey at https://survey.energynewsbeat.com/