Europe’s once-mighty industrial engine is sputtering, and Germany—the continent’s manufacturing powerhouse—is at the epicenter of a deepening crisis. High energy costs driven by aggressive Net Zero policies, renewable intermittency, heavy regulations, and carbon pricing are accelerating deindustrialization. Major firms are slashing jobs, closing plants, and relocating production to the United States and Asia, where energy is far cheaper and more reliable.

Recent developments underscore the urgency. On June 30, 2026, economist Peter St. Onge highlighted the trend in a widely shared post: “Europe’s industrial death spiral is accelerating. Volkswagen is laying off 100,000 while every major German carmaker — plus steel and chemicals — moves production to America. Last one out turn off the socialism.”

Volkswagen Leads the Exodus

Volkswagen Group, a symbol of German engineering prowess, is reportedly planning to cut up to 100,000 jobs and close or idle production at up to four German plants (including sites in Hanover, Zwickau, Emden, and Audi’s Neckarsulm facility). This follows earlier announcements of 50,000 cuts by 2030.

The moves come amid struggles with the EV transition, intense Chinese competition, U.S. tariffs, and—critically—Europe’s structurally high energy costs.

The Energy Cost Driver

Industrial electricity prices in the EU remain roughly twice as high as in the United States and about 50% higher than in China, according to the International Energy Agency (IEA) data for 2025.

In 2024, EU industrial electricity averaged around €0.199/kWh, compared to €0.082/kWh in China and €0.075/kWh in the US.

Germany consistently ranks among the highest in Europe.

These gaps persist despite some post-2022 declines from crisis peaks. Energy-intensive sectors (chemicals, steel, autos, glass) bear the brunt. Surveys show 37–51% of German industrial firms considering scaling back or relocating production abroad.

Net Zero Policies Amplify the Problem

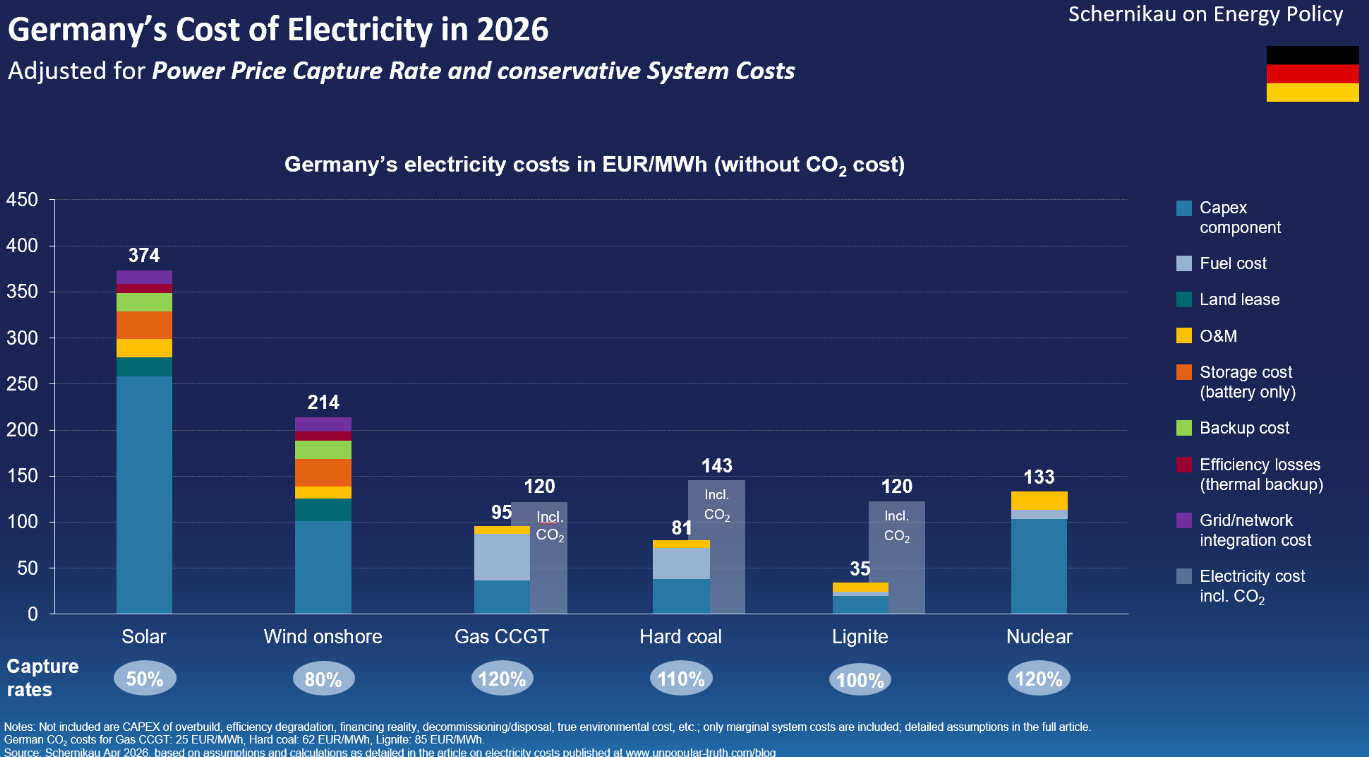

The root issue extends beyond the 2022 energy shock. Europe’s push for rapid decarbonization via wind and solar—under frameworks like the EU Green Deal and Germany’s Energiewende—has imposed massive system costs ignored by simplistic Levelized Cost of Electricity (LCOE) metrics.Dr. Lars Schernikau’s April 2026 analysis in The Unpopular Truth explains why. Full system costs (storage, backup, grid integration, reduced efficiency of dispatchable plants, and lost inertia) make variable renewables far more expensive at high penetration.

In Germany, Adjusted full costs for solar can exceed €374/MWh.

Wind follows closely above €210/MWh.

In contrast, lignite (even with CO₂ costs) remains far cheaper domestically.

Germany now has wind/solar capacity 2.5× peak demand, leading to curtailment and inefficiency. Regulations, carbon taxes (ETS), and subsidies further distort markets and raise costs for remaining fossil and nuclear capacity.The result: unreliable supply, volatile prices, and lost competitiveness. Emissions have fallen, but often through deindustrialization rather than genuine efficiency gains—factories close or move, “exporting” emissions elsewhere.

Deindustrialization in Action

Chemicals: BASF has repeatedly cut production and jobs at its Ludwigshafen complex due to energy spikes (e.g., €3.2 billion extra costs in 2022), closing energy-intensive lines and shifting output to lower-cost regions like the US and Asia.

Steel, autos, and others: Multiple major German carmakers and steel/chemical firms are expanding in the US. Broader manufacturing output has stagnated or declined, with industrial job losses mounting (e.g., 160,000 in Germany in 2025 alone in one report).

EU manufacturing’s share of GDP has fallen significantly. Over 10,000 factories were reported at risk in some 2025 assessments.

Can Europe (and Germany) Recover?

Short-term relief exists. The EU approved Germany’s industrial electricity price subsidy scheme for energy-intensive firms (2026–2028), and the European Commission launched a “Clean Industrial Deal” to support decarbonization while addressing competitiveness.

However, these are largely band-aids—subsidies funded by taxpayers that do not fix underlying problems of intermittency, over-regulation, and ideological commitment to rapid Net Zero timelines.

Longer-term recovery faces steep hurdles:

- Political and ideological lock-in: Reversing course requires admitting policy failures, which faces resistance in Brussels and Berlin.

- Infrastructure and capital flight: Once factories close and skilled workers disperse, rebuilding capacity takes years or decades.

- Global competition: China and the US continue investing in reliable, affordable energy mixes (including nuclear and fossils where needed).

- Energy reality: True low-cost, reliable power favors dispatchable sources. Over-reliance on weather-dependent renewables without adequate backup/storage drives up system costs exponentially at scale.

Some analysts point to political shifts (rising support for pragmatic parties) or potential nuclear revival as glimmers of hope. Others warn that without fundamental reform—deregulation, realistic timelines, and embracing all low-carbon options, including advanced nuclear—the “death spiral” could become permanent.

Europe has slashed emissions more than most regions, but at a steep economic price: crippled industry, higher living costs, and lost global standing. The question is no longer whether the pain is real—it is whether leaders will prioritize affordable, reliable energy over rigid ideology before more irreplaceable industrial capacity is lost forever.

- Peter St. Onge X post (June 30, 2026): https://x.com/profstonge/status/2071919174377689552

- “Rethinking the Cost of Electricity” by Dr. Lars Schernikau, The Unpopular Truth (April 25/30, 2026): https://unpopular-truth.com/2026/04/25/rethinking-the-cost-of-electricity/

- IEA Electricity 2026 – Prices analysis: https://www.iea.org/reports/electricity-2026/prices

- BusinessEurope on high energy costs (citing Eurostat): https://www.businesseurope.eu/media-room/data-hub/high-cost-of-energy/

- WSJ: “Europe’s Green Energy Rush Slashed Emissions—and Crippled the Economy” (Dec 2025)

- Guardian/Reuters/Manager Magazin on VW job cuts and plant plans (June 2026)

- Multiple reports on BASF restructuring and Ludwigshafen challenges

- DIHK and other surveys on German firm relocation intentions

- Eurostat electricity price statistics

- Additional references from OECD NEA, UNECE, and EWI studies on system costs (as cited in Schernikau article)

This article is written for the Energy News Beat channel. All data reflects publicly available reports as of June 2026. Views emphasize empirical evidence on energy economics and industrial outcomes.