California’s energy system is teetering on the edge of collapse. Decades of aggressive refinery closures, strict CARB fuel specifications, and heavy reliance on long-haul imports have left the state uniquely vulnerable. The ongoing disruption in the Strait of Hormuz—triggered by the U.S.-Israeli war on Iran—has now turned that vulnerability into an imminent crisis. Refined product tankers already at sea represent the final buffer. Once they unload, the pipeline goes dry.

Tankers on the Water: The 2–3 Week Clock

Industry analysts tracking Pacific tanker movements report that only two to three more weeks of gasoline, diesel, and jet fuel shipments remain in transit to California ports. These vessels left Asian loading ports (primarily South Korea, Singapore, India, and Japan) before the Hormuz chokepoint effectively closed. No new cargoes are departing to replace them. Asian refiners are prioritizing their own domestic markets amid the global supply squeeze.

Rough supply math (based on public EIA/CEC data and recent analyst estimates):

California’s approximate daily demand: ~850,000–900,000 barrels per day (bpd) of gasoline, plus significant diesel and jet fuel volumes (state leads U.S. in jet fuel consumption).

Imports currently account for roughly 20–40% of total supply (higher effective share post-recent refinery closures). The 42% figure cited in recent reporting reflects the combined impact of lost in-state production and halted Asian refined-product flows.

Pacific transit time: 30–45 days. The remaining ships in the queue, therefore, represent only ~14–21 days of cover once they dock and are offloaded into California terminals and storage.

After that window closes (likely mid-May 2026), California will lose the equivalent of 42% of its gasoline, jet fuel, and diesel supply chain with no immediate replacement. Inventories are already at 10-year lows (and in some categories near record lows), giving the state virtually no cushion.

State officials acknowledge the risk but point to “alternative imports and current stocks” as sufficient for the near term. Analysts are far less optimistic: the full impact will hit pumps and airports in the coming weeks.

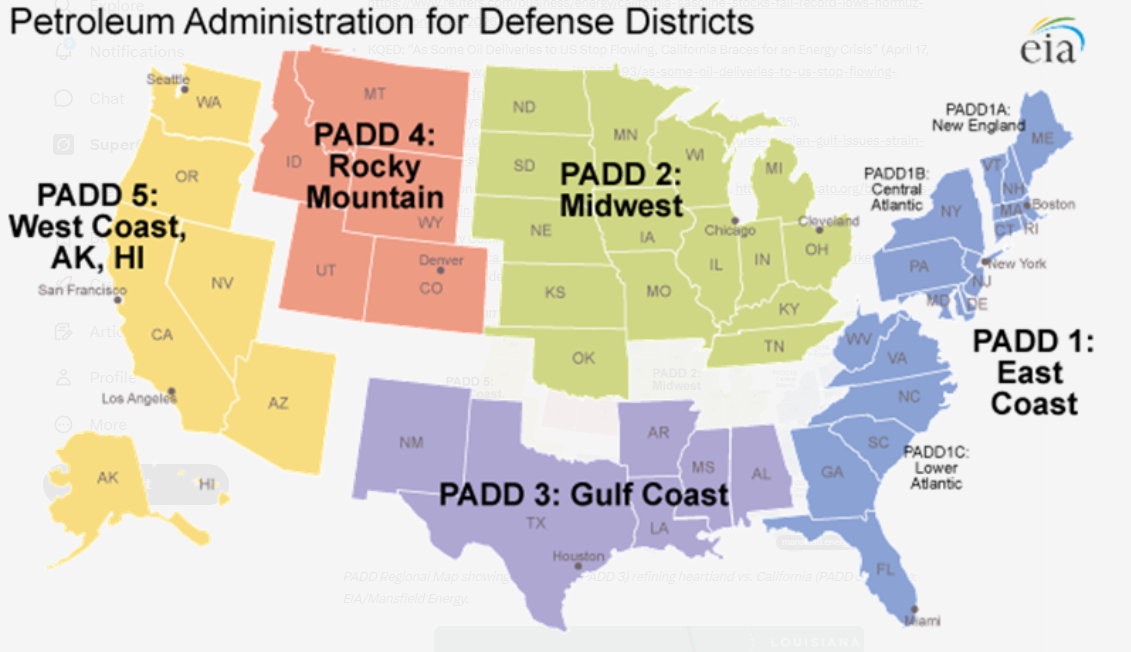

Can the U.S. Gulf Coast Pick Up the Slack?

Yes—if the President acts decisively on two critical waivers.Waive California’s unique CARB fuel requirements (stricter vapor pressure, oxygenates, and emissions specs that most Gulf Coast refineries are not optimized to produce at scale).

Extend or make permanent the Jones Act waiver (already temporarily in effect since mid-March 2026 for 60 days). The Jones Act currently forces ultra-expensive U.S.-flag tankers for coastwise trade; foreign-flag vessels are dramatically cheaper and more abundant.

Gulf Coast reality check (PADD 3):

Home to the world’s largest concentration of refining capacity.

Significant spare or redirectable output (the region is a major net exporter).

With CARB specs waived, Gulf refineries could produce standard U.S. conventional gasoline, ULSD, and jet fuel suitable for California.

Jones Act relief would allow foreign tankers to load directly at Houston, Beaumont, or Lake Charles and sail via Panama Canal or around South America—cutting costs versus the current Bahamas “blend-and-re-export” workaround that California has been forced to use.

However, even the existing temporary Jones Act waiver has produced limited relief so far. Export markets (Europe, Asia) are still outbidding domestic coastwise voyages, and vessel availability for California routes remains tight. A full CARB waiver would remove the single biggest technical barrier, but logistics, pricing arbitrage, and the short-term nature of current waivers limit immediate impact.

Bottom line: Gulf Coast refineries can fill much of the gap, but only with presidential action that removes both the regulatory (CARB) and maritime (Jones Act) handcuffs. Without those waivers, California remains an energy island dependent on disrupted Pacific tankers.

What Happens Next

Without swift federal intervention, California faces:

Gasoline and diesel shortages at the pump.

Jet fuel constraints are grounding flights and threatening military bases.

Skyrocketing prices (already the nation’s highest) and potential economic shutdown effects.

The state’s own policies—refinery closures, underground tank mandates, and refusal to allow conventional U.S. fuels—created this fragility. The Hormuz disruption simply lit the fuse.

Additional public charts on California gasoline inventories and prices are available via the EIA Weekly Petroleum Status Report and CEC dashboards (search “California gasoline stocks April 2026”). Record-low inventory levels align with the 2–3 week tanker timeline cited above.

The clock is ticking. Federal waivers on CARB specs and the Jones Act are the only realistic bridge until domestic refining capacity or new infrastructure can be restored. California cannot import its way out of a self-inflicted supply crisis when the world’s oil arteries are severed.

We will track and reach out to the administration for comments.

Appendix: Sources, Charts & LinksKey Sources & Links

- Energy News Beat / California Globe: “Statewide Fuel Shortages are Imminent” (April 22, 2026) – primary 2–3 week tanker analysis. https://energynewsbeat.co/big-oil-companies/statewide-fuel-shortages-are-imminent/

- Reuters: “California gasoline stocks fall to record lows as Hormuz disruption bites” (April 16, 2026). https://www.reuters.com/business/energy/california-gasoline-stocks-fall-record-lows-hormuz-disruption-bites-2026-04-16/

- KQED: “As Some Oil Deliveries to US Stop Flowing, California Braces for an Energy Crisis” (April 17, 2026). https://www.kqed.org/news/12080093/as-some-oil-deliveries-to-us-stop-flowing-california-braces-for-an-energy-crisis

- RBN Energy: Analysis of Jones Act waiver and PADD 5 impacts (April 2026). https://rbnenergy.com/daily-posts/blog/california-refinery-closures-persian-gulf-issues-strain-padd-5-product-supply

- Cato Institute: Jones Act economics and Bahamas workaround. https://www.cato.org/blog/jones-act-forces-us-gasoline-take-long-way-home

- California Energy Commission petroleum data portal (latest inventories & imports). https://www.energy.ca.gov/data-reports/energy-almanac/californias-petroleum-market

- RBN Energy: Analysis of Jones Act waiver and PADD 5 impacts (April 2026). https://rbnenergy.com/daily-posts/blog/california-refinery-closures-persian-gulf-issues-strain-padd-5-product-supply