We cover 9 Big stories on the Energy News Beat Stand Up

We cover 9 huge stories today. We would like to take a moment to wish all of our great Veterans a Happy Memorial Day, who gave their all so we could be free. Getting to spend time with my 91-year-old Vietnam Vet Dad, who was the only one who came back from Vietnam from his College friends, is very much appreciated, and it helps me be more grateful for the currently deployed great members of our military.

Make no mistake – if the deal is done without the Venezuelan-style controls in place, it just means that the IRGC will be back again like a bad dream or an ex-wife.

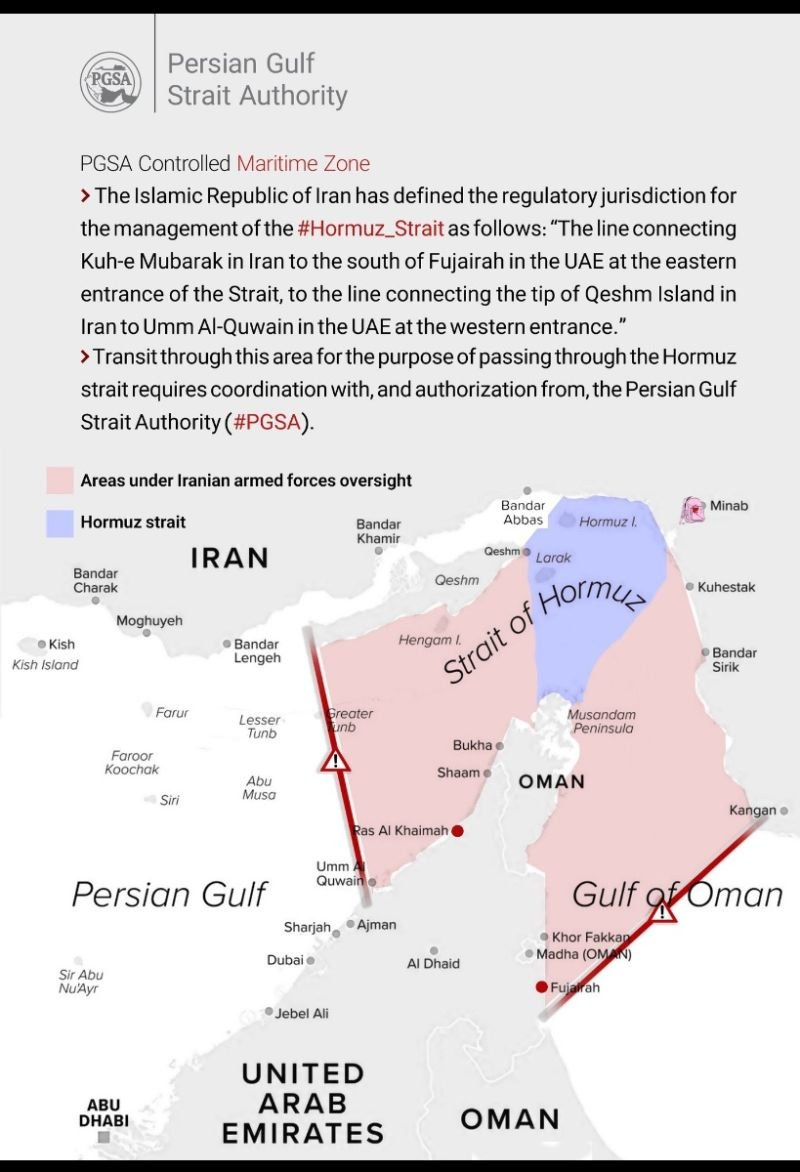

1. Iran Nuclear Deal & Strait of Hormuz

The podcast opens with discussion of potential negotiations between the US and Iran regarding the Strait of Hormuz. Key points include:

- President Trump’s efforts to broker a deal that could reopen the strait for 30-60 days

- Concerns about financial controls over Iranian oil to prevent funding of proxy fighters

- The IRGC’s establishment of the Persian Gulf Strait Authority and their territorial claims

- LNG tankers turning off transponders and navigating around the strait

2. US LNG Exports & Natural Gas Demand

Extensive coverage of America’s energy export capabilities:

- The US is now the world’s top LNG exporter with 11.9-14.9 BCF per day in 2024-2025

- Projections show exports doubling to 30 BCF per day by 2050

- Major projects like Cheniere Energy’s Corpus Christi expansion

- The technology that shrinks natural gas molecules 600 times for transport

3. AI in Oil & Gas Industry

Discussion of AI’s transformative potential:

- AI could unlock $500 billion for oil and gas producers by 2030

- Emphasis on the need for accountability, validation, and explainability in AI implementation

- Real-world example: ADNOC reported $500 million in AI-driven revenue

- The importance of data orchestration and legacy system integration

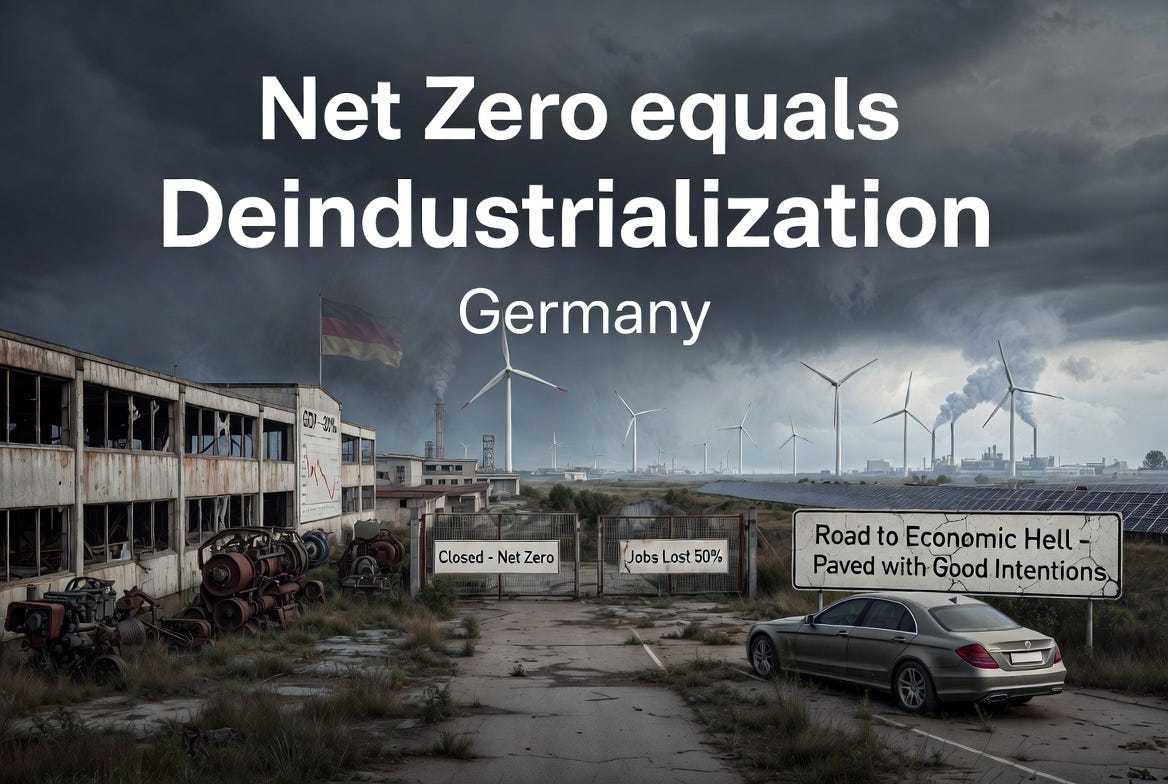

4. Germany’s Energy Crisis & Deindustrialization

Critical analysis of Germany’s net-zero policies:

- Germany’s decision to shut down nuclear and coal plants has backfired

- Real GDP contracted 3% in 2023 and 2% in 2024

- Volkswagen considering closing three German plants with 30,000+ layoffs

- Comparison to similar policies in California and New York

5. Ukraine War & Russian Oil Infrastructure

Brief coverage of ongoing conflict impacts:

- Russian Black Sea oil port attacked by drones

- Discussion of the need to end the Ukraine war

- Calls for Ukrainian leadership change

6. Jamie Dimon’s Economic Warnings

Discussion of JPMorgan CEO’s concerns:

- $5-6 trillion in leveraged corporate debt facing refinancing challenges

- Parallels drawn to 2005-2007 financial crisis

- Concerns about equity values and market stress

- Commentary on the Federal Reserve’s role and structure

7. Jones Act & US Shipping

Discussion of maritime policy:

- Jones Act waiver creating opportunities for foreign tankers

- Need for US-built tankers and shipyards

- Critique of relying on foreign solutions to domestic energy crises

8. Permian Basin Activity

Coverage of oil and gas M&A activity:

- Deal-making surge in the Delaware Basin

- Devon Energy’s major acquisition of undeveloped acres

- Importance of oil and gas royalties for local communities

9. Stock Analysis & Market Trends

Technical analysis of energy sector stocks including:

- Nano Nuclear Energy (NNE)

- Devon Energy

- Cheniere Energy

- Chevron

- Liberty Energy

- Exxon Mobil

The podcast emphasizes energy independence, the importance of reliable energy sources, and skepticism toward certain net-zero policies while advocating for balanced energy solutions.

1.Good News but not Final News on the Iran War and Re-opening of the Strait of Hormuz

I do not trust the IRGC. President Trump says we have a deal – they say they are expanding the Gulf Strait Authority to include the UAE exit points. This is a tough point for the Trump administration.

3.What Does the Demand for Natural Gas and LNG Look Like for the Next 20 Years?

4.AI Could Unlock $500 Billion for Oil and Gas Producers by 2030 — But Only with Accountability

The Wall Street Journal recently captured Germany’s predicament with brutal clarity in pieces like “Germany’s Slow Industrial Suicide.” A LinkedIn post by Doug Sheridan amplified the editorial, highlighting how green mandates, Net Zero zeal, and the Energiewende have delivered deindustrialization instead of the promised green nirvana.

The ironic title nails it: Good intentions around climate policy have paved a road to economic pain, and the iconic German auto industry — once the pride of Mittelstand engineering and export power — is struggling to stay on it.

The Policy Choices: Nuclear “Blow-Up,” Coal Phase-Out, and Lignite Mine “Flooding”

Germany completed its nuclear phase-out in April 2023, shuttering the last three reactors. This was framed as a climate and safety win. In reality, it removed reliable, low-carbon baseload power. Multiple analyses show this led to greater short-term reliance on coal and gas, higher electricity prices, and additional CO₂ emissions — estimates range from tens to over 200+ million tonnes of extra CO₂ equivalent compared to keeping nuclear online alongside renewables.

Coal and lignite phase-out plans (target 2038, with earlier ambitions in some regions) compound the issue. Germany remains Europe’s largest lignite producer and user. While mining continues in key opencast sites (Hambach, Garzweiler in the Rhineland; various in Lusatia), post-mining remediation involves flooding exhausted pits to create massive artificial lakes. These “flooding” plans — for example, turning Hambach into one of Europe’s largest artificial lakes (hundreds of meters deep, billions of cubic meters of water diverted, often from the Rhine over decades) — are part of structural change. They create future recreational assets but bring serious challenges: acid mine drainage, sulfate pollution in rivers like the Spree, groundwater disruptions, and enormous long-term water management costs.

The net result for the economy? Skyrocketing industrial electricity prices (often double U.S. levels), grid instability risks, and lost competitiveness. Renewables reached strong shares — around 59% clean electricity in 2025 (wind ~27%, solar ~18%) with fossils at ~41% — but the transition has been expensive and bumpy.

Deindustrialization in Numbers: Companies Leaving, Shrinking, or Dying

High energy costs, bureaucracy, taxes, and regulatory burden have hammered energy-intensive industries (chemicals, steel, autos, glass, fertilizers). Surveys tell the story:The DIHK Chambers of Industry and Commerce found 37% of industrial companies considering cutting production or relocating abroad (higher — ~45% — for energy-intensive firms). This was up from prior years.

Specific examples of pain (2020–2025 period):BASF: Cut thousands of jobs (hundreds in Ludwigshafen alone), shut energy-intensive lines (e.g., ammonia/fertilizer), and shifted investments/production toward the U.S., Asia, and Belgium, explicitly citing energy and regulatory costs.

Volkswagen: For the first time in its 87-year history, seriously considering or planning to close at least three German plants, with tens of thousands of layoffs (35,000+ cuts discussed) and pay reductions. Competition from China EVs + high German costs are key drivers.

Other hits: ArcelorMittal idled blast furnaces; Bosch planning ~22,000 German job cuts by 2030; numerous auto suppliers and Mittelstand firms scaling back or eyeing moves. Northvolt scaled back European battery plans in favor of U.S. opportunities.

Corporate bankruptcies/insolvencies have surged to decade highs: roughly 22,000–23,900 cases annually in 2024–2025, with sharp year-over-year increases (20%+ in some periods), the worst since the financial crisis era.

Auto sector alone: ~100,000 jobs lost since 2019 (VDA data), with another 125,000 (one in six current jobs) projected gone by 2035 amid EV mandates and broader uncompetitiveness.

GDP and Broader Economic Fallout

Germany — Europe’s former manufacturing engine — has endured its longest period of stagnation since WWII. Real GDP contracted ~0.3% in 2023 and ~0.2% in 2024, with anemic +0.2% growth in 2025. Output remains below mid-2022 levels; industrial production has fallen sharply (roughly 10 percentage points in key measures since recent peaks).

Manufacturing’s share of value added has slipped toward 20%. The “sick man of Europe” label has returned with force. High energy prices, weak exports (China competition), and domestic cost pressures are the primary culprits — not just global factors.

States that follow Germany’s lead on Net Zero are in that 38% higher energy costs for consumers.

What Dimon Actually Said

In the Bloomberg interview, Dimon stated, “A lot of companies are leveraged. There’s about $5–6 trillion of leveraged loans out there. They’re going to have a hard time refinancing at those rates. The equity values would be considerably less. Some will be prepared for it. Some hedge for it. A lot of people didn’t hedge for it.”He has repeatedly drawn parallels to periods before past market stress (including 2005–07 dynamics) and warned that sentiment can flip overnight, leading to liquidity crunches when everyone rushes for cash.

In his 2025 Annual Letter (released April 2026), Dimon noted:

The Iran war raises risks of ongoing oil/commodity price shocks and supply chain disruptions, potentially causing “stickier inflation” and higher interest rates than markets expect.

A “skunk at the party” scenario of inflation rising (possibly in 2026) could pressure asset prices.

High global and US sovereign debt levels, combined with weakening credit standards in leveraged lending and private credit.

Interest rates act like “gravity” to asset prices; rapid drops in prices can trigger flight-to-cash dynamics.

Dimon did not declare an imminent crisis or collapse. He has issued cautions for years (sometimes early), but the current combination of high debt, geopolitical energy shocks, and refinancing walls gives his warnings more weight this time. The economy has shown resilience, yet vulnerabilities are real.

Will the Fed Lower Interest Rates?

The New Chair Factor

Short answer: Not imminently — and Dimon’s warnings do not point to near-term cuts.Key context (as of late May 2026):

Inflation reaccelerated in April to multi-year highs.

Iran-related conflict has pushed oil to four-year highs, adding to commodity and inflation pressures.

Bond yields remain elevated: The 10-year Treasury yield recently hovered around 4.56–4.57%, with the 30-year hitting 5.2% (highest since 2007 in recent sessions).

Roughly $9.7 trillion in US government securities are maturing this year and must be rolled over at much higher rates than the current average (~3.5%).

Kevin Warsh was sworn in as the new Federal Reserve Chair on May 22, 2026. President Trump selected him partly in hopes of delivering lower rates. Warsh has long advocated for a framework that could support lower rates through productivity gains (drawing parallels to the 1990s tech/AI-driven boom) and has criticized aspects of the prior regime.

However, markets are currently pricing in zero rate cuts for the rest of 2026, with the probability of a rate hike rising due to inflation and geopolitical risks. Warsh inherits a data-dependent institution facing sticky inflation and elevated yields. While he may favor eventual easing and reforms (including balance sheet considerations), the near-term path is constrained.

Bottom line: Dimon’s comments highlight why the Fed may stay cautious or even lean restrictive in the short term — to avoid fueling inflation via premature cuts. A recession (if it materializes) could eventually force easing, but that is not the base case signaled by current pricing or the new Chair’s immediate environment.

The Refinancing Aspect: Corporate and Government Debt Wall

This is one of the most concrete risks Dimon flagged.

Corporate leveraged loans: The $5–6 trillion market faces a wall. Many borrowers did not hedge against higher rates. Refinancing at current yields will be painful or impossible for weaker credits, pressuring equity values and potentially triggering defaults or forced asset sales. Private credit defaults have already hit record levels in some portfolios.

Government debt: The US must refinance enormous sums at higher costs, adding to fiscal pressures and deficits.

Broader impact: Nonbank lenders dominate much of this market. Weakening covenants, aggressive assumptions, and limited transparency in private credit amplify risks if sentiment shifts.

Energy sector note: High rates raise the cost of capital for new projects, infrastructure, and M&A. Geopolitical oil strength helps producers in the short term but feeds the inflation/rate feedback loop that complicates long-term planning and financing.

8.The Jones Act Waiver has Turned Into a Boon for California at Our Nation’s Expense

9.There’s a Party Going on in the Permian Delaware – Reese Energy Consulting

Great story from Reese Energy Consulting’s LinkedIn.

The Delaware Basin, the western half of the mighty Permian, is buzzing with deal-making energy. According to Reese Energy Consulting’s May 21, 2026, update, “Looks like the Delaware this week is host of Party Central in Perm Town for upstream M&A and a midstream FID.” With crude prices volatile and recently tipping toward $100 per barrel in spots, producers are actively buying, selling, and expanding positions in one of the world’s most prolific oil and gas provinces.

Reese Energy Consulting, a sharp observer of Permian deal flow, highlighted a flurry of activity that signals robust underlying fundamentals and operator confidence in the Delaware’s long-term potential.

A shout-out to Steve Reese and the Reese Energy Consulting group for sponsoring the Podcast https://reeseenergyconsulting.com/.

Data2 if you have any business systems, can you trust A? Well, they have the patent on validation. . https://data2.zoholandingpage.com/energy

And we have WellDatabase rolling in as a new sponsor. https://welldatabase.com/