“We made too many wrong mistakes.” – Yogi Berra

On July 19, 2022, a group of economics professors from Yale University, the University of Pennsylvania, and the Warsaw School of Economics self-published a 118-page, non-peer-reviewed article titled “Business Retreats and Sanctions Are Crippling the Russian Economy.” Formatted to give the appearance of a rigorous academic study that one might find in a prestigious journal, the authors painted a dim picture of life in Russia in the aftermath of President Putin’s invasion of Ukraine.

According to their analysis, Russia “deals from a position of weakness” in the commodities sector, “Russian imports have largely collapsed,” and “Russia has lost companies representing ~40% of its GDP.” It also claimed that Putin holds “delusions of self-sufficiency and import substitution” and “is resorting to patently unsustainable, dramatic fiscal and monetary intervention to smooth over these structural economic weaknesses.” The final two paragraphs of the abstract hammer home the official adjudication of this pedigreed ensemble, leaving little room for further debate and not so subtly calling into question the patriotism of those who might hold different ideas about how best to execute the economic aspects of the war (emphasis added throughout):

“Looking ahead, there is no path out of economic oblivion for Russia as long as the allied countries remain unified in maintaining and increasing sanctions pressure against Russia, and The Kyiv School of Economics and McFaul-Yermak Working Group have led the way in proposing additional sanctions measures.

Defeatist headlines arguing that Russia’s economy has bounced back are simply not factual – the facts are that, by any metric and on any level, the Russian economy is reeling, and now is not the time to step on the brakes.”

Published at a time when serious flaws in the West’s sanctions strategy were becoming obvious, the article caused quite the stir. In a happy coincidence, the lead author of the study was none other than Yale’s Jeff Sonnenfeld, a media-savvy CNBC regular best known for his work as an executive coach to high-profile CEOs who also enjoy going on CNBC. Sonnenfeld saturated the airways, claiming that early indications of Russia’s resilience were mere proof of the need to double and triple down.

In the weeks before Sonnenfeld suddenly emerged as an expert on Russian domestic economics and international trade, we published an article titled “Crazy Pills” in which we contended that sanctions against Russia would not just fail, but backfire. Our core argument—which required distinctly less than 118 pages to articulate—was simple. Attempts to sanction the volume of commodity exports flowing out of Russia would only serve to drive up their price, leading to more revenue for Putin, not less. Two key excerpts:

“Russia’s energy is going to find its way to the market, and, as perverse as it might sound, we should want it to. Instead of attacking the supply of Putin’s energy, we should be doing everything in our power to increase ours. That is the only way to lower prices and materially impact the funding of his war machine. For highly inelastic products like oil and natural gas, price action works both ways. It does not take significant undersupply for prices to skyrocket, nor does it take significant oversupply for prices to crash…

If oil were $20 a barrel today, would that help or hurt Putin? The answer is self-evident and yet lost on our leaders, and we’re running out of crazy pills.”

We published two other articles on the subject in the ensuing months that further explained why things were not going to plan and emphasized the need for course correction. During various podcast appearances, we also pointed out how dangerously naïve it is to assume that the West holds such vast technological advantage over Russia and its friends that the contributions of Western companies to the Russian economy could not be readily replaced.

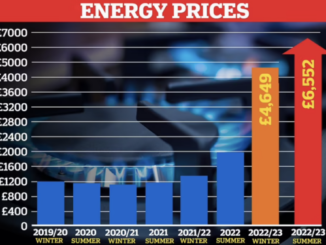

Two years later, the data are in, and virtually nothing predicted in the Sonnenfeld study has come to pass. Commodities continue to be a source of outsized profits for the Putin regime. The Russian economy is booming while Europe battles recession and Ukraine nears collapse on the battlefield—in large part because Russia produces vastly more weapons than the West can supply. Russian imports have been replaced by members of the Global South, especially China. China and Russia have gotten so chummy on trade that US Secretary of State Antony Blinken flew to Beijing and threatened to sanction the country just last week. The Chinese sent him packing, all but daring him to do something about it.

The “lost companies” that represented “~40% of its GDP” merely sold their businesses to new Russian owners on their way out of the country—often at pennies on the dollar—and those businesses quickly reopened under local management. Starbucks is now “Stars Coffee” and McDonald’s is now “Vkusno i tochka,” and both menus are virtually indistinguishable from their pre-war predecessors. The sanctions simply forced a change in the equity stack of the grand Russian capital table, and in Russia’s favor at that.

Putin also decreed that domestic companies no longer need to respect the intellectual property rights of so-called “unfriendly nations.” With a stroke of the pen, all manner of patented inventions—described such that anyone skilled in the art could easily replicate them—became fair game for Russian businesses to exploit without remuneration, helping domestic manufacturers leapfrog ahead in economic development.

And on it goes.

As testimony to the utter failure of the West’s efforts to punish Putin economically, consider the bizarre article that appeared in the Financial Times last week. Circularly titled “Russia’s new economy may end up prolonging its war,” the piece—written by someone currently employed by an economics think tank in Kyiv—is practically indistinguishable from parody:

“The Russian economy’s increasingly structural militarisation significantly complicates any efforts to end the war in Ukraine. Contrary to the expectations that economic constraints would hinder Russia’s capacity to sustain fighting, the spectre of economic collapse might push Vladimir Putin and his officials to double down on militarisation and seek further confrontation, even if aggression against Ukraine hits a standstill.

Russia’s economy grew by 3.6 per cent in 2023 and is projected to expand by over 3 per cent in 2024. Despite ongoing extensive sanctions and export controls, which are expected to hinder investment and potential growth in the long term, Russian authorities have praised themselves for their short-term success in avoiding a deep recession in 2022 and achieving subsequent strong growth.

Much of this success relies on the expansion of the military-industrial complex. The delayed and imperfect introduction of the oil price cap has enabled Russia to bolster fiscal revenues and use them to stimulate the domestic economy. While export controls impede Russia’s military production and make it more expensive, they have not yet resulted in decisive choke points or disruptions in supply chains.”

How did we get here? The answer is simple. Western political leaders have no earthly idea how commodity markets work and vastly underestimate the technical prowess of their adversaries. It is long past time to address both. It might be too late to win the war, but there is still time to impact the resulting peace. Consider these simple proposals:

The Western powers should coordinate and flood the world with commodities to crash global prices, thus devastating the Russian economy in ways sanctions never could. President Biden should temporarily tame or ignore the environmental wing of his progressive coalition and work directly with the fossil fuel industry to radically increase domestic production of oil, gas, and coal. Exports should be facilitated, permits fast-tracked, and excessive environmental regulations swept aside. The US government should incentivize the fossil fuel industry by covering for any losses incurred. Does Biden want to win the war or curry favor with the Sierra Club? He can’t do both, and the time for choosing has arrived.

Two global commodity giants—Canada and Australia—should be leaned on to do the same. The Netherlands should be encouraged to reopen the enormous Groningen natural gas field, and the Germans to restart their mothballed nuclear reactors. The West might lack enough artillery shells, but it has a vast capacity to produce BTUs.

Similarly, rather than impede Russian production and exports, the West should be doing everything in its power to push every fossil fuel molecule that Putin produces to market as seamlessly as possible. Heck, the US military could escort tankers carrying Russian crude! Instead of trying to sanction Russian liquefied natural gas (LNG) production, Biden should be encouraging the Russians to operate their export terminals at full capacity.

Venezuela and Iran should receive the same treatment. Sanctions should be lifted and production encouraged. If there’s oil or gas or coal in the ground somewhere in the world, get it to market as quickly as possible.

Let’s test how long the Russian economy can withstand $10 a barrel crude and $1 a million BTU LNG prices. Let’s test how disciplined OPEC would be in the face of collapsing prices. Let’s test whether the Saudis would continue to spurn senior US diplomats in the way they do now. This is how to regain the upper hand with Putin.

The best time to have implemented this strategy was two years ago when this publication first suggested it. The next best time is today.

“♡ Like” this piece and send it to your favorite elected official, news outlet, chat room, book club, neighbor, and friend!